ITAT held that cash deposits already recorded and taxed in the successor proprietorship concern cannot be taxed again in the hands of the dissolved partnership firm and remanded the matter for verification.

Vanshika verma | Jun 5, 2026 |

If Deposits Are Already Included in Proprietor’s Income, They Cannot Be Taxed Again: ITAT

The Income Tax Department filed an appeal before the Income Tax Appellate Tribunal (ITAT), Delhi, against an order of the CIT(A) for Assessment Year 2017-18.

The case was related to Devarshi Pharma, which had cash deposits in its bank account during the demonetisation period. AO noted cash deposits of Rs. 27,90,000 and other credits of Rs. 1,27,92,803 approximately in the bank account. Since no satisfactory explanation was given during assessment proceedings, the AO treated the total amount of Rs. 1,55,82,803 as unexplained money under section 69A of the Income Tax Act and added it to the income of the firm.

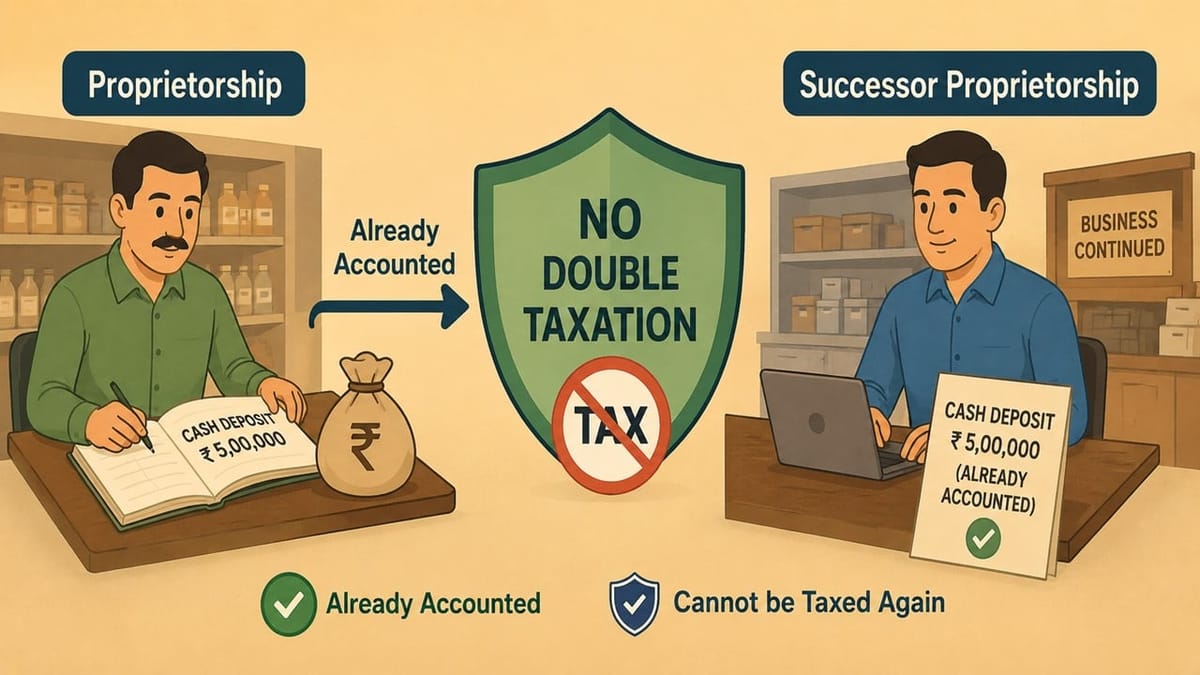

On appeal, Devarshi Pharma submitted that the partnership firm had been dissolved on 31st March, 2015. The assessee states that the business was taken over by one of the partners, namely, Mr Vikas Mohan Gupta, and was carried on as a proprietorship concern in the same name of “Devarshi Pharma”. The assessee further stated that all transactions in the bank account had been recorded in the books of the proprietorship business and were reflected in the proprietor’s income tax return.

The assessee further explained that although a request had been made to the bank to change the PAN from that of the partnership firm to the proprietor’s PAN, the bank had not updated its records. As a result, the tax department continued to treat the bank account as being of the dissolved partnership firm.

On perusal of the records, the CIT(A) accepted the assessee’s argument. The CIT(A), relying on the Supreme Court decision in the Maruti Suzuki case, held that an assessment in the name of a non-existent entity is void. Since the partnership firm was dissolved prior to the commencement of the assessment proceedings, CIT(A) held the assessment void and deleted the entire addition.

However, the ITAT did not agree with the conclusion of the CIT(A). The Tribunal observed that though the partnership firm was dissolved, the business continued under the same name, Devarshi Pharma, as a proprietorship concern. Therefore, the situation was different from cases where the entity completely ceased to exist.

The Tribunal noted that the assessee had claimed that all the bank transactions were recorded in the books of the proprietorship concern and had been included in the income declared by Mr. Vikas Mohan Gupta. However, the CIT(A) had not verified these facts or given any clear findings on them.

The ITAT held that if the impugned cash deposits and credits were already brought to books of proprietorship concern and included in the taxable income of the proprietor, then the same amount cannot be taxed again in the hands of the previous partnership firm.

Thus, the Tribunal set aside the order on merits and remanded the matter to the assessing officer for verification. The AO is directed to examine whether the bank transactions have been correctly recorded in the books of the proprietorship concern and in the income of Mr. Vikas Mohan Gupta. If this is indeed correct, the addition should be removed.

As a result, the Revenue’s appeal was allowed for statistical purposes.

In case of any Doubt regarding Membership you can mail us at [email protected]

Join Studycafe's WhatsApp Group or Telegram Channel for Latest Updates on Government Job, Sarkari Naukri, Private Jobs, Income Tax, GST, Companies Act, Judgements and CA, CS, ICWA, and MUCH MORE!"

![Government notifies exemption for FIIs on interest on Government Securities [Read Notification]](/cdn-cgi/image/width=320,height=195,fit=contain,format=webp,gravity=auto,metadata=none,quality=75/wp-content/uploads/2026/06/Government-Issues-Income-tax-Amendment-Ordinance-2026-to-Exempt-Certain-Foreign-Investors.jpg)