CBIC levied ADD on Fluoro Backsheet Exported from China PR for a period of five years

CBIC levied ADD on Fluoro Backsheet Exported from China PR for a period of five years The Central Board of Indirect Taxes & Customs (CBIC) vide N…

CBIC levied ADD on Fluoro Backsheet Exported from China PR for a period of five years

The Central Board of Indirect Taxes & Customs(CBIC) vide Notification No. 22/2022-Customs (ADD) dated 15th June 2022 levied ADD on Fluoro Backsheet Exported from China PR for a period of five years.

The Notification is Given Below:

G.S.R.---(E). – Whereas, in the matter of “Fluoro Backsheet excluding transparent backsheet” (hereinafter referred to as the subject goods), falling under tariff headings 3920 and 3921 of the First Schedule to the Customs Tariff Act, 1975 (51 of 1975) (hereinafter referred to as the Customs Tariff Act), originating in, or exported from the China PR (hereinafter referred to as the subject country) and imported into India, the Designated Authority in its final findings, vide, notification F. No. 6/3/2021-DGTR, dated the 29th March, 2022, published in the Gazette of India, Extraordinary, Part I, Section 1, dated the 29th March, 2022, has come to the conclusion that-

The anti-dumping duty imposed by this notification will be due in Indian currency for a period of five years (unless cancelled, superseded, or amended earlier) from the date of publication of this notification in the Official Gazette.

Explanation - For the purposes of this notification, the rate of exchange applicable for the purpose of calculating such anti-dumping duty shall be the rate specified in the notification issued from time to time by the Government of India, through the Ministry of Finance (Department of Revenue), in exercise of the powers conferred by section 14 of the Customs Act, 1962 (52 of 1962), and the relevant date for determining the rate of exchange shall be the date of presentment.

For Official Notification Download PDF Given Below:

The anti-dumping duty imposed by this notification will be due in Indian currency for a period of five years (unless cancelled, superseded, or amended earlier) from the date of publication of this notification in the Official Gazette.

Explanation - For the purposes of this notification, the rate of exchange applicable for the purpose of calculating such anti-dumping duty shall be the rate specified in the notification issued from time to time by the Government of India, through the Ministry of Finance (Department of Revenue), in exercise of the powers conferred by section 14 of the Customs Act, 1962 (52 of 1962), and the relevant date for determining the rate of exchange shall be the date of presentment.

For Official Notification Download PDF Given Below:

(i) the product under consideration has been exported to India from the subject country at a price below normal value, thus resulting in dumping;

(ii) the domestic industry has suffered material injury due to dumping in respect of the subject goods; and

(iii) there is causal link between dumping of product under consideration and injury to the domestic industry,

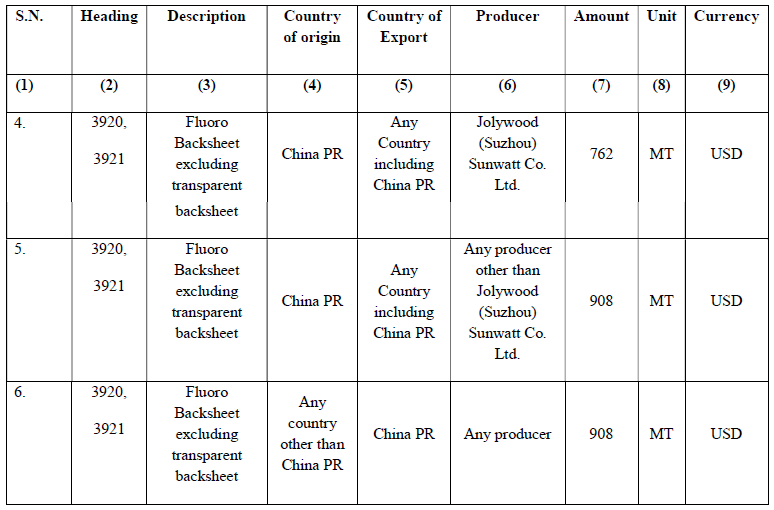

and has recommended imposition of anti-dumping duty on imports of the subject goods, originating in or exported from the subject country and imported into India, in order to remove injury to the domestic industry. Now, therefore, in exercise of the powers conferred by sub-sections (1) and (5) of section 9A of the Customs Tariff Act, read with rules 18 and 20 of the Customs Tariff (Identification, Assessment and Collection of Anti-dumping Duty on Dumped Articles and for Determination of Injury) Rules, 1995, the Central Government, after considering the aforesaid final findings of the designated authority, hereby imposes on the subject goods, the description of which is specified in column (3) of the Table below, falling under the tariff heading of the First Schedule to the Customs Tariff Act as specified in the corresponding entry in column (2), originating in the country as specified in the corresponding entry in column (4), exported from the countries as specified in the corresponding entry in column (5), produced by the producers as specified in the corresponding entry in column (6), and imported into India, an anti-dumping duty at the rate equal to the amount as specified in the corresponding entry in column (7), in the currency as specified in the corresponding entry in column (9) and as per unit of measurement as specified in the corresponding entry in column (8) of the said Table, namely :-

The anti-dumping duty imposed by this notification will be due in Indian currency for a period of five years (unless cancelled, superseded, or amended earlier) from the date of publication of this notification in the Official Gazette.

Explanation - For the purposes of this notification, the rate of exchange applicable for the purpose of calculating such anti-dumping duty shall be the rate specified in the notification issued from time to time by the Government of India, through the Ministry of Finance (Department of Revenue), in exercise of the powers conferred by section 14 of the Customs Act, 1962 (52 of 1962), and the relevant date for determining the rate of exchange shall be the date of presentment.

For Official Notification Download PDF Given Below:About Author

Reetu

Content Manager

Reetu is a Content Writer with 4+ years of experience in GST, Income Tax, Finance, Company Law, Education and Career Related Content. She is a B.COM (Honrs.) Graduate.

Reetu is a Content Writer with 4+ years of experience in GST, Income Tax, Finance, Company Law, Education and Career Related Content. She is a B.COM (Honrs.) Graduate.

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 8072

8072My Recent Articles

- Income Tax Guide for Indian Defence Personnel for Tax Filing, Taxable Allowances and Other Benefits

- Income Tax Return Breaking: ITR Forms released for AY 25-26

- Ex-DRT Officials Sentenced to 5 Years Rigorous Imprisonment by Madras High Court along with Rs.27 Lakh Fine

- GSTN issued Advisory on Case Sensitivity in IRN Generation

- RBI to issue Notes of Rs.10 and Rs.500 bearing Signature of Guv Malhotra

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts