Assessment Under Provisions of Section 153 A of IT Act, 1961

Assessment Under Provisions of Section 153 A of IT Act, 1961 SOME IMPORTANT FACTS RELATED TO ASSESSMENT UNDER SECTION 153A OF THE INCOME TAX ACT, 196…

Table of Contents

SOME IMPORTANT FACTS RELATED TO ASSESSMENT UNDER SECTION 153A OF THE INCOME TAX ACT, 1961.

As you are aware that provisions of Section 153A of the Income Tax Act, 1961 deals with assessment of an assessee in searched cases u/s. 132 of the IT Act, 1961. The Assessing Officer in this section allowed to assess income of an assessee for previous six assessment years preceding assessment year in which search happened. Please note that, the AO has not provided unfettered right for the assessment through this section. The main ingredient of assessment under this is the search should be conducted and on the basis of “incriminating materials” found during the search the AO must issue notice of Assessment to the assessee. It is right of an assessee to get final assessment order and department is not allowed to ask to assessee again and again for assessment for the same assessment year. Once assessment for an assessment year has closed for an assessee, this can be reopened only of valid and substantiate grounds. Since one should not be allowed to review its own actions and hence addition under Section 153A should be made only on the basis of valid material documents or requisition found during the Search on the premises of an assessee under Section 132. Under section 153A of the Act, an assessment has to be made in relation to the search or requisition, namely, in relation to material disclosed during the search or requisition. If in relation to any assessment year, no incriminating material is found, no addition or disallowance can be made in relation to that assessment year in the exercise of powers under section 153A of the Act and the earlier assessment shall have to be reiterated.SECTION 153A OF INCOME TAX ACT "ASSESSMENT IN CASE OF SEARCH OR REQUISITION"

153A. (1) Notwithstanding anything contained in section 139, section 147, section 148, section 149, section 151 and section 153, in the case of a person where a search is initiated under section 132 or books of account, other documents or any assets are requisitioned under section 132A after the 31st day of May, 2003, the Assessing Officer shall-(a) issue notice to such person requiring him to furnish within such period, as may be specified in the notice, the return of income in respect of each assessment year falling within six assessment years and for the relevant assessment year or years referred to in clause (b), in the prescribed form and verified in the prescribed manner and setting forth such other particulars as may be prescribed and the provisions of this Act shall, so far as may be, apply accordingly as if such return were a return required to be furnished under section 139;

(b) assess or reassess the total income of six assessment years immediately preceding the assessment year relevant to the previous year in which such search is conducted or requisition is made and for the relevant assessment year or years;

PROVIDED THAT the Assessing Officer shall assess or reassess the total income in respect of each assessment year falling within such six assessment years and for the relevant assessment year or years : PROVIDED FURTHER THAT assessment or reassessment, if any, relating to any assessment year falling within the period of six assessment years and for the relevant assessment year or years referred to in this sub-section pending on the date of initiation of the search under section 132 or making of requisition under section 132A, as the case may be, shall abate : PROVIDED ALSO THAT the Central Government may by rules made by it and published in the Official Gazette (except in cases where any assessment or reassessment has abated under the second proviso), specify the class or classes of cases in which the Assessing Officer shall not be required to issue notice for assessing or reassessing the total income for six assessment years immediately preceding the assessment year relevant to the previous year in which search is conducted or requisition is made and for the relevant assessment year or years: PROVIDED ALSO THAT no notice for assessment or reassessment shall be issued by the Assessing Officer for the relevant assessment year or years unless-(a) the Assessing Officer has in his possession books of account or other documents or evidence which reveal that the income, represented in the form of asset, which has escaped assessment amounts to or is likely to amount to fifty lakh rupees or more in the relevant assessment year or in aggregate in the relevant assessment years;

(b) the income referred to in clause (a) or part thereof has escaped assessment for such year or years; and

(c) the search under section 132 is initiated or requisition under section 132A is made on or after the 1st day of April, 2017.

EXPLANATION 1.-For the purposes of this sub-section, the expression "relevant assessment year" shall mean an assessment year preceding the assessment year relevant to the previous year in which search is conducted or requisition is made which falls beyond six assessment years but not later than ten assessment years from the end of the assessment year relevant to the previous year in which search is conducted or requisition is made. EXPLANATION 2.-For the purposes of the fourth proviso, "asset" shall include immovable property being land or building or both, shares and securities, loans and advances, deposits in bank account. (2) If any proceeding initiated or any order of assessment or reassessment made under sub-section (1) has been annulled in appeal or any other legal proceeding, then, notwithstanding anything contained in sub-section (1) or section 153, the assessment or reassessment relating to any assessment year which has abated under the second proviso to sub-section (1), shall stand revived with effect from the date of receipt of the order of such annulment by the Principal Commissioner or Commissioner: PROVIDED THAT such revival shall cease to have effect, if such order of annulment is set aside. Explanation.-For the removal of doubts, it is hereby declared that,-(i) save as otherwise provided in this section, section 153B and section 153C, all other provisions of this Act shall apply to the assessment made under this section;

(ii) in an assessment or reassessment made in respect of an assessment year under this section, the tax shall be chargeable at the rate or rates as applicable to such assessment year.

PROCEDURE OF ASSESSEMENT U/S. 153A After search and seizure proceedings at the premises of assessee has been completed the investigating officer have to submit Appraisal Report with the concerned A.O. for further action to be taken. 1. APPRAISAL REPORT- Internal document Conducting Directorate (Inv) prepares an appraisal report and forwards it to the A.O. The Appraisal Report contains indicative details such as:- Findings of search for premises covered u/s 132 and 133A of the Act,

- Inventory of books of accounts/documents etc., found / seized. Analysis of seized/impounded materials etc., analysis of computer data backup, core documents if any.

- Inventory of assets found and seized.

- Deciphering of incriminating material seized.

- Details of undisclosed income, assets.

- Summary of important statements recorded.

- Applied when there are unexplained credit and debit entries;

- Can be extended to cases where the credit appears not in the same account but in accounts of different person.

- The basic idea behind the peak credit theory is to avoid double addition and to bring only the actual income of the assessee to suffer tax, where there are large number of unexplained credit and debit entries.

- AO shall issue notice to the person searched to file Return of Income for six Assessment Years (Inserted by Finance Act, 2017) immediately preceding the year in which the search is conducted.

- AO to assess/ reassess total income for six assessment years (Inserted by Finance Act, 2017).

- Assessment/ reassessment in relation to any assessment year.

a) falling within the period of such six assessment years, (Inserted by Finance Act, 2017).

b)pending on the date of initiation of search shall abate.

- 153A contemplates issue of notice for 6 years (Inserted by Finance Act, 2017) preceding the search but not for the year of search or requisition and thus no return is required to be filed for the year of search u/s 153A. Only regular return u/s139 is to be filed.

- save as otherwise provided in this section, sec. 153B and sec. 153C, all other provisions of this Act shall apply to the assessment made under this section;

- in an assessment or reassessment made in respect of an assessment year under this section, the tax shall be chargeable at the rate or rates as applicable to such assessment year.

- No time limit prescribed for issue of notice u/s 153A.

- Section mentions about issue not service of notice.

- Section 153A speaks of the prescribed time and prescribed particulars, the rules & forms are yet to be prescribed.

- Income which has escaped assessment amounts to or is likely to amount to fifty lakh rupees or more in one year or in aggregate in the relevant four assessment years (falling beyond the sixth year);

- such income escaping assessment is represented in the form of asset;

- the income escaping assessment or part thereof relates to such year or years.

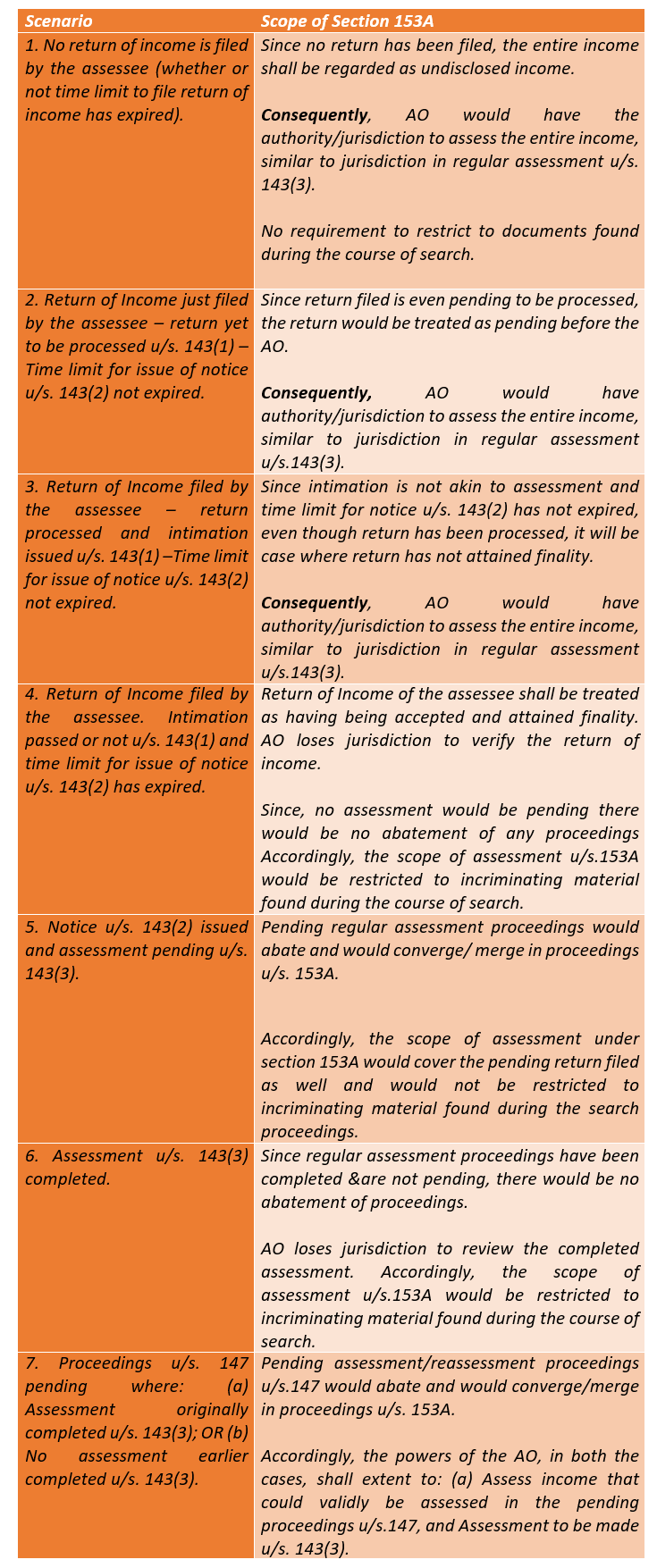

SOME ISSUES RELATED TO APPLICABILITY OF PROVISIONS OF SCETION 153A

- Whether pre-conditions of sec. 153A/132 are to be complied mandatorily?

- Whether proceedings may be continued without giving notice u/s 153A?

- Applicability of provisions of sec. 143 (2)

- Return filed u/s 153A is the original return.

JUDICIAL PRONOUNCEMENT -

- The Hon’ble Supreme Court of India in case of All Cargo Global Logistics Ltd. Vs. DCIT (23 taxmann.com103) has explained provisions of Section 153A as follows;

1. The final conclusion of the Mumbai ITAT Special Bench in the case of All Cargo Global Logistics Ltd. v. DCIT (supra), on the issue is as under:

1. The final conclusion of the Mumbai ITAT Special Bench in the case of All Cargo Global Logistics Ltd. v. DCIT (supra), on the issue is as under:

- In assessments that are abated, the AO retains the original jurisdiction as well as jurisdiction conferred on him u/s 153A for which assessments shall be made for each of the six assessment years separately;

- In other cases, in addition to the income that has already been assessed, the assessment u/s 153A will be made on the basis of incriminating material, which in the context of relevant provisions means –

a) books of account, other documents, found in the course of search but not produced in the course of original assessment, and

b) undisclosed income or property discovered in the course of search.

2. In relation to section 153A read with Section 263, the Bombay High Court in the case of CIT v. Murli Agro Products Ltd. (49 taxmann.com 172) has held that where there was nothing on record to suggest that any material was unearthed during search or during proceedings initiated under section 153A showing that certain relief in form of deduction was wrongly allowed to assessee, Commissioner could not invoke jurisdiction under section 263 on ground that assessment order passed under section153A, read with section 143(3) was erroneous or prejudicial to interest of revenue.SECTION 153B OF THE IT ACT, 1961

Time limit for completion of assessment u/s153A/153C: 1. 153(A): In case of person searched:- 21 months* from the end of the financial year in which last of the authorization for search u/s 132 or requisition u/s 132A was executed. Similar time limit shall apply in respect of the year of search also.

*18 months from 1 st day of April, 2018 (FY 2018-19)

*12 months from 1 st day of April, 2019 (FY 2019-20)

Eg. For AY 2017-18 (FY 2016-17) – Dec 2018 (21 months)

For AY 2018-19 (FY 2017-18) – Oct 2019 (18 months)

For AY 2019-20 (FY 2018-19) – March 2020 (12 months)

3. If it involves TP (transfer pricing), then time limit increases by one year. 4. The period of limitation of 21/ 18/ 12 months to start from the last panchnama drawn. 5. This section also provides certain exclusions while computing the period of limitation for completion of assessment or reassessment. (Eg: application made before settlement commission; application made before AAR.) 6. If after exclusion, the period of limitation available to the Assessing Officer for making an order of assessment or reassessment, is less than sixty days, such remaining period shall be extended to sixty days. 7. Section 153 D No AO below the rank of JCIT can pass the Order except with the prior approval of JCITSOME ISSUED U/S. 153B

1. Last authorization or last panchnama? CIT Vs Sh. Anil Minda ITA No.582, 527, 593, 605, 618, 772 of 2009 authorization referred to in sub-Section (1) would be that authorization which is executed on the conclusion of search as recorded in the last panchnama. Therefore, by this deeming provision, even an authorization which may not be otherwise the last authorization would become last authorization, if that is executed and if the panchnama in respect thereto is drawn last. 2. [2009] 308 ITR 116(Del) CIT vs. Deepak Aggarwal- last panchnama to be taken into consideration for the purpose of reckoning the limitation period.

- revocation order for the purpose of continuing the search did not amount to execution of a search when no asset is seized under that order and there is only revocation of the prohibitory order passed earlier.

SECTION 153C OF THE IT ACT, 1961

- Where the AO is satisfied that any money, bullion, jewellery or other valuable article documents seized belongs to a person other than the person referred to u/s 153A, the same shall be handed over to the AO having jurisdiction over such other person; and

- that AO shall proceed against each such other person, issue notice and assess or reassess the income of the other person in accordance with the provisions of section 153A, if, that AO is satisfied that the books of account or documents or assets seized or requisitioned have a bearing on the determination of the total income of such other person (for six assessment years immediately preceding the assessment year relevant to the previous year in which search is conducted or requisition is made) for the relevant assessment year or years referred to in sub-section (1) of section 153A.

SOME ISSUED U/S. 153C

1. Reasons to be recorded to reach at the satisfaction Supreme Court in Amity Hotels (P) Ltd. 272 ITR 75, held that : the reasons must be recorded by the Assessing Officer having jurisdiction over the assessee who had been searched before issuing the notice u/s 158BD of the Act. The aforesaid view has been reiterated by this Court in the case of CIT Vs. Karan Engg. P. Ltd. and Janki Exports International Vs. UOI, 193 CTR 730. 2. Belongs to assessee? Meghmani Organics Ltd. vs DCIT 129 TTJ 255 -The prerequisite for initiating proceedings u/s. 153C of the Act is that any money, bullion, jewellery or other valuable articles or things or documents seized or requisitioned belong to a person other than person in whose case warrant of authorizations is issued u/s. 132(1) of the Act. Since none of the documents belongs to the assessee, though they may be referable to the work of the assessee the same cannot be considered as "belonging to the assessee. 3. Where no material seized other than statement recorded-whether 153C/158BD can be invoked? Held no CIT VS. Late Sh. Raj Pal Bhatia, ITA 276 OF 2009, Date of decision29.11.2010, DELHI (HC):- no Assessment u/s 158BD can be invoked merely on the basis of Statement of a person in whose premises search was conducted as the statement is not in the nature of document which was found during search.

- Therefore, it cannot be said that the statement was, seized "during the search and thus, would not qualify the expression “document” having been seized during the search. In such a scenario, proper course of action was reassessment u/s147readwith section 148 of the Act.

- Both the Assessing Officer i.e., the AO of the original assesse and AO issuing notice u/s.153C has to place his satisfaction.

- Such satisfaction should be expressive and a speaking one.

- Assessing Officer should demonstrate that the seized books of accounts/documents/assets have any impact on determination of total income of such other person.

- Satisfaction shall be given for each assessment year of such other person proposed u/s153C.

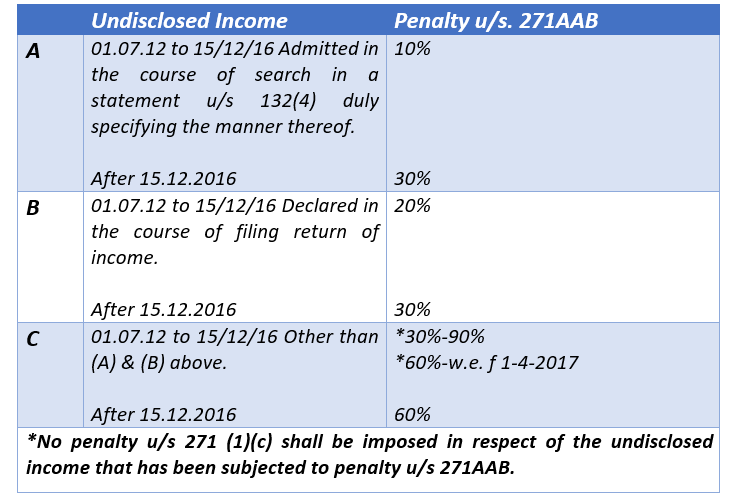

PENALTY U/S. 271AAB

SOME MORE IMPORTANT JUDICIAL PRONOUNCEMENTS

Case laws on ‘Incriminating material’ Though the majority of the judicial precedents, indicates that the Assessing Officer, while framing assessment under section 153A of the Act cannot make the addition/disallowance de-hors any ‘incriminating’ material, yet the said view has always been challenged by the Revenue on one count or the other and thus, the said controversy is yet to be settled by the Hon’ble Supreme Court. 1. CIT v. Kabul Chawla [T S-494-HC-2015(DEL)] The legal position relating to assessment under section 153A of the Act has been examined in great detail by the Hon’ble Delhi High Court in the case of Kabul Chawla(supra)and the following principles thereof has, after analyzing host of decisions, been succinctly laid down by the Hon’ble Court: “Summary of the legal position 37. On a conspectus of Section 153A (1) of the Act, read with the provisos thereto, and in the light of the law explained in the aforementioned decisions, the legal position that emerges is as under:i) Once a search takes place under Section 132 of the Act, notice under Section153A (1) will have to be mandatorily issued to the person searched requiring him to file returns for six AYs immediately preceding the previous year relevant to the AY in which the search takes place.

ii) Assessments and reassessments pending on the date of the search shall abate. The total income for such AYs will have to be computed by the AOs as a fresh exercise.

iii) The AO will exercise normal assessment powers in respect of the six years previous to the relevant AY in which the search takes place. The AO has the power to assess and reassess the 'total income' of the aforementioned six years in separate assessment orders for each of the six years. In other words, there will be only one assessment order in respect of each of the six AYs “in which both the disclosed and the undisclosed income would be brought to tax”.

iv) Although Section 153 A does not say that additions should be strictly made on the basis of evidence found in the course of the search, or other post-search material or information available with the AO which can be related to the evidence found, it does not mean that the assessment “can be arbitrary or made without any relevance or nexus with the seized material. Obviously, an assessment has to be made under this Section only on the basis of seized material.”

v) In absence of any incriminating material, the completed assessment can be reiterated and the abated assessment or reassessment can be made. The word 'assess' in Section153A is relatable to abated proceedings (i.e., those pending on the date of search) and the word 'reassess' to completed assessment proceedings.

vi) Insofar as pending assessments are concerned, the jurisdiction to make the original assessment and the assessment under Section 153A merges into one. Only one assessment shall be made separately for each AY on the basis of the findings of the search and any other material existing or brought on the record of the AO.

vii) Completed assessments can be interfered with by the AO while making the assessment under Section 153 A only on the basis of some incriminating material unearthed during the course of search or requisition of documents or undisclosed income or property discovered in the course of search which were not produced or not already disclosed or made known in the course of original assessment.

2. Smt. Dayawanti Gupta v. CIT [TS-5978-HC-2016(DELHI)-O] In the case of Dayawanti Gupta (supra), the Hon’ble Delhi High Court, after considering the decision of Kabul Chawla (supra), held that, in the facts of the case, the statement recorded under section 132(4) of the Act during the course of search proceedings, in the absence of any other material, would in itself constitute ‘incriminating’ material giving leeway to the Assessing Officer to make addition/disallowance. The aforesaid decision of Dayawanti Gupta, perhaps appears to be a sword for the Revenue to counter the principles laid down in the decision of Kabul Chawla (supra). 3. PCIT v. Meeta Gutgutia: [T S-199-HC-2017(DEL)] Recently, the Delhi High Court in the case of Meeta Gutgutia (supra) had an occasion to deal with the above decision of Dayawanti Gupta. The Delhi High Court after considering the entire gamut of the facts of the case held that the decision of the Court in the case of Dayawanti Gupta (supra) proceeded on the peculiar facts of the said case and the said decision in no way dilutes the dictum laid down in the case of Kabul Chawla(supra). The said position has been reiterated by the Hon’ble Delhi High Court recently in the case of Pr.CIT v. Best Infrastructure (India) Pvt Ltd [TS-5668-HC-2017(DELHI)-O]. 4. The Hon’ble Ahmedabad Tribunal in the case of Dr. Mansukh Kanjibhai Shahv. ACIT(129ITD376) has held that once the warrant of authorization or requisition is issued and search is conducted & Panchanama is drawn, all the relevant six assessment years would get reopened irrespective of any incriminating material is found or not in respect of any particular assessment year falling within the relevant six assessment years. 5. The Hon’ble Delhi High Court in the case of CIT v. Anil Kumar Bhatia (211 Taxman453) has held that even if assessment order had already been passed in respect of all or any of those six assessment years, either u/s. 143(1)(a) or u/s. 143(3) prior to intimation of search/ requisition, still Assessing Officer is empowered to reopen those proceedings u/s. 153A without any fetters and reassess total income taking note of undisclosed income, if any, unearthed during search. 6. Regency Mahavir Properties v. Assistant Commissioner of Income-tax, CenCir. 1, Thane[2018] 89 taxmann.com 444 (Mumbai – Trib.) Section 69, read with section 153A, of the Income tax Act, 1961 – Unexplained investment (On money) Assessment years 2007-08and2010-11–Whether no addition under section 69 can be made in case of assessee on basis of documents being found from premises of the third party where neither name of assessee was mentioned nor any document found evidencing fact that assessee had paid any cash as on-money to said party–Held,yes [Paras 12 and 13] [In favour of assessee]. 7. One important question arise here Does AO has the right to assess total income? Hon’ble Bombay High Court in the case of Continental Warehousing Corporation(NhavaSheva) Ltd. (supra), wherein considering the judgment of the Special Bench of the Mumbai Tribunal in the case of All Cargo Global Logistics 137 ITD 287(SB) (Mum), considered this issue that, once assessment has attained finality, then the assessing officer while passing independent assessment order under section 153A/143(3) of the Act could not disturb the assessment order which has attained finality unless the material gathered in the course of search under section132/153A of the Act established that the finality attained in the assessment were contrary to the facts unearthed during the course of searchCONCLUSION:

The controversy qua scope of addition/disallowance under section 153A of the Act being restricted to the ‘incriminating’ material’ as answered by the Hon’ble Delhi High Court in the case of Kabul Chawla (supra), which according to the Revenue was disturbed by the Dayawanti Gupta (supra), has been reconciled and reiterated in the case of Meeta Gutgutia(supra). The decision of Kabul Chawla (supra), though, has been challenged by the Revenue before the Supreme Court and the same is pending adjudication, but since there is no stay of operation by the Supreme Court, the said decision of Kabul Chawla (supra) would continue to hold the field till the time controversy is put to rest by the Supreme Court. An Assessing Officer before issuing notice under Section 153A should keep in mind below mentioned points;- Systematically arrange and make analysis of all the seized documents.

- Sort the documents assessee wise, assessment year wise and premises wise.

- Sort the documents having financial relevance and financially irrelevant.

- If the documents are financially relevant, ascertain how they are explainable vis-a-vis books of accounts or other details available with the Income Tax Department or are found / seized from the premises searched or surveyed.

- See if the explanation is available about all the records available with the Income tax department.

- Offer Peak Credits as undisclosed income, if any.

- Return of income u/s153A should be filed judiciously after consideration of records and material lying with income tax department.

- Where any undisclosed income is offered in the return filed u/s153A then the expenditure incurred to earn that income may also be claimed.

- File returns under protest if required notices are not properly issued &challenge the validity of proceedings at the time of Assessments itself.

About Author

FCS DEEPAK P. SINGH

Manager Legal & Compliance

SBI GENERAL INSURANCE COMPANY LIMITED

SBI GENERAL INSURANCE COMPANY LIMITED Mumbai, Maharashtra, India

Mumbai, Maharashtra, India 53

53My Recent Articles

- Surveyor Cannot Apply Deductions Arbitrarily On Amount Of Assessed Loss: Supreme Court Of India

- Insurance Company Cannot Impose Condition That Will Impossible To Comply By Insured

- Mergers & Acquisitions- Under Provisions of ITA,1961

- The Disputes between Landlord & Tenant Governed by Transfer of Property Act 1882 are Arbitrable in Nature

- Damage Caused by the Insurers Taking Possession of Insured Premises & Judicial Opinions

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts