Various Examples Discussing Income Tax Audit Applicability

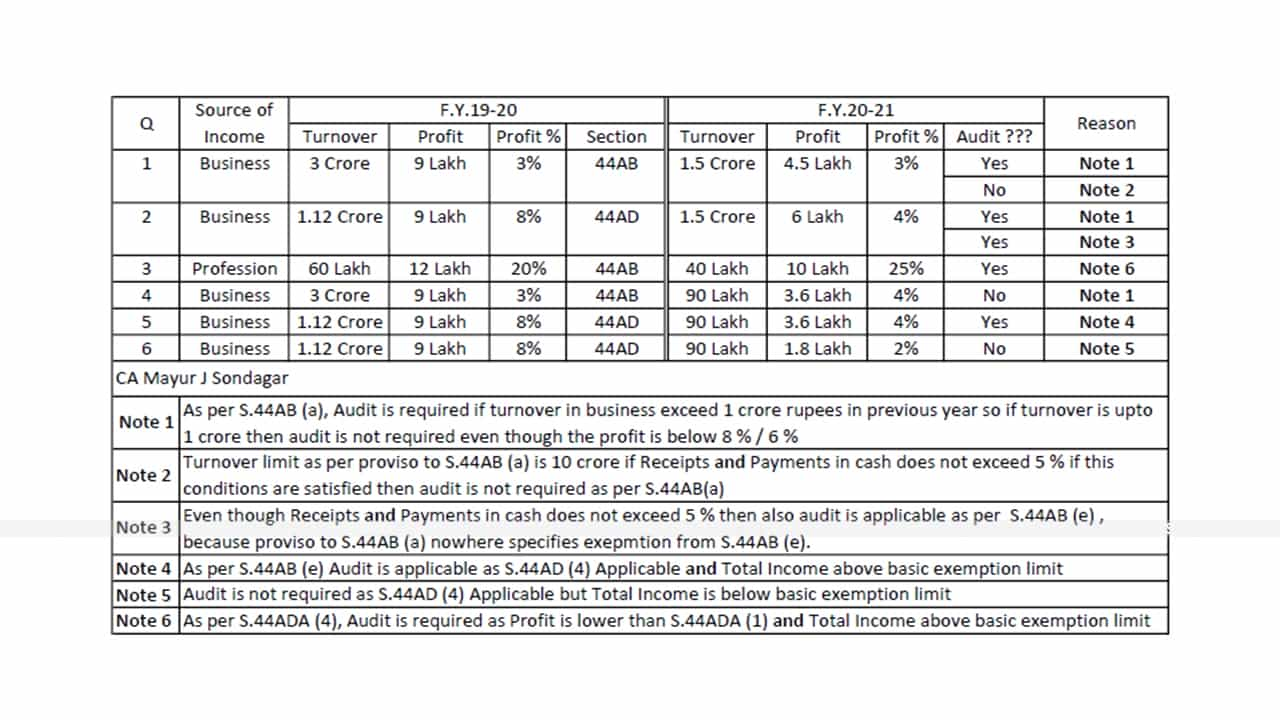

Various Examples Discussing Income Tax Audit Applicability Q Source of Income F.Y.19-20 F.Y.20-21 Reason Turnover Profit Profit % Section Turnover Pr…

Various Examples Discussing Income Tax Audit Applicability

Note 1 As per S. 44AB (a), Audit is required if turnover in business exceeds 1 crore rupees in the previous year so if turnover is up to 1 crore then an audit is not required even though the profit is below 8 % / 6 %

Note 2 Turnover limit as per proviso to S.44AB (a) is 10 crore if Receipts and Payments in cash does not exceed 5 % if these conditions are satisfied then an audit is not required as per S.44AB(a)

Note 3 Even though Receipts and Payments in cash does not exceed 5 % then also audit is applicable as per S.44AB (e), because proviso to S.44AB (a) nowhere specifies exemption from S.44AB (e).

Note 4 As per S.44AB (e) Audit is applicable as S.44AD (4) Applicable and Total Income above the basic exemption limit

Note 5 Audit is not required as S.44AD (4) Applicable but Total Income is below the basic exemption limit

Note 6 As per S.44ADA (4), Audit is required as Profit is lower than S.44ADA (1) and Total Income above the basic exemption limit

| Q | Source of Income | F.Y.19-20 | F.Y.20-21 | Reason | ||||||

| Turnover | Profit | Profit % | Section | Turnover | Profit | Profit % | Audit ??? | |||

| 1 | Business | 3 Crore | 9 Lakh | 3% | 44AB | 1.5 Crore | 4.5 Lakh | 3% | Yes | Note 1 |

| No | Note 2 | |||||||||

| 2 | Business | 1.12 Crore | 9 Lakh | 8% | 44AD | 1.5 Crore | 6 Lakh | 4% | Yes | Note 1 |

| Yes | Note 3 | |||||||||

| 3 | Profession | 60 Lakh | 12 Lakh | 20% | 44AB | 40 Lakh | 10 Lakh | 25% | Yes | Note 6 |

| 4 | Business | 3 Crore | 9 Lakh | 3% | 44AB | 90 Lakh | 3.6 Lakh | 4% | No | Note 1 |

| 5 | Business | 1.12 Crore | 9 Lakh | 8% | 44AD | 90 Lakh | 3.6 Lakh | 4% | Yes | Note 4 |

| 6 | Business | 1.12 Crore | 9 Lakh | 8% | 44AD | 90 Lakh | 1.8 Lakh | 2% | No | Note 5 |

About Author

CA Mayur J Sondagar

Proprietor

Mumbai, Maharashtra, India

Mumbai, Maharashtra, India 12

12My Recent Articles

- Income Tax Return and Audit Due Date for AY 2021-22

- Applicability of Section 44AA/44AB/44AD of Income Tax Act, 1961-2021

- GST QRMP vs Non-QRMP Brief Analysis

- Discussion on various provisions related to GST E-Way Bill

- Existing Tax Regime v/s New Tax Regime 115BAC (For Resident Individual Age Below 60)

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts