Applicability of Section 44AA/44AB/44AD of Income Tax Act, 1961-2021

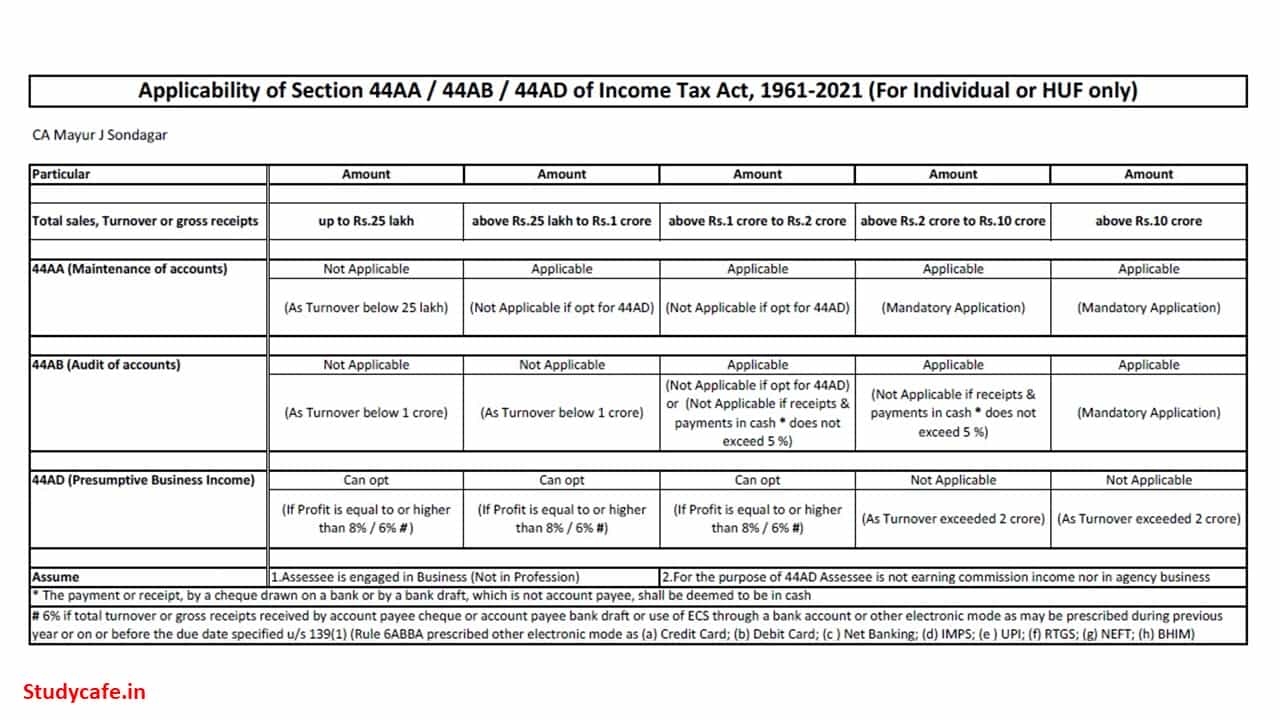

Applicability of Section 44AA/44AB/44AD of Income Tax Act, 1961-2021 Particular Amount Amount Amount Amount Amount Total sales, Turnover or gross rec…

Applicability of Section 44AA/44AB/44AD of Income Tax Act, 1961-2021

* The payment or receipt, by a cheque drawn on a bank or by a bank draft, which is not account payee, shall be deemed to be in cash

# 6% if total turnover or gross receipts received by account payee cheque or account payee bank draft or use of ECS through a bank account or other electronic mode as may be prescribed during previous year or on or before the due date specified u/s 139(1) (Rule 6ABBA prescribed other electronic mode as (a) Credit Card; (b) Debit Card; (c ) Net Banking; (d) IMPS; (e ) UPI; (f) RTGS; (g) NEFT; (h) BHIM)

| Particular | Amount | Amount | Amount | Amount | Amount |

| Total sales, Turnover or gross receipts | up to Rs.25 lakh | above Rs.25 lakh to Rs.1 crore | above Rs.1 crore to Rs.2 crore | above Rs.2 crore to Rs.10 crore | above Rs.10 crore |

| 44AA (Maintenance of accounts) | Not Applicable | Applicable | Applicable | Applicable | Applicable |

| (As Turnover below 25 lakh) | (Not Applicable if opt for 44AD) | (Not Applicable if opt for 44AD) | (Mandatory Application) | (Mandatory Application) | |

| 44AB (Audit of accounts) | Not Applicable | Not Applicable | Applicable | Applicable | Applicable |

| (As Turnover below 1 crore) | (As Turnover below 1 crore) | (Not Applicable if opt for 44AD) or (Not Applicable if receipts & payments in cash * does not exceed 5 %) | (Not Applicable if receipts & payments in cash * does not exceed 5 %) | (Mandatory Application) | |

| 44AD (Presumptive Business Income) | Can opt | Can opt | Can opt | Not Applicable | Not Applicable |

| (If Profit is equal to or higher than 8% / 6% #) | (If Profit is equal to or higher than 8% / 6% #) | (If Profit is equal to or higher than 8% / 6% #) | (As Turnover exceeded 2 crore) | (As Turnover exceeded 2 crore) | |

| Assume | 1.Assessee is engaged in Business (Not in Profession) | 2.For the purpose of 44AD Assessee is not earning commission income nor in agency business | |||

About Author

CA Mayur J Sondagar

Proprietor

Mumbai, Maharashtra, India

Mumbai, Maharashtra, India 12

12My Recent Articles

- Income Tax Return and Audit Due Date for AY 2021-22

- Various Examples Discussing Income Tax Audit Applicability

- GST QRMP vs Non-QRMP Brief Analysis

- Discussion on various provisions related to GST E-Way Bill

- Existing Tax Regime v/s New Tax Regime 115BAC (For Resident Individual Age Below 60)

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts