Changes in GST Rate on Rent a Cab Services w.e.f. 20-10-2023:

Changes in GST Rate on Rent-a-Cab Services w.e.f. 20-10-2023 The following amendment has been made in Notification No. 11/2017-Central Tax (Rate) dat…

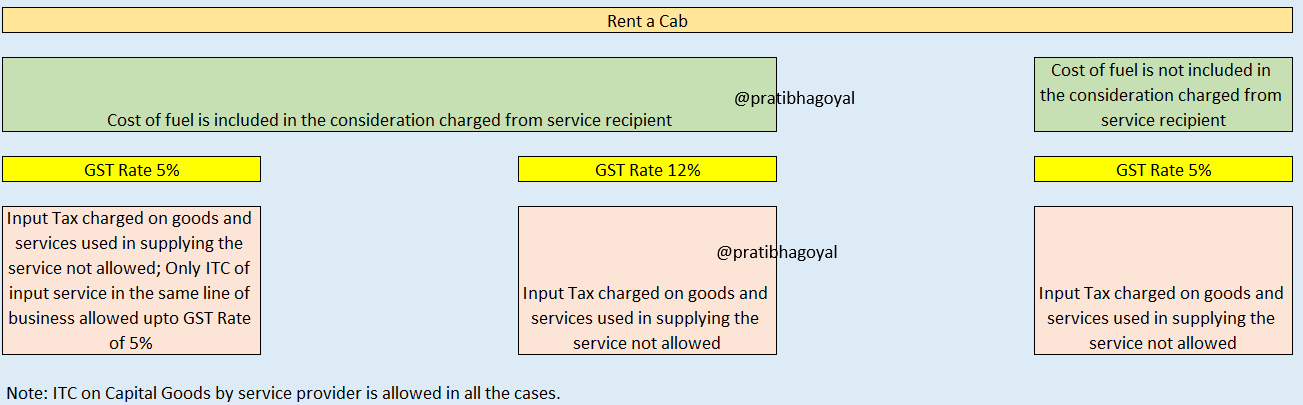

GST Rate on Rent a Cab Services

Changes in GST Rate on Rent-a-Cab Services w.e.f. 20-10-2023

The following amendment has been made in Notification No. 11/2017-Central Tax (Rate) dated 28.06.2017 by Notification No. 12/2023-Central Tax (Rate) dated 20-10-2023.

Supply of service by way of transportation of passengers by motor cab or renting of motor cab, where the cost of fuel is included attracts GST @ 5% or 12% without or with ITC respectively. wherever the GST is paid at the rate of 5%, the condition for availing ITC in same line of business is restricted to 5% even if input tax at the rate of 12%.

This has been Explained by following examples:

This has been Explained by following examples:

Example 1

Example 2

Example 3

Example 4

Note: ITC on Capital Goods is allowed to service provider (Mr. A or Mr. B) in all the cases.

This has been Explained by following examples:

| A | Main Service Provider | |

| B | Input service Provider to A in the same line of business | |

| C; Unregistered | Customer of A | |

| Particulars | Services provided by A to C | Services provided by B to C |

| Taxable Value | 1000 | 800 |

| GST Rate | 5% | 5% |

| GST on Output | 50 | 40 |

| ITC | ITC Allowed to A w.r.t. services provided by B= Rs. 40. ITC of Goods and service other than ITC of input service in the same line of business will not be allowed. | |

| Particulars | Services provided by A to C | Services provided by B to C |

| Taxable Value | 1000 | 800 |

| GST Rate | 5% | 12% |

| GST on Output | 50 | 96 |

| ITC | ITC Allowed to A w.r.t. services provided by B= Rs. 40. ITC of Goods and service other than ITC of input service in the same line of business will not be allowed. | |

| Particulars | Services provided by A to C | Services provided by B to C |

| Taxable Value | 1000 | 800 |

| GST Rate | 12% | 5% |

| GST on Output | 120 | 40 |

| ITC Allowed to A w.r.t. services provided by B= Rs. 40. ITC of Goods and service other than ITC of input service in the same line of business will be allowed in this case. | ||

| Particulars | Services provided by A to C | Services provided by B to C |

| Taxable Value | 1000 | 800 |

| GST Rate | 12% | 12% |

| GST on Output | 120 | 96 |

| ITC Allowed to A w.r.t. services provided by B= Rs. 96. ITC of Goods and service other than ITC of input service in the same line of business will be allowed in this case. | ||

About Author

CA Pratibha Goyal

Co Founder

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

Studycafe

Studycafe New Delhi, Delhi, India

New Delhi, Delhi, India 1486

1486My Recent Articles

- Biggest Labour Reform in Indian History: 4 Labour Codes Effective from today

- Tax Audit and ITR Due date not extended in this case: Know More

- Government notifies Agreement and Protocol between India and Qatar [Read Notification]

- CA Breaking: Results of ICAI Examination to be announced soon, Know probable Date

- Breaking: GSTR-3B Due Date for September 2025 extended by CBIC amid Diwali Festivities

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

Recent Posts

All Posts