7 Changes made in Tax Audit Report Form 3CD:

The Central Board of Direct Taxes (CBDT) has notified changes in Form 3CD. Changes in Tax Audit Report The Central Board of Direct Taxes (CBDT) has notified changes in Form 3CD.

Changes in Tax Audit Report

7 Changes made in Tax Audit Report Form 3CD

Recently, CBDT notified changes in Form 3CD. [Read Notification]. This Article discusses the 7 changes that have been made in the Income Tax Audit Report Form [Form 3CD].

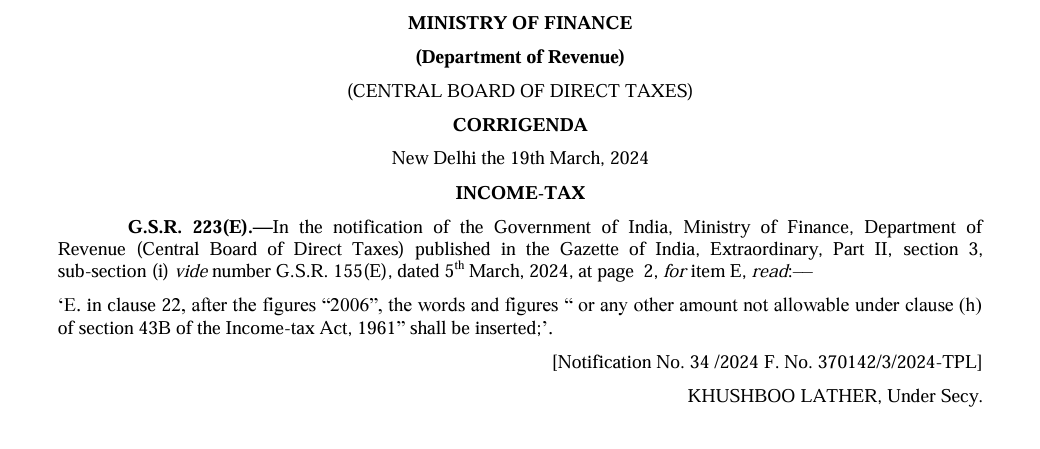

1. Clause 26 [Clause (h) added for MSME Late Payment rule reporting for Disallowance u/s 43B], in respect of sum referred to in specified clauses of section 43B, to include reporting requirement in respect of compliance u/s 43B(h) relating to the amount payable to micro and small enterprises; [Omitted by Corrigendum G.S.R. 223(E), dated 19-3-2024]

2. Clause 22 has been amended to add Disallowance u/s 43B(h) [Added by Corrigendum G.S.R. 223(E), dated 19-3-2024]

2. Clause 22 has been amended to add Disallowance u/s 43B(h) [Added by Corrigendum G.S.R. 223(E), dated 19-3-2024]

3. Clause 8A has been amended relating to whether an assessee has opted for special provisions u/s 115BA/115BAA/115BAB/115BAC/

3. Clause 8A has been amended relating to whether an assessee has opted for special provisions u/s 115BA/115BAA/115BAB/115BAC/ 4. Clause 12 has been amended relating to whether the profit and loss account includes profit computed on a presumptive basis, to include reference to section 44ADA

4. Clause 12 has been amended relating to whether the profit and loss account includes profit computed on a presumptive basis, to include reference to section 44ADA

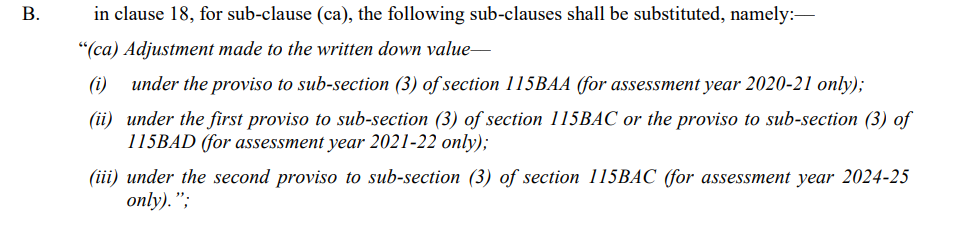

5. Clause 18 relating to particulars of depreciation, sub-clause (ca) has been substituted to require adjustment to the WDV under the different provisos to section 115BAA/115BAC/115BAD for specified assessment years;

5. Clause 18 relating to particulars of depreciation, sub-clause (ca) has been substituted to require adjustment to the WDV under the different provisos to section 115BAA/115BAC/115BAD for specified assessment years;

6. Clause 19 relating to amounts admissible under different sections, to include reference to section 35ABA and any other relevant section;

6. Clause 19 relating to amounts admissible under different sections, to include reference to section 35ABA and any other relevant section;

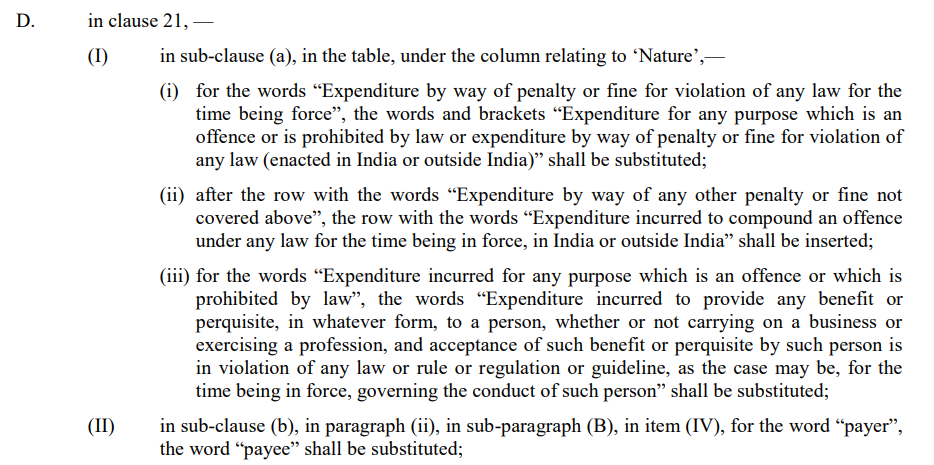

7. Clause 21 relating to details of amounts debited to profit and loss account, being in the nature of capital, personal and advertisement expenditure etc., to include reference to expenditures for any purpose which is an offence or which is prohibited by law or expenditure to compound an offence etc.;

7. Clause 21 relating to details of amounts debited to profit and loss account, being in the nature of capital, personal and advertisement expenditure etc., to include reference to expenditures for any purpose which is an offence or which is prohibited by law or expenditure to compound an offence etc.;

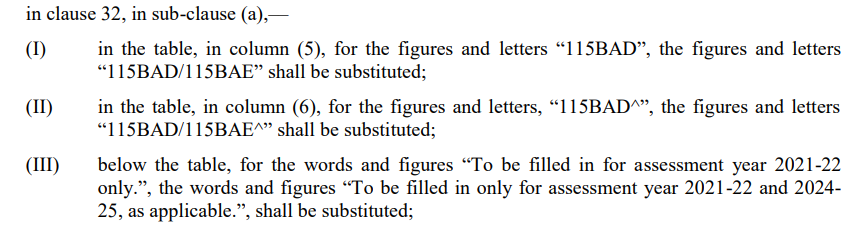

8. Clause 32(a) relating to details of brought forward loss/depreciation, to include reference to losses/allowances not allowed under section 115BAE and amount adjusted by way of withdrawal of additional depreciation on account of opting for taxation under section 115BAE.

8. Clause 32(a) relating to details of brought forward loss/depreciation, to include reference to losses/allowances not allowed under section 115BAE and amount adjusted by way of withdrawal of additional depreciation on account of opting for taxation under section 115BAE.

2. Clause 22 has been amended to add Disallowance u/s 43B(h) [Added by Corrigendum G.S.R. 223(E), dated 19-3-2024]

3. Clause 8A has been amended relating to whether an assessee has opted for special provisions u/s 115BA/115BAA/115BAB/115BAC/

4. Clause 12 has been amended relating to whether the profit and loss account includes profit computed on a presumptive basis, to include reference to section 44ADA

5. Clause 18 relating to particulars of depreciation, sub-clause (ca) has been substituted to require adjustment to the WDV under the different provisos to section 115BAA/115BAC/115BAD for specified assessment years;

6. Clause 19 relating to amounts admissible under different sections, to include reference to section 35ABA and any other relevant section;

7. Clause 21 relating to details of amounts debited to profit and loss account, being in the nature of capital, personal and advertisement expenditure etc., to include reference to expenditures for any purpose which is an offence or which is prohibited by law or expenditure to compound an offence etc.;

8. Clause 32(a) relating to details of brought forward loss/depreciation, to include reference to losses/allowances not allowed under section 115BAE and amount adjusted by way of withdrawal of additional depreciation on account of opting for taxation under section 115BAE.

About Author

CA Pratibha Goyal

Co Founder

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

Studycafe

Studycafe New Delhi, Delhi, India

New Delhi, Delhi, India 1486

1486My Recent Articles

- Biggest Labour Reform in Indian History: 4 Labour Codes Effective from today

- Tax Audit and ITR Due date not extended in this case: Know More

- Government notifies Agreement and Protocol between India and Qatar [Read Notification]

- CA Breaking: Results of ICAI Examination to be announced soon, Know probable Date

- Breaking: GSTR-3B Due Date for September 2025 extended by CBIC amid Diwali Festivities

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts