ITAT Deletes Section 50C Addition, Rejects Stamp Duty Value Where DVO Variation Was Within 15% Tolerance Limit.

Meetu Kumari | Jun 23, 2026 |

ITAT Discards Stamp Duty Value, Accepts Declared Sale Consideration

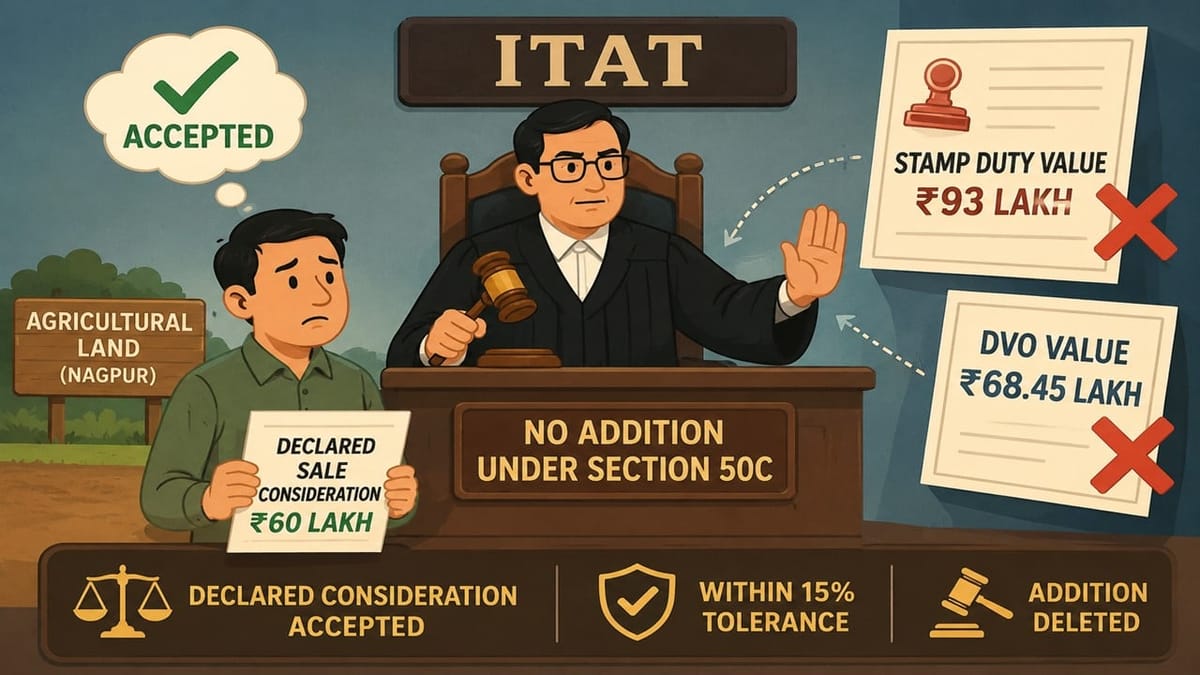

Nagpur ITAT held that where the difference between the actual sale consideration and the DVO’s valuation was less than 15%, no addition could be made under Section 50C. The Tribunal also ruled that the CIT(A) was not justified in directing adoption of the stamp duty value of Rs.93 lakh as the full value of consideration.

The assessee, Shri Bhupendra Abhimanyu Kukreja, sold an urban agricultural land situated at Mouza Nara, Nagpur, during AY 2016-17 for a consideration of Rs.60 lakh. The stamp valuation authority adopted the value of the property at Rs.93 lakh for stamp duty purposes. In the return of income, the assessee computed long-term capital gains on the basis of the actual sale consideration received.

During assessment proceedings, the Assessing Officer invoked Section 50C and referred the matter to the Departmental Valuation Officer (DVO) after the assessee objected to the stamp duty valuation. The DVO determined the fair market value of the property at Rs.68.45 lakh. Based on the difference between the DVO value and the declared sale consideration, the Assessing Officer made an addition of Rs.8.45 lakh to the assessee’s long-term capital gains.

The first appellate authority not only upheld the action but further directed the Assessing Officer to compute capital gains by adopting the stamp duty value of ₹93 lakh as the full value of consideration. Aggrieved, the assessee approached the ITAT.

The Tribunal allowed the appeal and deleted the entire addition. It observed that the DVO had valued the property at ₹68.45 lakh against the actual sale consideration of Rs.60 lakh, resulting in a variation of less than 13%. Such variation was within the permissible tolerance band recognized by judicial precedents and could reasonably arise due to estimation differences in valuation exercises.

Relying on its earlier decision in Yashoda Builders and Developers v. ACIT, the Tribunal reiterated that differences of less than 15% between the actual consideration and the DVO valuation fall within the acceptable tolerance range and do not justify additions under Sections 43CA or 50C. Since Section 50C operates on principles similar to Section 43CA, the same reasoning applied to the assessee’s case.

The Tribunal further found merit in the assessee’s objection to the DVO’s methodology. It noted that the DVO had not valued the land on an “as is where is” basis. Instead, the valuation assumed future development of the agricultural land into a plotted layout and estimated the value by considering hypothetical sale prices of developed plots after deducting projected development costs and developer profits. Therefore the Tribunal, such a hypothetical development model could not represent the fair market value of the property in its actual condition on the date of transfer.

The Bench also held that the CIT(A)’s direction to adopt the stamp duty value of Rs.93 lakh was contrary to the scheme of Section 50C(2), particularly when a DVO valuation had already been obtained. Thus, both the addition of Rs.8.45 lakh made by the Assessing Officer and the enhancement direction issued by the CIT(A) were deleted.

To Read Full Order, Download PDF Given Below

In case of any Doubt regarding Membership you can mail us at [email protected]

Join Studycafe's WhatsApp Group or Telegram Channel for Latest Updates on Government Job, Sarkari Naukri, Private Jobs, Income Tax, GST, Companies Act, Judgements and CA, CS, ICWA, and MUCH MORE!"