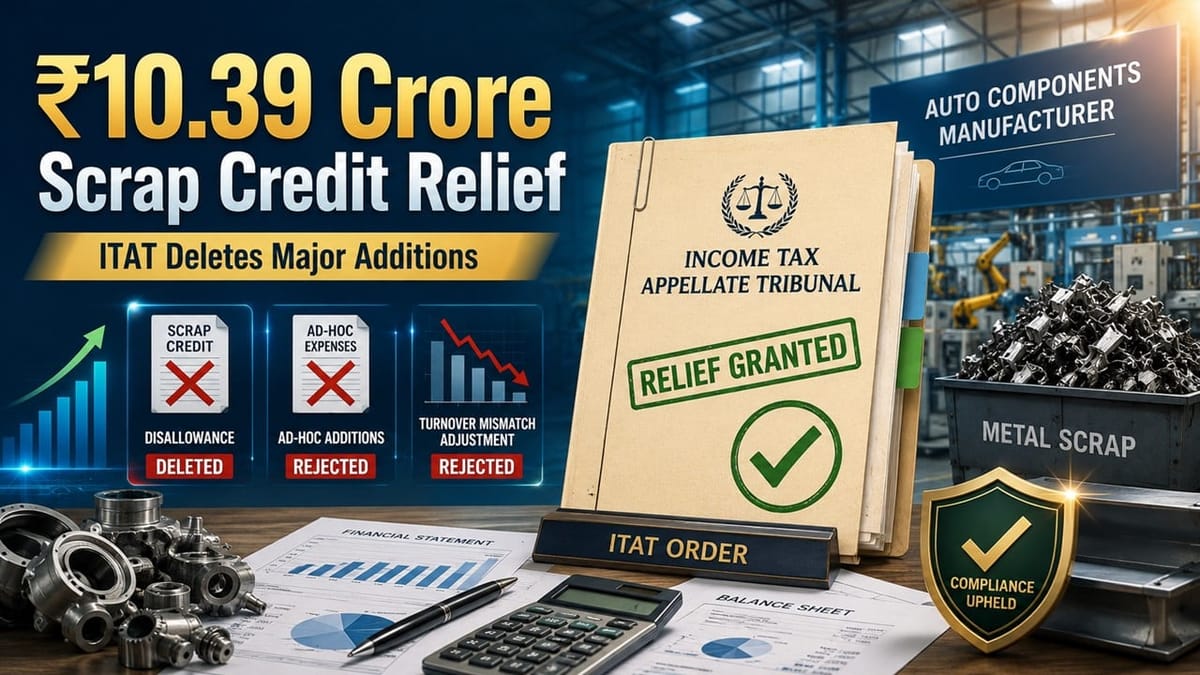

Scrap liability to M&M held genuine; turnover mismatch, staff welfare and other estimated additions quashed by Tribunal.

Meetu Kumari | Jun 20, 2026 |

Auto Components Manufacturer Got Rs 10.39 Crore Scrap Credit Disallowance Deleted; ITAT Rejects Ad-Hoc Expense Additions and Turnover Mismatch Adjustment

In case of any Doubt regarding Membership you can mail us at [email protected]

Join Studycafe's WhatsApp Group or Telegram Channel for Latest Updates on Government Job, Sarkari Naukri, Private Jobs, Income Tax, GST, Companies Act, Judgements and CA, CS, ICWA, and MUCH MORE!"