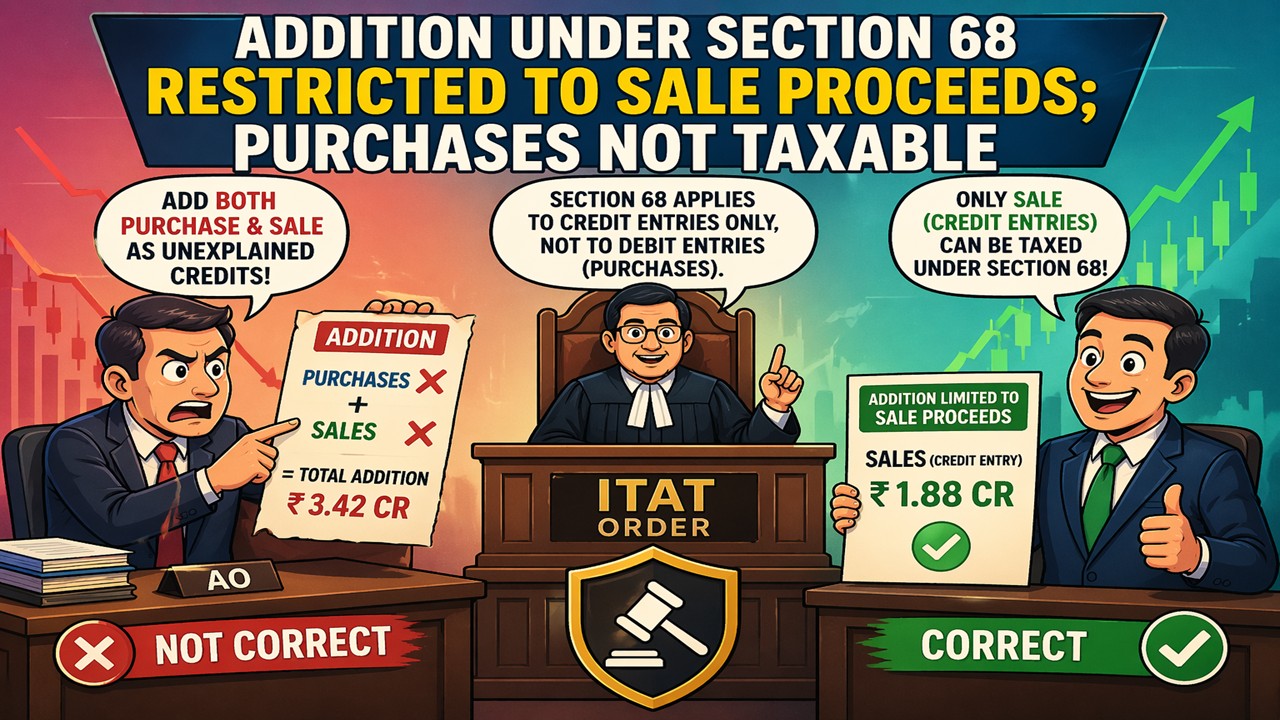

Addition under Section 68 Restricted to Sale Proceeds; Purchases Not Taxable:

Only sale (credit entries) taxable under Section 68, not purchases; ITAT upheld limited addition and dismissed Revenue’s appeal.

Section 68 applies only to credit entries, not debit transactions.

Addition under Section 68 Restricted to Sale Proceeds; Purchases Not Taxable

The AO considered both the buying and selling of shares as fraudulent and made a complete addition. However, the CIT(A) concluded that only sales (credit entries) can be taxed under section 68 but not purchases (debit entries), thus limiting the addition. The ITAT agreed to this interpretation and rejected the appeal by the Revenue.

[related id="417605."]

Facts The assessee had filed their return of income and declared a loss amounting to ₹4.17 crore. Section 148 was used to reopen the case due to the fact that the assessee had taken accommodation entries through penny stock transactions in Still Exchange Ltd and Monotype India Ltd. The AO added both purchase and sale transactions as bogus, & a total addition of Rs 3.42 cr was made. Even though the assessee did not co-operate, the CIT(A) restricted the addition to sale proceeds of Rs 1.88 cr & treated them as unexplained credits u/s 68. Issue Whether the AO was justified in making the addition of both purchase and sale value of alleged bogus share transactions or whether the addition should be restricted only to credit entries (sale proceeds) under Section 68. Court's observation The ITAT agreed with the CIT(A) that section 68 applies only to credit entries, not to debits. As purchase transactions are debits, the same cannot be taxed as unexplained credits, and the A.O. has failed to demonstrate that the purchase entries were credited in the books. The Tribunal further observed that ideally only the profit/loss element could have been taxed, but since the assessee did not file an appeal, the CIT order was sustained. The ITAT’s judgement Revenue’s appeal was dismissed by ITAT; the addition was restricted to the sale consideration, as per the CIT(A) order. Key Highlight of the judgement "In determining income… the addition should be restricted to credit entries only; the purchase values are always debited in the books of account hence, purchase transactions could not be treated as credit entries under section 68." When computing income, only credit entries should be taken into consideration for making the additions. The purchase values will always be debited in the books of accounts. Therefore, the purchase transaction cannot be considered as credit entries under Section 68. Importance of the Case:- Defines Section 68 as Crediting Transactions Only and Not Debiting Transactions.

- Reaffirms core accounting standards in tax assessments.

- Limits A.O. from making random additions in penny-stock/force-bogus Transaction Cases.

- Suggests that only real income, i.e., profit/loss, should ideally be taxed.

About Author

Aishwarya Singh

Legal Content Writer

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 92

92My Recent Articles

- ITAT Allows Fresh Opportunity to Trust Seeking Income Tax Exemption

- ITAT Upholds Section 11 Exemption for Gujarat Maritime Board Despite Commercial Receipt Allegations

- ITAT Ahmedabad Deletes Rs 52 Lakh Addition based on information received through Insight Portal

- ITAT Deletes Rs. 1.82 Crore Addition on Cash Held for Payments to Farmers During Demonetisation

- Company Penalised by ROC Delhi for Failure to File AOC-4 CFS Within Prescribed Timeline

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

Recent Posts

All Posts