Discussion on various provisions related to GST E-Way Bill

Discussion on various provisions related to GST E-Way Bill Section 68: Inspection of goods in movement (1) The Government may require person in charg…

Table of Contents

Discussion on various provisions related to GST E-Way Bill

Section 68: Inspection of goods in movement

(1) The Government may require person in charge of a conveyance carrying any consignment of goods of value exceeding such amount as may be specified

to carry with him such documents & such devices as may be prescribed.

(2) The details of documents required to be carried under sub-section (1) shall be validated in such manner as may be prescribed

(3) Where any conveyance referred to in sub-section (1) is intercepted by the proper officer at any place, he may require person in charge of said

conveyance to produce documents prescribed under said sub-section and devices for verification, and said person shall be liable to produce documents and devices and also allow the inspection of goods.

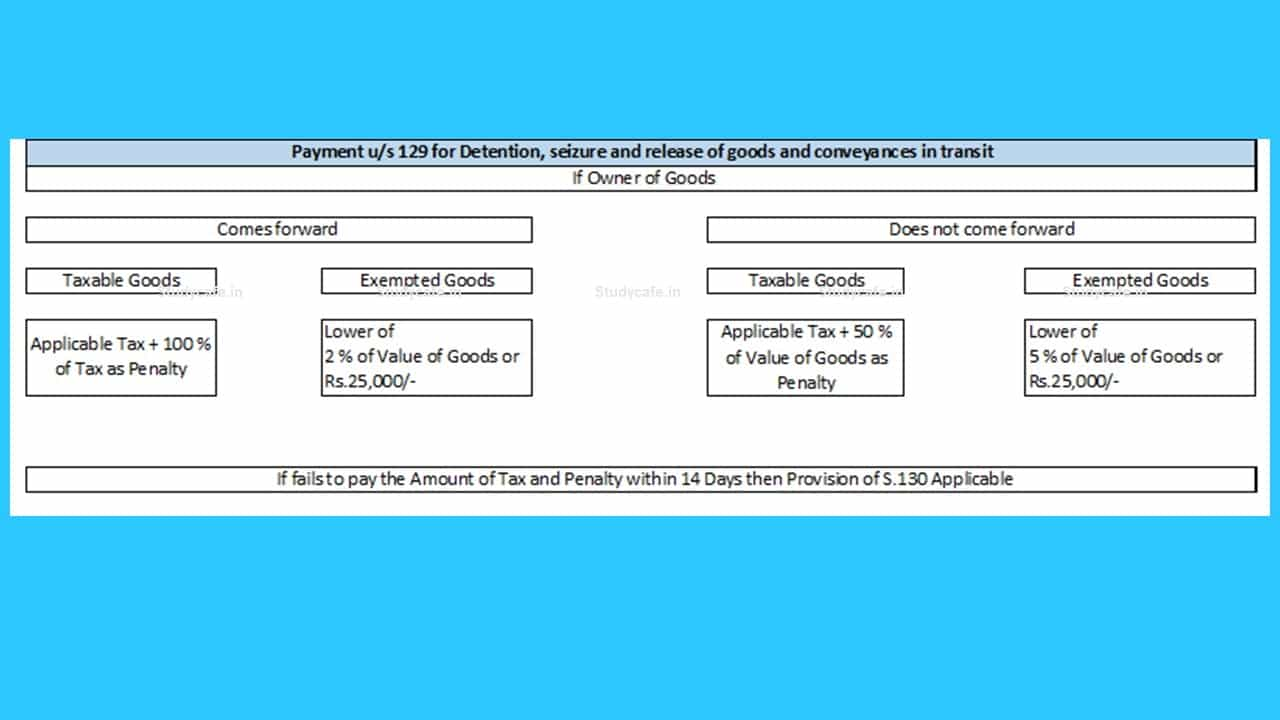

No order for confiscation of goods or conveyance, or for imposition of penalty, shall be issued without giving person an opportunity of being heard

In case neither the owner of the goods nor any person other than the owner of the goods comes forward to make the payment of tax, penalty and fine imposed and get the goods or conveyance released within the me specified in FORM GST MOV 11, the proper officer shall auc on the goods and/or conveyance by a public auction and remit the sale proceeds to the account of the Central Government

A summary of every order in FORM GST MOV-09 and FORM GST MOV-11 shall be uploaded electronically in FORM GST-DRC-07 on common portal

Rule 138 to 138D of the Central Goods and Services Tax Rules, 2017 lay down, in detail, the provisions relating to e-way bills

Rule 138

- Information to be furnished prior to commencement of movement of goods and generation of e-way bill

- E-way bill shall be valid for movement of goods by road only if information in Part-B of FORM GST EWB-01 has been furnished

- E-way bill may be cancelled electronically on the common portal within 24 hours of generation of the e-way bill

- Unique number generated under sub-rule (1) shall be valid for a period of 15 days for updation of Part B of FORM GST EWB-01

- Validity of the e-way bill may be extended within 8 hours from the time of its expiry

- No e-way bill is required to be generated where

- Goods are being transported by a non-motorised conveyance

- Goods being transported are alcoholic liquor for human consumption, petroleum crude, high speed diesel, motor spirit (commonly known as petrol), natural gas or aviation turbine fuel

- Supply of goods being transported is treated as no supply under Schedule III of the Act

- Consignor of goods is the Central Government, Government of any State or a local authority for transport of goods by rail

- Goods being transported are specified below

- Liquefied petroleum gas for supply to household and non domestic exempted category (NDEC) customers

- Natural or cultured pearls & precious or semi-precious stones; precious metals & metals clad with precious metal

- Jewellery, goldsmiths‘ and silversmiths‘ wares and other articles

- Currency

- Kerosene oil sold under PDS

- Postal baggage transported by Department of Post

- Used personal and household effects

- Coral, unworked and worked coral

Rule 138A

- Documents and devices to be carried by a person-in-charge of a conveyance.

- Invoice or bill of supply or delivery challan, as the case may be; and

- Copy of the e-way bill in physical form or the e-way bill number in electronic form or mapped to a Radio Frequency Identification Device embedded on to the conveyance in such manner as may be notified by the Commissioner

Rule 138B

Verification of documents and conveyances.Rule 138C

- Inspection and verification of goods.

- Proper officer shall record online

- Summary report in Part A of FORM GST EWB-03 within 24 hours of such inspection

- Final report in Part B of FORM GST EWB-03 within 3 days of such inspection

Rule 138D

- Facility for uploading information regarding detention of vehicle.

- Where a vehicle has been intercepted and detained for a period exceeding thirty minutes, the transporter may upload the said information in FORM GST EWB-04 on the common portal

Payment u/s 129 for Detention, seizure and release of goods and conveyances in transit

Section 130: Confiscation of goods or conveyances and levy of penalty:

(i) Supplies or Receives goods in contravention of any provisions of this Act or rules made thereunder with intent to evade tax payment (ii) Does not account for any goods on which he is liable to pay tax under this Act (iii) Supplies any goods liable to tax under this Act without having applied for registration (iv) Contravenes any of the provisions of this Act or the rules made thereunder with intent to evade tax payment (v) Uses any conveyance as a means of transport for carriage of goods in contravention of the provisions of this Act or the rules made thereunder unless the owner of the conveyance proves that it was so used without the knowledge or connivance of the owner himself, his agent, if any, and the person in charge of the conveyance. then, all such goods or conveyances shall be liable to confiscation and the person shall be liable to penalty under section 122| Related FORMS | |

| FORM GST MOV-01 | Statement of the person in charge of the conveyance |

| FORM GST MOV-02 | Order for physical verification/inspection of the conveyance, goods, and documents |

| Requiring the person in charge of the conveyance to station the conveyance at the place mentioned in such order & allow the inspection of the goods. The proper officer shall, within 24 hours of the aforementioned issuance of FORM GST MOV-02, prepare a report in Part A of FORM GST EWB-03 and upload the same on the common portal | |

| FORM GST MOV-03 | Extension of time beyond 3 working days |

| Within a period of 3 working days from the date of issue of the order in FORM GST MOV-02, the proper officer shall conclude the inspection proceedings. Where circumstances warrant such time to be extended, he shall obtain written permission in FORM GST MOV-03 from the Commissioner or an officer authorized by him, for extension of time beyond 3 working days and a copy of the order of extension shall be served on the person in charge of the conveyance. | |

| FORM GST MOV-04 | Report of such physical verification |

| On completion of the physical verification/inspection of the conveyance and the goods in movement, the proper officer shall prepare a report of such physical verification in FORM GST MOV-04 and serve a copy of the said report to the person in charge of the goods and conveyance. The proper officer shall also record, on the common portal, the final report of the inspection in Part B of FORM GST EWB-03 within 3 days of such physical verification/inspection. | |

| FORM GST MOV-05 | Release order |

| Where no discrepancies are found after the inspection of the goods and conveyanc | |

| Where amount of tax & penalty as specified u/s 129 has been paid | |

| FORM GST MOV-06 | Order of detention |

| Where the proper officer is of the opinion that the goods and conveyance need to be detained u/s 129 | |

| FORM GST MOV-07 | Notice specifying the tax and penalty payable u/s 129 |

| The said notice shall be served on the person in charge of the conveyance | |

| FORM GST MOV-08 | Bond along with a security in the form of bank guarantee |

| The finalization of the proceedings under section 129 of the CGST Act shall be taken up on priority by the officer concerned and the security provided may be adjusted against the demand arising from such proceedings. | |

| FORM GST MOV-09 | Order of the amount of tax |

| Where any objections are filed against the proposed amount of tax and penalty payable, the proper officer shall consider such objections and thereafter, pass a speaking order in FORM GST MOV-09, quantifying the tax and penalty payable. | |

| FORM GST MOV-10 | Notice for confiscation of the goods and conveyance and imposition of penalty |

| In case the proposed tax & penalty are not paid within 7 days from the date of the issue of order of detention in FORM GST MOV-06, ac on u/s 130 of the CGST Act shall be initiated by serving a notice in FORM GST MOV10, proposing confiscaon of the goods | |

| FORM GST MOV-11 | An order of confiscation of goods |

| After taking into consideration the objections filed by the person in charge of the goods (owner or his representative), an order of confiscation of goods shall be passed, and the same shall be served on the person concerned | |

| Once the order of confiscation is passed, the title of such goods shall stand transferred to the Central Government. | |

| In the said order, a suitable time not exceeding 3 months shall be offered to make the payment of tax, penalty, and fine imposed in lieu of confiscation and get the goods released | |

| Once an order of confiscation of goods is passed in FORM GST MOV-11, the order in FORM GST MOV-09 passed earlier with respect to the said goods shall be withdrawn. | |

About Author

CA Mayur J Sondagar

Proprietor

Mumbai, Maharashtra, India

Mumbai, Maharashtra, India 12

12My Recent Articles

- Income Tax Return and Audit Due Date for AY 2021-22

- Various Examples Discussing Income Tax Audit Applicability

- Applicability of Section 44AA/44AB/44AD of Income Tax Act, 1961-2021

- GST QRMP vs Non-QRMP Brief Analysis

- Existing Tax Regime v/s New Tax Regime 115BAC (For Resident Individual Age Below 60)

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

Recent Posts

All Posts