18% GST on Restaurant services provided at specified premises [Read CBIC FAQs]:

![18% GST on Restaurant services provided at specified premises [Read CBIC FAQs]](https://assets.studycafe.in/uploads/2025/03/GST-on-Restaurant-services.jpg)

CBIC Clarification on GST on Restaurant services provided at specified premises GST on Restaurant services CBIC Clarification on GST on Restaurant services provided at specified premises

GST on Restaurant services

18% GST on Restaurant services provided at specified premises [Read CBIC FAQs]

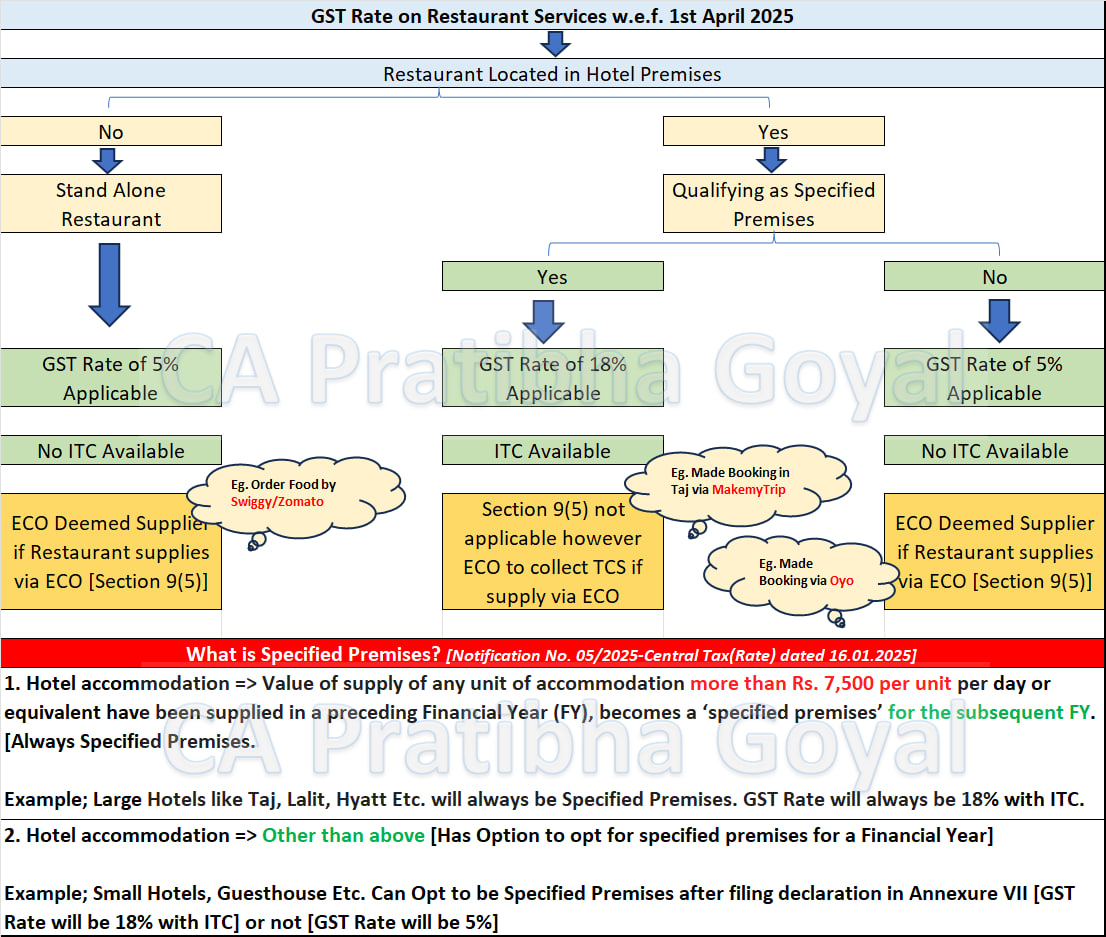

The Central Board of Indirect Taxes & Customs (CBIC) has issued 28 Frequently Asked Questions on 'Restaurant Service' supplied at 'Specified Premises'.

Specified premises are defined as locations where the supplier has provided hotel accommodation services above Rs. 7,500 per unit per day in the previous financial year. Alternatively, premises can be declared as specified through official declarations by registered persons.

Restaurant services provided at specified premises will be subject to GST at a specific rate (likely a different rate than standard restaurant services). Entry 7(vi) of notification No. 11/2017-CTR dated 28.06.2017 prescribes the rate of 18% with ITC for restaurant services supplied at specified premises. For restaurant services supplied outside specified premises, the rate of 5% without ITC is applicable as per entry 7(ii) of notification No. 11/2017-CTR dated 28.06.2017.

Consumers dining at restaurants within specified premises may experience changes in pricing due to GST implications. Businesses operating within these premises must adjust their billing and accounting practices accordingly.

Registered businesses must submit declarations between January 1 and March 31 if they wish to classify their premises as specified.

New businesses must submit their declaration within 15 days of obtaining registration.

Click on the below given link to download the FAQs.

Specified premises are defined as locations where the supplier has provided hotel accommodation services above Rs. 7,500 per unit per day in the previous financial year. Alternatively, premises can be declared as specified through official declarations by registered persons.

Restaurant services provided at specified premises will be subject to GST at a specific rate (likely a different rate than standard restaurant services). Entry 7(vi) of notification No. 11/2017-CTR dated 28.06.2017 prescribes the rate of 18% with ITC for restaurant services supplied at specified premises. For restaurant services supplied outside specified premises, the rate of 5% without ITC is applicable as per entry 7(ii) of notification No. 11/2017-CTR dated 28.06.2017.

Consumers dining at restaurants within specified premises may experience changes in pricing due to GST implications. Businesses operating within these premises must adjust their billing and accounting practices accordingly.

Registered businesses must submit declarations between January 1 and March 31 if they wish to classify their premises as specified.

New businesses must submit their declaration within 15 days of obtaining registration.

Click on the below given link to download the FAQs.

Specified premises are defined as locations where the supplier has provided hotel accommodation services above Rs. 7,500 per unit per day in the previous financial year. Alternatively, premises can be declared as specified through official declarations by registered persons.

Restaurant services provided at specified premises will be subject to GST at a specific rate (likely a different rate than standard restaurant services). Entry 7(vi) of notification No. 11/2017-CTR dated 28.06.2017 prescribes the rate of 18% with ITC for restaurant services supplied at specified premises. For restaurant services supplied outside specified premises, the rate of 5% without ITC is applicable as per entry 7(ii) of notification No. 11/2017-CTR dated 28.06.2017.

Consumers dining at restaurants within specified premises may experience changes in pricing due to GST implications. Businesses operating within these premises must adjust their billing and accounting practices accordingly.

Registered businesses must submit declarations between January 1 and March 31 if they wish to classify their premises as specified.

New businesses must submit their declaration within 15 days of obtaining registration.

Click on the below given link to download the FAQs.About Author

CA Pratibha Goyal

Co Founder

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

Studycafe

Studycafe New Delhi, Delhi, India

New Delhi, Delhi, India 1486

1486My Recent Articles

- Biggest Labour Reform in Indian History: 4 Labour Codes Effective from today

- Tax Audit and ITR Due date not extended in this case: Know More

- Government notifies Agreement and Protocol between India and Qatar [Read Notification]

- CA Breaking: Results of ICAI Examination to be announced soon, Know probable Date

- Breaking: GSTR-3B Due Date for September 2025 extended by CBIC amid Diwali Festivities

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.