8,39,73,416 Filed ITR out of which 5,57,95,391 Filed Zero Tax Liability ITR upto December 2024:

The State Finance Minister in a written reply to a question raised in Lok Sabha said, “8,39,73,416 Filed ITR out of which 5,57,95,391 Filed Zero Tax Liability ITR.”.

5,57,95,391 ITR Filed with Zero Tax Liability

8,39,73,416 Filed ITR out of which 5,57,95,391 Filed Zero Tax Liability ITR upto December 2024

The Minister of State in the Ministry of Finance, Shri Pankaj Chaudhary in a written reply to a question raised in Lok Sabha said, “8,39,73,416 Filed ITR out of which 5,57,95,391 Filed Zero Tax Liability ITR.”.

Shri Janardan Singh Sigriwal asked these questions in Lok Sabha:

Will the Minister of FINANCE be pleased to state:

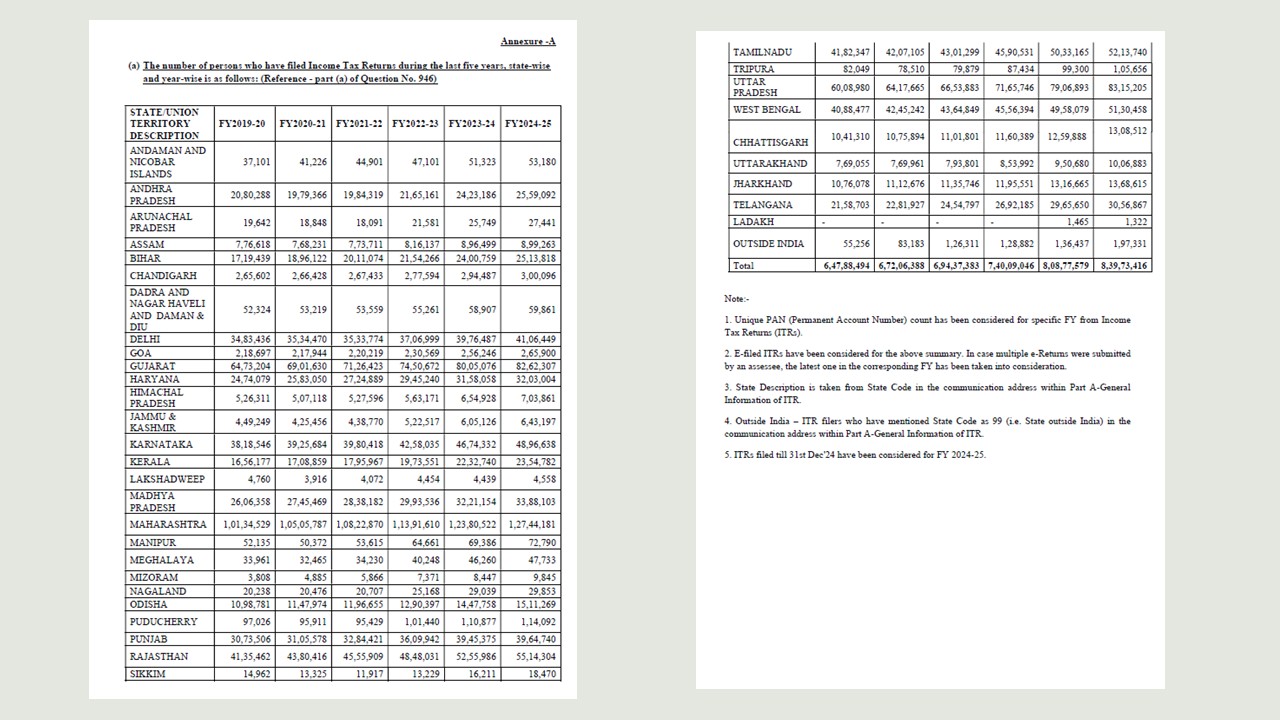

(a) the number of persons who have filed Income Tax Returns during the last five years, State-wise and year-wise;

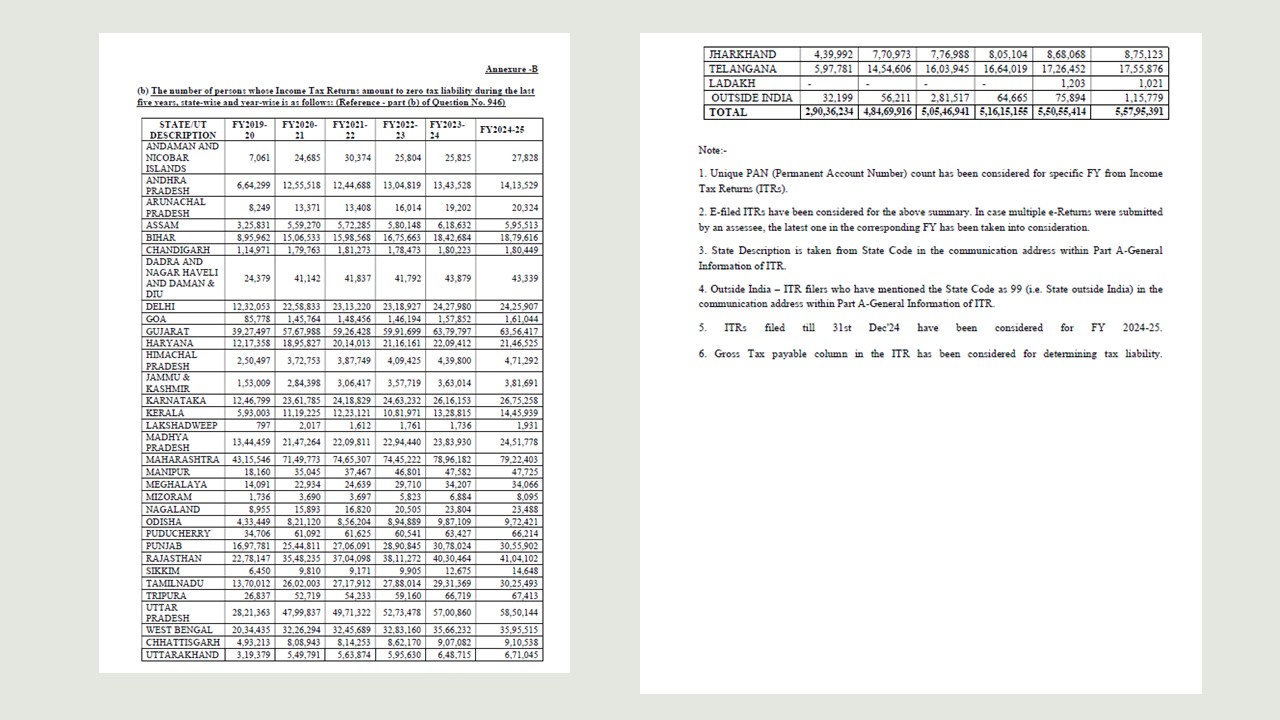

(b) the number of persons whose Income Tax Returns amount to zero tax liability during the last five years, State-wise and year-wise;

(c) whether there is an increase in the number of persons filing Income Tax Returns in the country; and

(d) if so, the details thereof along with the steps taken by the Government attributed to the said increase?

The Minister of State in the Ministry of Finance, Shri Pankaj Chaudhary replied:

(a) The details are attached as Annexure-A.

(b) The details are attached as Annexure-B.

(c) Yes, there is an increase in the number of persons filing Income Tax Returns in the country.

(d) Steps taken by the Government that can be attributed to the increase in the number of persons filing I-T returns are as follows:

New Form 26AS - This new form contains all information of deduction or collection of tax at source, specified financial transaction (SFT), and payment of taxes, demand and refund, pending and completed proceedings. Further, details of SFT data in the Form 26AS makes taxpayer aware about their transactions beforehand and encourages them to disclose their true income.

Pre-filling of Income-tax Returns- In order to make tax compliance more convenient, pre-filled Income tax Returns (ITR) have been provided to individual taxpayers. The scope of information for pre-filing includes information such as salary income, bank interest, dividends, etc.

Updated Return- Section 139(8A) of the Income Tax Act facilitates the taxpayer to update his return anytime within two years from the end of the relevant assessment so that he can file an updated return by voluntarily admitting omissions or mistakes and paying an additional tax as applicable. Further, e-verification scheme was launched to allow taxpayers to disclose their unreported or under-reported income in the updated Income Tax Return.

Reduction in the Corporate tax rate- Starting from the Finance Act, 2016, the corporate tax rates have been gradually reduced while phasing out the exemptions and incentives available to the corporates so as to increase the tax base.

Simplification of the Personal Income Tax- Finance Act, 2020 simplified the filing of Income Tax Returns by providing an option to individual taxpayers for paying income-tax at lower slab rates if they do not avail specified exemption and incentive.

Black Money Act- In order to curb the flow of black money stashed abroad, the Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act, 2015 (the Black Money Act) has been enacted, it increased the voluntary compliance in filing Income Tax Returns.

Benami Law- The Benami Transactions (Prohibition) Act, 1988, was comprehensively amended by the Benami Transactions (Prohibition) Amendment Act, 2016 to enable confiscation of Benami Property and prosecution of benamidar and the beneficial owner.

Expansion of scope of TDS/TCS - For bringing new tax-payers into the net of income tax department, scope of TDS/TCS was expanded by including huge cash withdrawal, foreign remittance, purchase of luxury car, e-commerce participants, sale of goods, acquisition of immovable property, remittance under LRS, purchase of overseas tour program package etc.

Annexure A

Annexure B

Annexure B

ITRs filed till 31st Dec'24 have been considered for FY 2024-25.

ITRs filed till 31st Dec'24 have been considered for FY 2024-25.

Annexure B

ITRs filed till 31st Dec'24 have been considered for FY 2024-25.About Author

Reetu

Content Manager

Reetu is a Content Writer with 4+ years of experience in GST, Income Tax, Finance, Company Law, Education and Career Related Content. She is a B.COM (Honrs.) Graduate.

Reetu is a Content Writer with 4+ years of experience in GST, Income Tax, Finance, Company Law, Education and Career Related Content. She is a B.COM (Honrs.) Graduate.

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 8072

8072My Recent Articles

- Income Tax Guide for Indian Defence Personnel for Tax Filing, Taxable Allowances and Other Benefits

- Income Tax Return Breaking: ITR Forms released for AY 25-26

- Ex-DRT Officials Sentenced to 5 Years Rigorous Imprisonment by Madras High Court along with Rs.27 Lakh Fine

- GSTN issued Advisory on Case Sensitivity in IRN Generation

- RBI to issue Notes of Rs.10 and Rs.500 bearing Signature of Guv Malhotra

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.