Changes in new ITR Forms for AY 2021-22

Changes in new ITR Forms for AY 2021-22 CBDT has released new ITR Forms vide Notification Number 21/2021 dated April 1, 2021 . This article discusses…

Table of Contents

Changes in new ITR Forms for AY 2021-22

CBDT has released new ITR Forms vide Notification Number 21/2021 dated April 1, 2021.

This article discusses changes in new ITR [Income Tax Return] Forms released by the Central Board of Direct Taxes [CBDT] for AY 2021-22 or FY 2020-21.

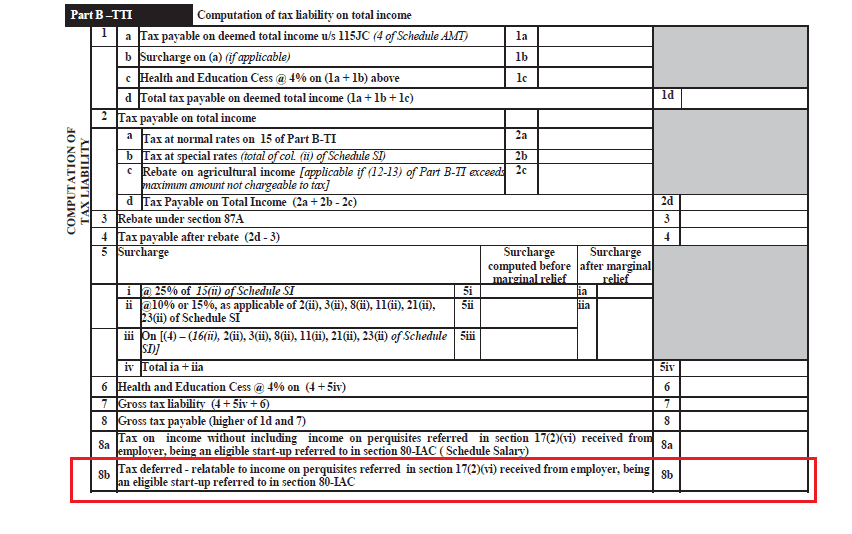

Amount Deferred in respect of ESOPs

If an Employee of Eligible Startup u/s has received ESOPs and Taxliability on same has been deferred, then ITR-1 cannot be filed. The same shall be shown in ITR-2 or ITR-3.

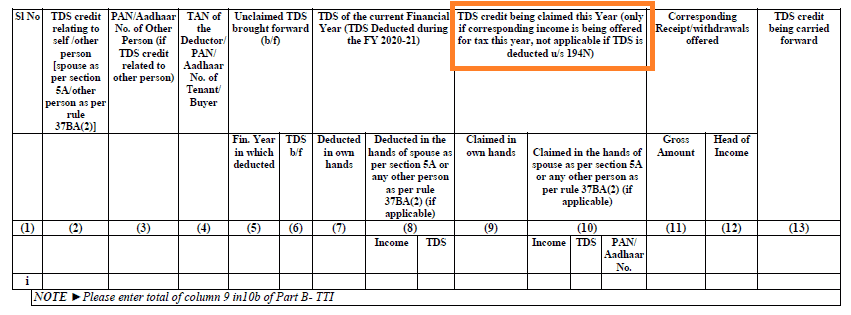

TDS under section 194N

Tax under section 194N is required to be deducted if the amount of cash withdrawn during the year exceeds Rs. 20 lakhs in the case of certain non-filers of ITR and Rs 1 crore in other cases. Any Tax Payer, whose TDS has been deducted under section 194N cannot File ITR-1.No Option provided to carry Forward TDS under section 194N

TDS under section 194N is not related to the income of the taxpayer. It is related to cash withdrawal during the year. Thus no, option to carry forward TDS has been provided in the Forms. Change has been made in ITR-2 to ITR-7 Accordingly.

Taxability of Dividend Income

- The dividend was made taxable by Finance Act 2020. Accordingly, the ITR Forms for FY 2020-21 have been amended to account for the same.

- Also, Taxpayers are required to provide a Quarterly breakup of Dividend income for Calculation of Interest u/s 234C

- Schedule DDT has been removed from ITR-6 [Applicable on companies].

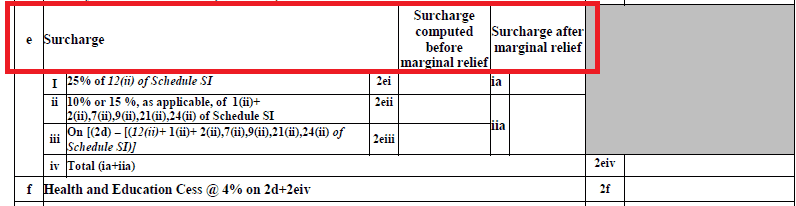

Marginal Relief Effect to be highlighted in the ITR Form

ITR Forms have been amended to provide for Surcharge computed before marginal relief and Surcharge after marginal relief.

Tax Audit Limit Changes

As we know the Tax Audit Limit has been increased to Rs. 10Cr from Rs. 5Cr by Finance Act 2021 where: (a) the aggregate sales, in cash, does not exceed 5% of total sales; and (b) the aggregate payments, in cash, does not exceed 5% of total payment. Accordingly, the ITR Forms for AY 2021-22 have been amended to account for the same.Adjustment of unabsorbed depreciation and losses on account of various exemptions and deductions for Taxpayer opting for Section 115BAC or 115BAD

Unabsorbed depreciation

A taxpayer opting to take benefit of Section 115BAC or Section 115BAD:- Cannot carry forward unabsorbed depreciation relating to additional depreciation.

- Cannot take a further deduction on account of additional depreciation.

Losses on account of various exemptions and deductions

A taxpayer opting to take benefit of Section 115BAC or Section 115BAD:- Cannot carry forward Losses on account of various exemptions and deductions as specified in Section 115BAC or Section 115BAD.

- Cannot take a further deduction on account of same.

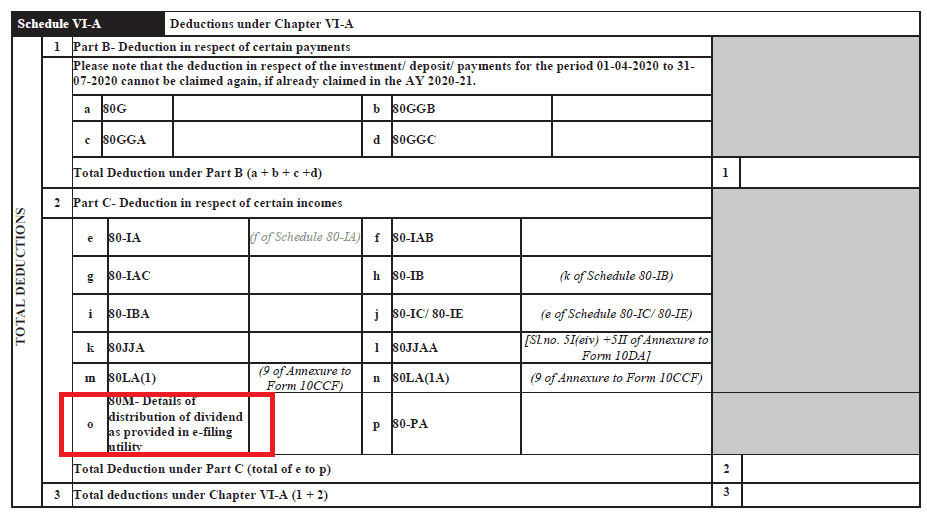

Section 80M Deduction

As per Section 80M introduced by Finance Act 2020:- The deduction can be claimed by a domestic company for the amount received as a dividend from another domestic company, a foreign company, or a business trust.

- The deduction is allowed when the company further distributes the dividend to the shareholders.

- Accordingly, the ITR-6 Form has been amended to account for the same.

Schedule DI Deleted

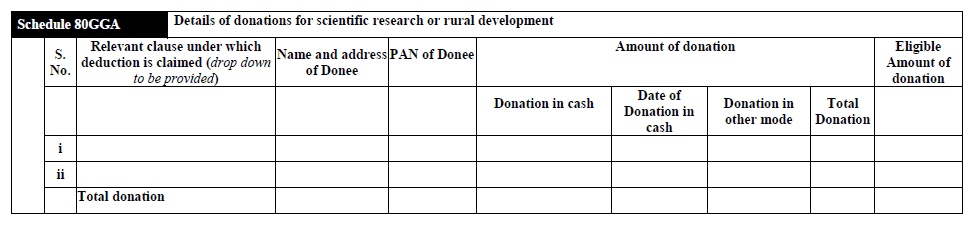

During FY 2019-20, the due date for claiming deduction under Chapter VI-A, section 10AA, and section 54 to 54GB was extended till 30-06-2020. This was benefit given at the time of lockdown. Now this schedule DI for reporting such investments has been Deleted.Date to be mentioned in respect of Cash Donations u/s 80GGA

The ITR forms notified for Assessment year 2021-2022 require additional disclosures of the date on which such cash donation has been made.

No separate reporting of LIC Bussiness Income

The ITR forms notified for Assessment Year 2021-2022 have removed such separate reporting requirements in respect of income from the life insurance business in Schedule BP.A specific ceiling that deduction u/s 54EC cannot exceed Rs. 50 Lakh has been provided in the ITR Forms.

Section 80P deduction: Nature of business code to be mentioned by the taxpayer

Now Nature of the business code is to be mentioned if the assessee is claiming deduction under section 80P.About Author

CA Pratibha Goyal

Co Founder

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

Studycafe

Studycafe New Delhi, Delhi, India

New Delhi, Delhi, India 1486

1486My Recent Articles

- Biggest Labour Reform in Indian History: 4 Labour Codes Effective from today

- Tax Audit and ITR Due date not extended in this case: Know More

- Government notifies Agreement and Protocol between India and Qatar [Read Notification]

- CA Breaking: Results of ICAI Examination to be announced soon, Know probable Date

- Breaking: GSTR-3B Due Date for September 2025 extended by CBIC amid Diwali Festivities

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts