Big Change in Calculation of House Property Income [Budget 2025]:

![Big Change in Calculation of House Property Income [Budget 2025]](https://assets.studycafe.in/uploads/2025/02/Calculation-of-House-Property-Income.jpg)

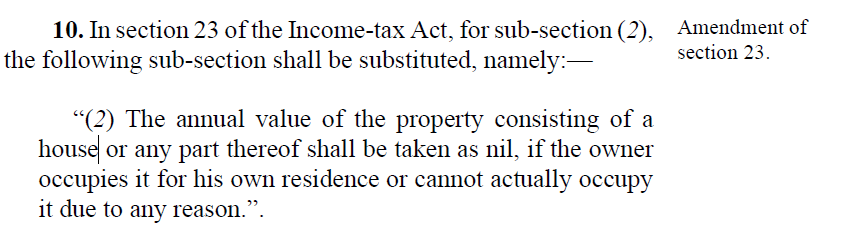

With a view to simplifying the provisions, it is proposed to amend the sub-section (2) so as to provide that the annual value of the property consisting of a house or any part thereof shall be taken as nil, if the owner occupies it for his own residence or cannot actually occupy it due to any reason.

Changes in Calculation of Income from House Property

Big Change in Calculation of House Property Income [Budget 2025]

Section 23 of the Act relates to determination of annual value. Sub-section (2) of the said section provides that where house property is in the occupation of the owner for the purposes of his residence or owner cannot actually occupy it due to his employment, business or profession carried on at any other place, in such cases, the annual value of such house property shall be taken to be nil. Further, sub-section (4) of the said section provides that provisions of sub-section (2) of the Act will be applicable in respect of two house properties only, which are to be specified by the owner.

With a view to simplifying the provisions, it is proposed to amend the sub-section (2) so as to provide that the annual value of the property consisting of a house or any part thereof shall be taken as nil, if the owner occupies it for his own residence or cannot actually occupy it due to any reason. The provision of sub-section (4) of section 23 of the Act which allows this benefit only in respect of two of such houses shall continue to apply as earlier.

This amendment will take effect from the 1st day of April, 2025 and shall accordingly apply for assessment year 2025-26 onwards.

This amendment will take effect from the 1st day of April, 2025 and shall accordingly apply for assessment year 2025-26 onwards.

This amendment will take effect from the 1st day of April, 2025 and shall accordingly apply for assessment year 2025-26 onwards.About Author

CA Pratibha Goyal

Co Founder

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

Studycafe

Studycafe New Delhi, Delhi, India

New Delhi, Delhi, India 1486

1486My Recent Articles

- Biggest Labour Reform in Indian History: 4 Labour Codes Effective from today

- Tax Audit and ITR Due date not extended in this case: Know More

- Government notifies Agreement and Protocol between India and Qatar [Read Notification]

- CA Breaking: Results of ICAI Examination to be announced soon, Know probable Date

- Breaking: GSTR-3B Due Date for September 2025 extended by CBIC amid Diwali Festivities

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.