The Income Tax Appellate Tribunal (ITAT) has held SBNs received during demonetisation cannot be treated as unexplained cash credits merely because such notes ceased to be legal tender.

Saima | Jun 13, 2026 |

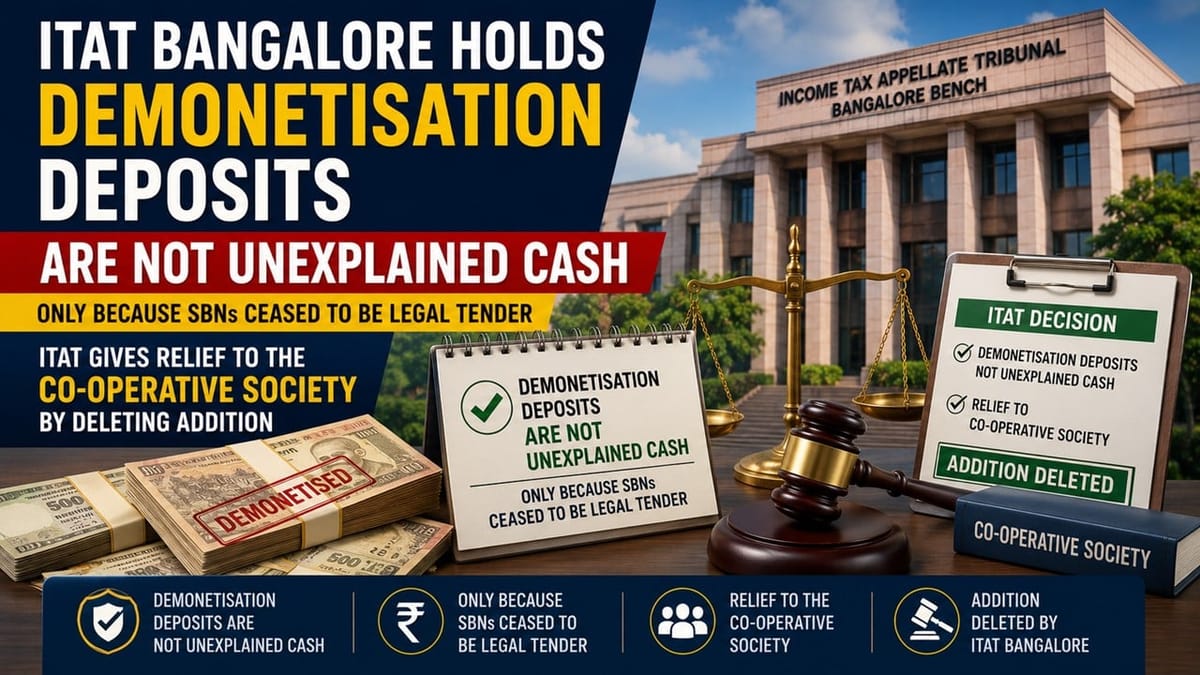

ITAT Holds Demonetisation Deposits Are Not Unexplained Cash Only Because SBNs Ceased to be Legal Tender

The Income Tax Appellate Tribunal (ITAT) Bangalore held that acceptance of Specified Bank Notes during the demonetisation period prior to 31 December 2016 cannot be treated as unexplained cash credit.

The assessee is a co-operative society registered under the Karnataka Co-operative Societies Act, 1959 and is engaged in providing credit facilities to its members. For assessment year 2017-18, it filed its return and declared a total income of Rs 5.30 lakh after claiming deductions under Section 80P of the Income Tax Act. During scrutiny proceedings, the AO noticed that the society had accepted deposits from its members in the form of Specified Bank Notes (SBNs) during the demonetisation period that amounts to Rs 2.2 lakh.

The AO observed that after 8 November 2016, SBNs had ceased to be legal tender and therefore had no monetary value. Consequently, the amount was treated as unexplained cash credit under Section 68 of the Income Tax Act and added to the assessee’s income. The CIT(A) upheld the addition, leading the assessee to file an appeal before the Tribunal.

The Tribunal referred to Section 5 of the Specified Bank Notes (Cessation of Liabilities) Act, 2017 and observed that the prohibition against SBNs became effective only from the “appointed date”, namely 31 December 2016 and therefore, receipt of SBNs prior to that date could not automatically be regarded as illegal or unexplained and it could not form the sole basis for making an addition under Section 68 of the Income Tax Act. At the same time, the Tribunal clarified that the assessee still required the proof of the identity of the members from whom the SBNs were received and the furnishing of complete KYC particulars.

The Tribunal directed that the addition under Section 68 should be deleted in respect of all deposits where the assessee furnishes satisfactory details of the concerned members. The AO was also directed to provide an adequate opportunity of hearing before passing any fresh order. The ITAT set aside the orders of the lower authorities and restored the matter to the file of the AO for a limited verification of the identity and KYC details of the members who had deposited the SBNs. Accordingly, the appeal of the assessee was allowed for statistical purposes.

In case of any Doubt regarding Membership you can mail us at [email protected]

Join Studycafe's WhatsApp Group or Telegram Channel for Latest Updates on Government Job, Sarkari Naukri, Private Jobs, Income Tax, GST, Companies Act, Judgements and CA, CS, ICWA, and MUCH MORE!"