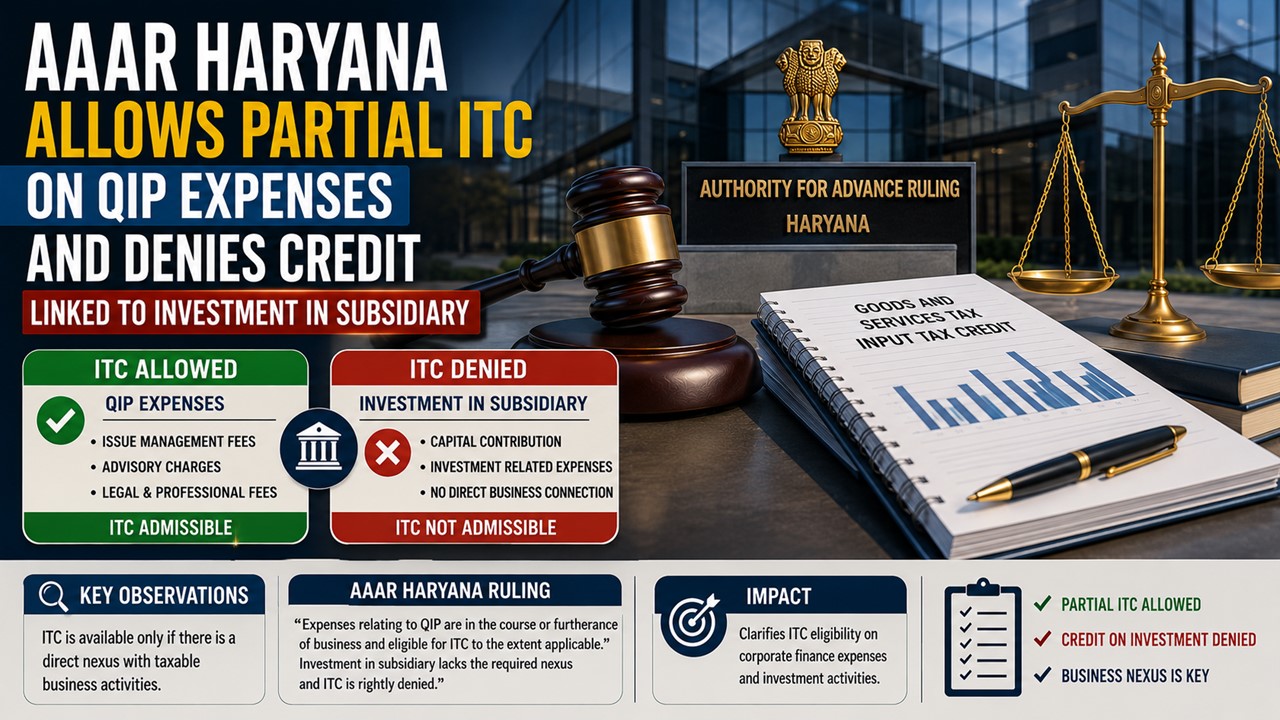

AAAR Haryana Allows Partial ITC on QIP Expenses And Denies Credit Linked to Investment in Subsidiary:

The Haryana Appellate Authority for Advance Ruling (AAAR) has partly allowed the appeal filed by M/s RHI Magnesita India Limited and held that Input Tax Credit on QIP would be available only on payment of borrowings

AAAR Holds GST Credit on QIP Services is not Available for Investment in Subsidiary Companies

AAAR Haryana Allows Partial ITC on QIP Expenses And Denies Credit Linked to Investment in Subsidiary

M/s RHI Magnesita India Limited approached the Haryana Appellate Authority for Advance Ruling seeking clarification regarding the admissibility of Input Tax Credit (ITC) on various professional and intermediary services procured in connection with its Qualified Institutional Placement (QIP). The company had raised funds through QIP and utilised the proceeds towards repayment of borrowings and for investment in its subsidiary, Dalmia OCL Limited.

The appellant is engaged in the manufacture and supply of refractory products and had undertaken a Qualified Institutional Placement in accordance with the Securities and Exchange Board of India (Issue of Capital and Disclosure Requirements) Regulations, 2018. In connection with the issue, the company availed services of investment bankers, legal advisors, registrars and other intermediaries and claimed Input Tax Credit on the GST charged on these services.

The Authority for Advance Ruling, Haryana had earlier denied the claim of ITC. Aggrieved by the ruling, the appellant preferred an appeal before the Appellate Authority under Section 100(1) of the Central Goods and Services Tax Act, 2017 and the Haryana Goods and Services Tax Act, 2017.

Before the Appellate Authority, the appellant contended that the expenditure incurred for raising capital through QIP was integrally connected with its business activities and, therefore, qualified for credit under Section 16(1) of the CGST Act, 2017.

The Appellate Authority observed that under Section 16(1) of the CGST Act, a registered person is entitled to avail Input Tax Credit on goods or services used or intended to be used in the course or furtherance of business. However, the Appellate Authority held that the part of the QIP proceeds invested in Dalmia OCL Limited, the subsidiary company, did not have a direct connection with the business operations of the appellant. Accordingly, Input Tax Credit for the services relatable to that portion of the funds was held to be inadmissible.

[related id="424197 "]

In view of the above findings, the Haryana AAAR partly upheld Advance Ruling No. HR/HAAR/30/2023-24 dated 21.02.2024 and modified the ruling by holding that ITC on QIP-related services shall be available only to the extent for repayment or pre-payment of borrowings, the appeal filed by M/s RHI Magnesita India Limited was partly allowed.

For full information, refer to the document given below.

About Author

Saima

Content Writer

Saima is a Law graduate with a passion for research and content writing. She writes for Finance, Taxation and Legal Updates at Studycafe.in, simplifying complex legal decisions by the ITAT, High Court, AAR and GSTAT into uncomplicated and clear explanations.

Saima is a Law graduate with a passion for research and content writing. She writes for Finance, Taxation and Legal Updates at Studycafe.in, simplifying complex legal decisions by the ITAT, High Court, AAR and GSTAT into uncomplicated and clear explanations.

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 271

271My Recent Articles

- ITAT Condones 185 Day Delay And Grants Fresh Opportunity to Defunct PSU Premium

- ITAT Quashes Reassessment Proceedings for Approval from Wrong AuthorityPremium

- ITAT Quashes Reassessment as AO Made Additions on Issues Unrelated to Reasons Under Section 148APremium

- ITAT Holds Section 148 Notice Issued After 1 April 2021 for AY 2015–16 As Time-BarredPremium

- ITAT Remands Unexplained Money Addition As PAN and Identity Were Fraudulently MisusedPremium

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts