Changes by GST Notification No 30/2020 to 36/2020 dated 03.04.2020

Recent Changes in GST vide Various Notification No. 30/2020 to 36/2020 dated 03.04.2020 In view of the spread of pandemic COVID-19, the Hon’

Recent Changes in GST vide Various Notification No. 30/2020 to 36/2020 dated 03.04.2020

In view of the spread of pandemic COVID-19, the Hon’ble FM has announced various reliefs measures relating to statutory and regulatory compliance matters in GST. For ease of your convenience and reference, due date calendar for various returns in GST is given as under:

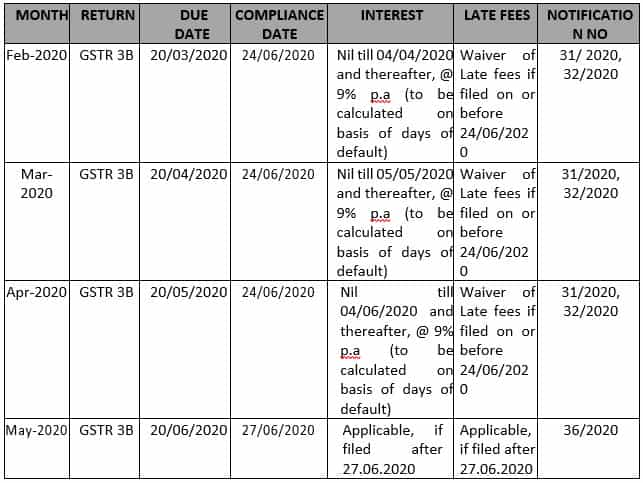

Taxpayers having Aggregate Turnover of More Than Rs. 5 Cr in the Preceding Financial Year

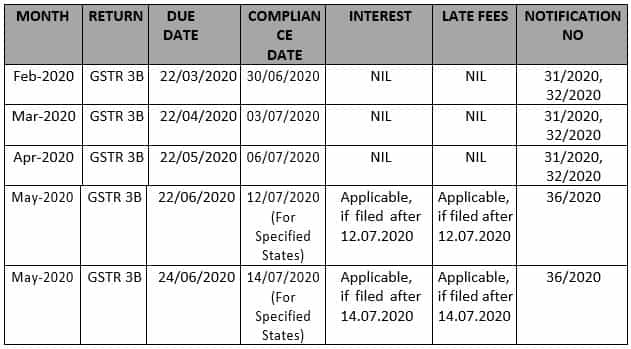

Taxpayers having Aggregate Turnover of More Than Rs. 1.5 Cr but up to Rs. 5 Cr in the Preceding Financial Year

Taxpayers having Aggregate Turnover of More Than Rs. 1.5 Cr but up to Rs. 5 Cr in the Preceding Financial Year

Taxpayers having Aggregate Turnover of up to Rs. 1.5 Cr in the Preceding Financial Year

Taxpayers having Aggregate Turnover of up to Rs. 1.5 Cr in the Preceding Financial Year

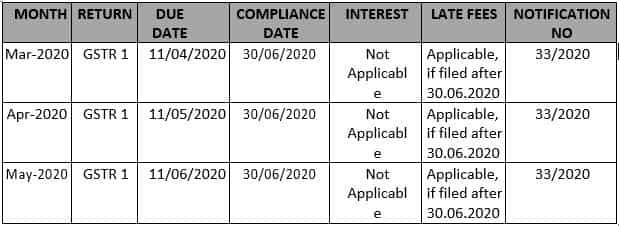

Due Date for filing Form GSTR-1 for the Taxpayers having Aggregate Turnover of More Than Rs. 1.5 Cr

Due Date for filing Form GSTR-1 for the Taxpayers having Aggregate Turnover of More Than Rs. 1.5 Cr

Due Date for filing Form GSTR-1 for the Taxpayers having Aggregate Turnover up to Rs. 1.5 Cr

Due Date for filing Form GSTR-1 for the Taxpayers having Aggregate Turnover up to Rs. 1.5 Cr

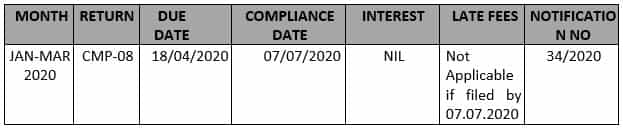

Due Date for filing Form CMP-08 i.e. Statement for payment of self-assessed tax by the Composition Dealer

Due Date for filing Form CMP-08 i.e. Statement for payment of self-assessed tax by the Composition Dealer

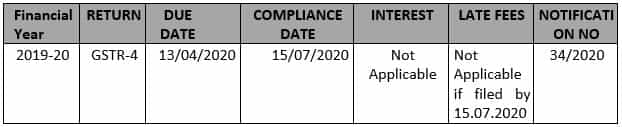

Due Date for filing Form GSTR- 04 for Composition Dealer for FY 2019-20

Due Date for filing Form GSTR- 04 for Composition Dealer for FY 2019-20

Miscellaneous Provisions: -

Miscellaneous Provisions: -

DISCLAIMER: The views expressed are strictly of the author and A2Z Taxcorp LLP. The contents of this article are solely for informational purpose. It does not constitute professional advice or recommendation of firm. Neither the author nor firm and its affiliates accepts any liabilities for any loss or damage of any kind arising out of any information in this article nor for any actions taken in reliance thereon.

Taxpayers having Aggregate Turnover of More Than Rs. 1.5 Cr but up to Rs. 5 Cr in the Preceding Financial Year

Taxpayers having Aggregate Turnover of up to Rs. 1.5 Cr in the Preceding Financial Year

Due Date for filing Form GSTR-1 for the Taxpayers having Aggregate Turnover of More Than Rs. 1.5 Cr

Due Date for filing Form GSTR-1 for the Taxpayers having Aggregate Turnover up to Rs. 1.5 Cr

Due Date for filing Form CMP-08 i.e. Statement for payment of self-assessed tax by the Composition Dealer

Due Date for filing Form GSTR- 04 for Composition Dealer for FY 2019-20

Miscellaneous Provisions: -

- Relaxation of Provision Under Rule 36(4): In Terms of Notification No. 30/2020, a proviso has been inserted in CGST Rules 2017 to provide that the condition as stated in Rule 36(4) of the CGST Rules, 2017 shall not apply to input tax credit availed by the registered person in the returns in FORM GSTR-3B for the months of February 2020, March 2020, April 2020, May 2020, June 2020, July 2020 and August, 2020, but that the said condition shall apply cumulatively for the said period in the return in FORM GSTR-3B for the tax period of September, 2020 shall be furnished with cumulative adjustment of ITC.

Condition under rule 36(4) prescribes the restriction for availment of Input Tax Credit (“ITC”) i.e. 10% of the eligible credit in respect of invoices or debit notes the details of which have not been uploaded by the suppliers under sub-section (1) of section 37 of the CGST Act, 2017.

- Validity of E-Way Bill: In terms of Notification No. 35/2020 (effective w.e.f. March 20, 2020) where an E-Way Bill has been generated under rule 138 of the CGST, 2017 and its period of validity expires during the period 20.03.2020 to 15.04.2020, the validity period of such e-way bill shall be deemed to have been extended till the 30.04.2020.

- Extension of Due Dates for compliances under the GST Laws falling in the period from March 20, 2020 to June 29, 2020 for Form GSTR-5, GSTR-6, GSTR-7, GSTR-8: In terms of Notification No. 35/2020 (effective w.e.f. March 20, 2020) it is stated that the said class of taxpayers have been allowed to furnish the respective returns specified in sub-sections (3) i.e. Tax Deducted at Source (Form GSTR-7), (4) i.e. Input Service Distributor (Form GSTR-6) and (5) i.e. Non-Resident Taxable Person (GSTR - 5), of section 39 of the CGST Act, for the months of March, 2020 to May, 2020 to be filed on or before the June 30, 2020.

- As per Notification No. 35/2020, all other compliances viz. Appeal, Refund, statement, etc. under the provisions of the CGST Act which is falling during the period from March 20, 2020 to June 29, 2020 is extended to June 30, 2020 EXCEPT for following provisions of the CGST Act, as mentioned below –

| Date | Source | Reference No. | Subject |

| April 03, 2020 | CBIC | Notification No. 30/2020 – Central Tax | Seeks to amend CGST Rules (Fourth Amendment) in order to allow opting Composition Scheme for FY 2020-21 till 30.06.2020 and to allow cumulative application of condition in rule 36(4). |

| April 03, 2020 | CBIC | Notification No. 31/2020 – Central Tax | Seeks to provide relief by conditional lowering of interest rate for tax periods of February, 2020 to April, 2020. |

| April 03, 2020 | CBIC | Notification No. 32/2020 – Central Tax | Seeks to provide relief by conditional waiver of late fee for delay in furnishing returns in FORM GSTR-3B for tax periods of February, 2020 to April, 2020. |

| April 03, 2020 | CBIC | Notification No. 33/2020 – Central Tax | Seeks to provide relief by conditional waiver of late fee for delay in furnishing outward statement in FORM GSTR-1 for tax periods of February, 2020 to April, 2020. |

| April 03, 2020 | CBIC | Notification No. 34/2020 – Central Tax | Seeks to extend due date of furnishing FORM GST CMP-08 for the quarter ending March, 2020 till 07.07.2020 and filing FORM GSTR-4 for FY 2020-21 till 15.07.2020. |

| April 03, 2020 | CBIC | Notification No. 35/2020 – Central Tax | Seeks to extend due date of compliance which falls during the period from "20.03.2020 to 29.06.2020" till 30.06.2020 and to extend validity of e-way bills. |

About Author

A2ZBimal Jain

Chartered Accountant

CA Bimal Jain is a Member of Institute of Chartered Accountants of India since May 1994 and Member of Institute of Company Secretaries of India since December 2006 along with a Bachelors degree in Law. Also, he is a Qualified SAP - FI/CO Consultant and has more than 21 years of experience in Indirect Taxation and specializes in all aspects of Service Tax, Value Added Tax (VAT)/ Central Sales Tax (CST), Central Excise, Customs, Foreign Trade Policy (FTP), Special Economic Zone (SEZ), Export Oriented Unit (EOU), Export-Import Laws and well acquainted with the concept and impact of way forward Goods and Services tax (GST).

CA Bimal Jain is a Member of Institute of Chartered Accountants of India since May 1994 and Member of Institute of Company Secretaries of India since December 2006 along with a Bachelors degree in Law. Also, he is a Qualified SAP - FI/CO Consultant and has more than 21 years of experience in Indirect Taxation and specializes in all aspects of Service Tax, Value Added Tax (VAT)/ Central Sales Tax (CST), Central Excise, Customs, Foreign Trade Policy (FTP), Special Economic Zone (SEZ), Export Oriented Unit (EOU), Export-Import Laws and well acquainted with the concept and impact of way forward Goods and Services tax (GST).

A2Z Taxcorp LLP

A2Z Taxcorp LLP Delhi, Delhi, India

Delhi, Delhi, India 468

468My Recent Articles

- Actions taken by the department during enquiry need not necessarily be termed as harassment

- Who are liable to generate e-invoice w.e.f October 1, 2022

- Personal penalty cannot be imposed on the Chairman of the Company for failure in ensuring proper accounting of the goods

- Stayed the order of cancellation of GST Registration of the assessee for continuing the trading activities

- Can CA be arrested- Section 69 vs Section 132 of the CGST Act

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

Recent Posts

All Posts