Tribunal follows Bombay High Court ruling in connected shareholder buyback cases involving same company.

Meetu Kumari | May 31, 2026 |

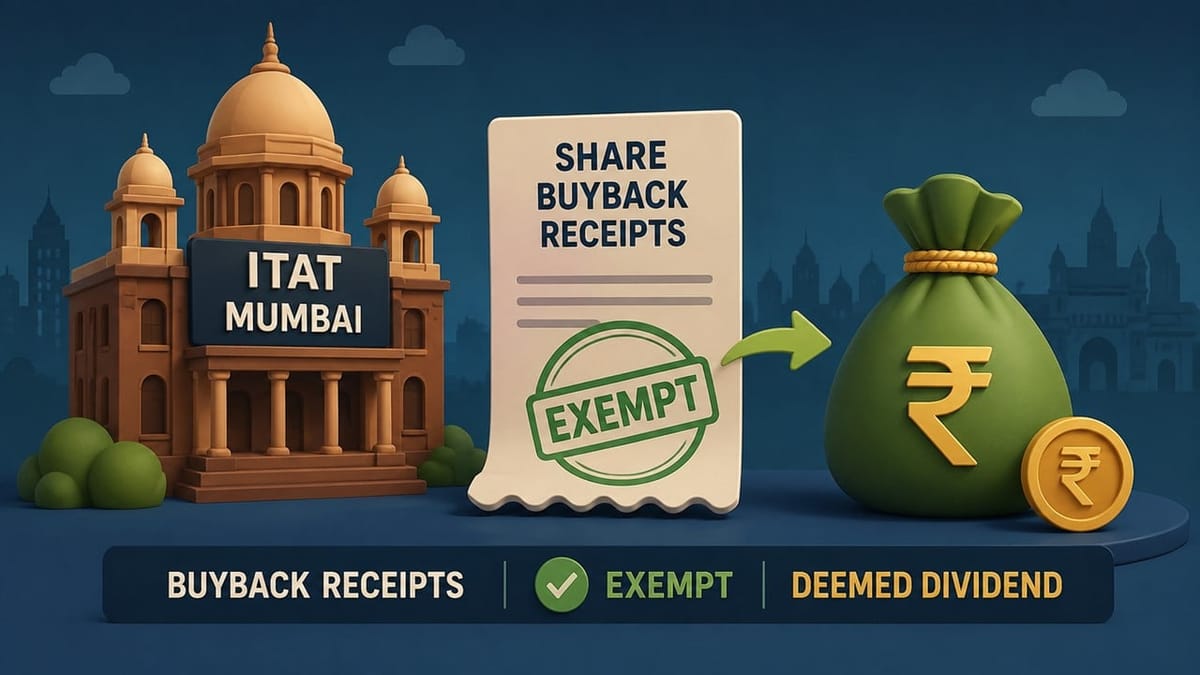

ITAT Mumbai Treats Share Buyback Receipts as Exempt Deemed Dividend

The Mumbai Bench of the Income Tax Appellate Tribunal (ITAT) held that consideration received by a shareholder on buyback of shares pursuant to a court-approved scheme of arrangement was taxable as deemed dividend under Section 2(22)(d) of the Income Tax Act, but remained exempt in the hands of the shareholder under Section 10(34).

The assessee had purchased 25,466 shares of M/s Spirax Marshall Pvt. Ltd. on 31.03.2006 for Rs.1.04 crore and sold them back to the company on 05.04.2007 for Rs.4.96 crore under a buyback arrangement approved by the High Court. In the return of income, the assessee declared long-term capital gains of Rs.3.91 crore after indexation and also claimed deduction under Section 54F against purchase of a residential flat.

During reassessment proceedings, the Assessing Officer denied the Section 54F deduction and also rejected the assessee’s claim of long-term capital gains treatment. The Department treated the transaction differently on the ground that the conditions for exemption were not fulfilled.

Before the Tribunal, the assessee argued that identical transactions undertaken by other family shareholders had already been adjudicated by the Tribunal and the Bombay High Court. In those cases, the Revenue itself had treated the buyback consideration as deemed dividend under Section 2(22)(d) rather than capital gains, and the courts ultimately held that such deemed dividend was exempt under Section 10(34).

The Tribunal noted that the assessee, along with family members, had sold shares to the same company under the same scheme of arrangement. It observed that in the cases of Kamal Imran Panju and Smt. Kayan Jamshid Pandole, the Department had itself recharacterised the receipts as deemed dividend under Section 2(22)(d). Those findings were upheld by both the Tribunal and the Bombay High Court.

Relying heavily on the Bombay High Court ruling in PCIT v. Smt. Kayan Jamshid Pandole, the Tribunal reiterated that deemed dividend under Section 2(22)(d) falls within the scope of Chapter XII-D and consequently qualifies for exemption under Section 10(34) read with Section 115-O.

The Tribunal rejected the Revenue’s argument that exemption under Section 10(34) should not apply merely because the company had not paid dividend distribution tax under Section 115-O. It observed that if an income is statutorily exempt in the hands of the recipient, such exemption cannot be denied solely due to default by the payer company.

Thus, the Tribunal held that although the receipt from buyback of shares was in the nature of deemed dividend under Section 2(22)(d), it was exempt under Section 10(34). The Assessing Officer was directed to delete the addition made in the reassessment proceedings.

To Read Full Order, Download PDF Given Below.

In case of any Doubt regarding Membership you can mail us at [email protected]

Join Studycafe's WhatsApp Group or Telegram Channel for Latest Updates on Government Job, Sarkari Naukri, Private Jobs, Income Tax, GST, Companies Act, Judgements and CA, CS, ICWA, and MUCH MORE!"