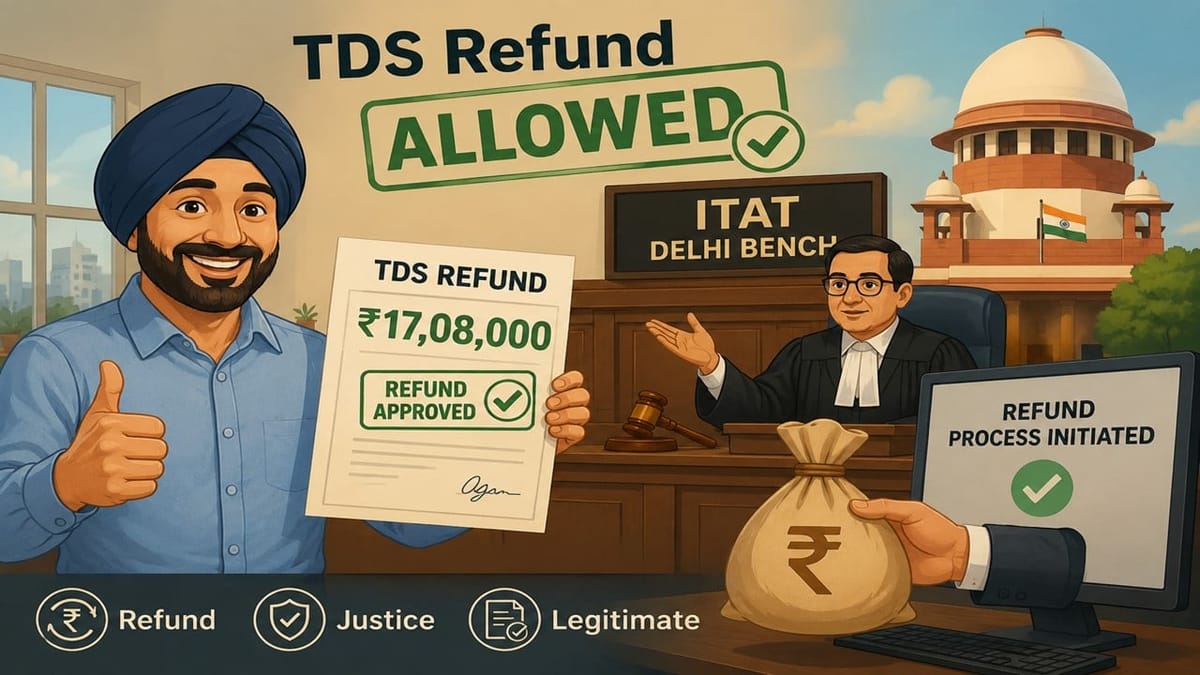

ITAT held that a genuine, condoned delay in e-verification cannot be used to deny a lawful TDS refund, and directed the Income Tax Department to refund over Rs 17 lakh to the taxpayer.

Vanshika verma | Jun 18, 2026 |

Missed ITR Verification While Caring for Ailing Father, Lost Rs. 17 Lakh Refund; ITAT Orders Release of Refund

The Delhi Bench of the Income Tax Appellate Tribunal (ITAT) has ruled in favor of taxpayer Gurcharan Singh Bhatia and directed the Income Tax Department to refund more than Rs 17 lakh that had been deducted as Tax Deducted at Source (TDS).

The case related to Assessment Year 2015-16. Mr. Bhatia had filed his income tax return on time in September 2015, declaring nil taxable income after adjusting business losses and carried-forward losses. Since tax had already been deducted from his rental income, he claimed a refund of Rs 17.08 lakh.

However, the Income Tax Department refused to process the refund because the return had not been electronically verified within the prescribed time. According to the taxpayer, the delay occurred because he was occupied with caring for his seriously ill 83-year-old father and could not complete the e-verification process on time.

Later, in February 2018, he applied for condonation of delay. The Central Processing Centre (CPC) accepted his request and treated the return as valid after successful e-verification. Despite this, the refund was still not issued.

The assessee approached the department multiple times and also filed an application for rectification under section 154 of the Income Tax Act. The Assessing Officer rejected the request. The appellate authority also upheld the rejection on the ground that the return was not verified within the original time limit.

The taxpayer had contended before the ITAT that the delay had already been condoned and it was unjust and illegal to deny the refund of tax which was lawfully deducted from his income. He relied on decisions of the Karnataka High Court and Gujarat High Court whereby the court ruled that tax authorities should not deny legitimate relief on mere technical grounds.

The Tribunal agreed with the taxpayer. It noted that the amount of TDS was admittedly deducted and was also reflected in the official tax records. Having condoned the delay in e-verification, there was no justification for withholding the refund.

The ITAT emphasised that the government cannot retain amounts of tax without legal authority under Article 265 of the Constitution of India. The Tribunal observed that the Revenue would be unjustly enriched by denial of refund on account of a mere technical lapse.

The Bench said that the tax authorities are duty bound to see that only such amount of tax as is legally due is collected and retained. The refusal to grant the refund was a miscarriage of justice because the taxpayer had given a genuine reason for the delay and the delay had been condoned.

Accordingly, the ITAT set aside the orders of the lower authorities and directed the Assessing Officer/ CPC to take necessary steps to issue the refund in accordance with law.

In case of any Doubt regarding Membership you can mail us at [email protected]

Join Studycafe's WhatsApp Group or Telegram Channel for Latest Updates on Government Job, Sarkari Naukri, Private Jobs, Income Tax, GST, Companies Act, Judgements and CA, CS, ICWA, and MUCH MORE!"