CBIC Notifies New Rule 88D for dealing with ITC mismatch in GSTR-2B and GSTR-3B:

The CBIC has notified New Rule 88D regarding Manner of dealing with difference in ITC available in auto-generated statement containing the details of input tax credit and that availed in return via issuing Notification.

Manner of dealing with difference in ITC

CBIC Notifies New Rule 88D for dealing with ITC mismatch in GSTR-2B and GSTR-3B

The Central Board of Indirect Taxes and Custom(CBIC) has notified New Rule 88D regarding Manner of dealing with difference in ITC available in auto-generated statement containing the details of input tax credit and that availed in return via issuing Notification.

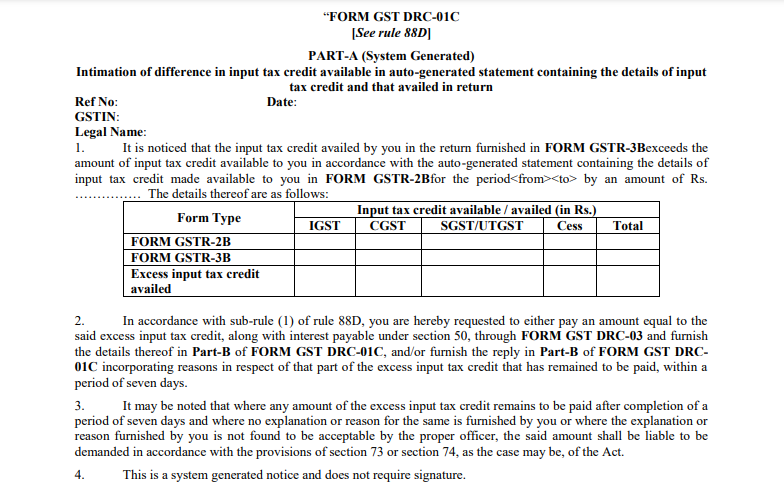

The system will now compare the ITC available in GSTR 3B to the ITC available in GSTR 2B. If the ITC obtained exceeds the prescribed amount and percentage, such disparities must be reported in Part A of FORM GST DRC-01C, and the Taxpayer must respond in Part B of FORM GST DRC-01C.

The Notification Stated as, "In exercise of the powers conferred by section 164 of the Central Goods and Services Tax Act, 2017 (12 of 2017), the Central Government, on the recommendations of the Council, hereby makes the following rules further to amend the Central Goods and Services Tax Rules, 2017."

In the said rules, after rule 88C, the following rule shall be inserted, namely:-

“88D. Manner of dealing with difference in input tax credit available in auto-generated statement containing the details of input tax credit and that availed in return.-

(1) Where the amount of input tax credit availed by a registered person in the return for a tax period or periods furnished by him in FORM GSTR-3B exceeds the input tax credit available to such person in accordance with the auto-generated statement containing the details of input tax credit in FORM GSTR-2B in respect of the said tax period or periods, as the case may be, by such amount and such percentage, as may be recommended by the Council, the said registered person shall be intimated of such difference in Part A of FORM GST DRC01C, electronically on the common portal, and a copy of such intimation shall also be sent to his e-mail address provided at the time of registration or as amended from time to time, highlighting the said difference and directing him to—

(a) pay an amount equal to the excess input tax credit availed in the said FORM GSTR-3B, along with interest payable under section 50, through FORM GST DRC-03, or

(b) explain the reasons for the aforesaid difference in input tax credit on the common portal, within a period of seven days.

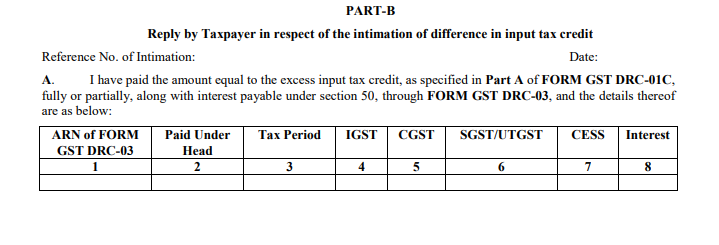

(2) The registered person referred to sub-rule (1) shall, upon receipt of the intimation referred to in the said sub-rule, either,

(a) pay an amount equal to the excess input tax credit, as specified in Part A of FORM GST DRC01C, fully or partially, along with interest payable under section 50, through FORM GST DRC-03 and furnish the details thereof in Part B of FORM GST DRC-01C, electronically on the common portal, or

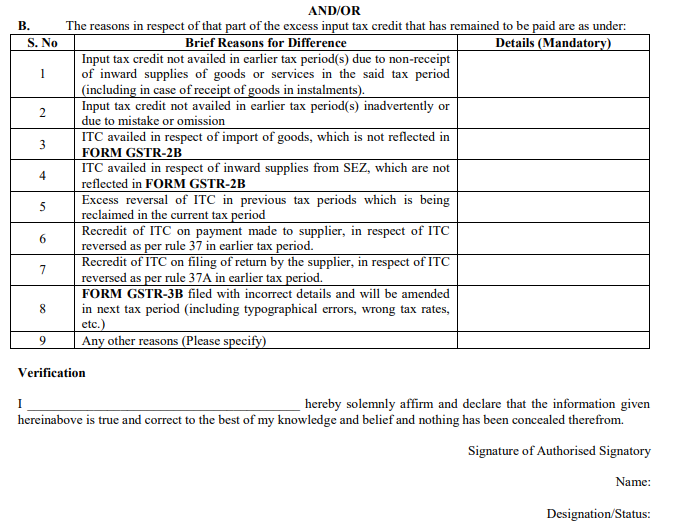

(b) furnish a reply, electronically on the common portal, incorporating reasons in respect of the amount of excess input tax credit that has still remained to be paid, if any, in Part B of FORM GST DRC-01C,

within the period specified in the said sub-rule.

(3) Where any amount specified in the intimation referred to in sub-rule (1) remains to be paid within the period specified in the said sub-rule and where no explanation or reason is furnished by the registered person in default or where the explanation or reason furnished by such person is not found to be acceptable by the proper officer, the said amount shall be liable to be demanded in accordance with the provisions of section 73 or section 74, as the case may be.”.

For Official Notification Download PDF Given Below:

For Official Notification Download PDF Given Below:

For Official Notification Download PDF Given Below:About Author

Reetu

Content Manager

Reetu is a Content Writer with 4+ years of experience in GST, Income Tax, Finance, Company Law, Education and Career Related Content. She is a B.COM (Honrs.) Graduate.

Reetu is a Content Writer with 4+ years of experience in GST, Income Tax, Finance, Company Law, Education and Career Related Content. She is a B.COM (Honrs.) Graduate.

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 8072

8072My Recent Articles

- Income Tax Guide for Indian Defence Personnel for Tax Filing, Taxable Allowances and Other Benefits

- Income Tax Return Breaking: ITR Forms released for AY 25-26

- Ex-DRT Officials Sentenced to 5 Years Rigorous Imprisonment by Madras High Court along with Rs.27 Lakh Fine

- GSTN issued Advisory on Case Sensitivity in IRN Generation

- RBI to issue Notes of Rs.10 and Rs.500 bearing Signature of Guv Malhotra

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts