Changes introduced in ITR forms for AY 2025–26:

CBDT has released ITR-1 and ITR-4 forms for AY 2025–26. Let us understand some important changes introduced in ITR forms for AY 2025–26

ITR Changes FY 24-25

The Central Board of Direct Taxes (CBDT) has released Income Tax Return Forms (ITR Forms) for the Financial Year 2024-25 (Assessment Year 2025-26).

ITR-1 (SAHAJ): This form can be filed by individuals being a resident (other than not ordinarily resident) having total income upto Rs. 50 lakh and having Income from Salaries, one house property, other sources (Interest etc.), long-term capital gains under section 112A up to Rs. 1.25 lakh, and agricultural income up to Rs. 5 thousand.

ITR-4 (SUGAM): This form can be filed by Individuals, HUFs and Firms (other than LLP) being a resident having total income upto Rs.50 lakh and having income from business and profession which is computed under sections 44AD, 44ADA or 44AE, and having long-term capital gains under section 112A upto Rs. 1.25 lakh.

Changes Introduced:

ITR-1 and ITR-4 can now be used even if there is long-term capital gain (LTCG) under section 112A, provided:

Until AY 2024-25, ITR-1 or ITR-4 couldn’t be used at all if any capital gains existed.

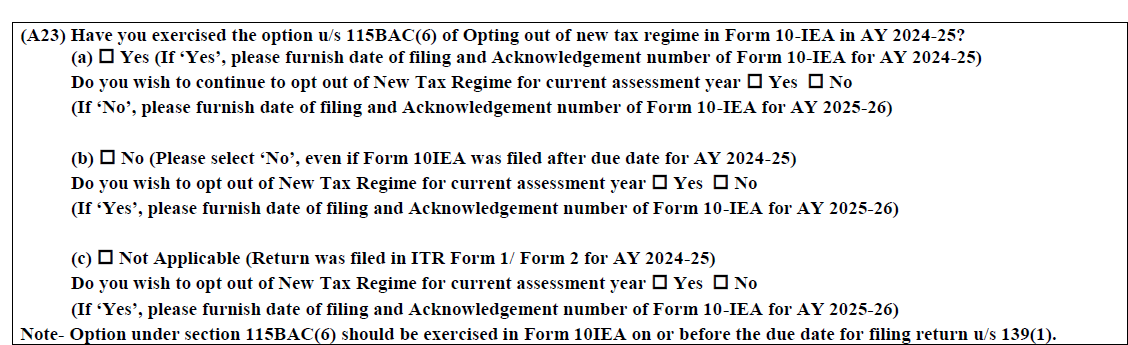

ITR-4 Form has expanded disclosure on opting out of new tax regime using Form 10-IEA under section 115BAC(6):

Until AY 2024-25, ITR-1 or ITR-4 couldn’t be used at all if any capital gains existed.

ITR-4 Form has expanded disclosure on opting out of new tax regime using Form 10-IEA under section 115BAC(6):

In both ITR-1 and ITR-4 Forms

In both ITR-1 and ITR-4 Forms

- The LTCG does not exceed Rs. 1.25 lakh, and

- There is no loss to be carried forward or set off under the capital gains head.

Until AY 2024-25, ITR-1 or ITR-4 couldn’t be used at all if any capital gains existed.

ITR-4 Form has expanded disclosure on opting out of new tax regime using Form 10-IEA under section 115BAC(6):

- If opting out in AY 2024–25, the user must declare and optionally continue or reverse that decision.

- If opting out for the first time in AY 2025–26, they must provide Form 10-IEA acknowledgment details.

- Now, there is an option for additional clarification regarding the late filing of Form 10-IEA.

In both ITR-1 and ITR-4 Forms

- All deductions (e.g., 80C to 80U) must now be selected from a drop-down in the e-filing utility. Specific clauses and subsections must be disclosed.

- Income under section 89A (retirement accounts maintained abroad) has enhanced fields and relief tracking

- All bank accounts held in India during the previous year must be reported (excluding dormant accounts).

- At least one account must be selected for refund credit.

About Author

CA Pratibha Goyal

Co Founder

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

Studycafe

Studycafe New Delhi, Delhi, India

New Delhi, Delhi, India 1486

1486My Recent Articles

- Biggest Labour Reform in Indian History: 4 Labour Codes Effective from today

- Tax Audit and ITR Due date not extended in this case: Know More

- Government notifies Agreement and Protocol between India and Qatar [Read Notification]

- CA Breaking: Results of ICAI Examination to be announced soon, Know probable Date

- Breaking: GSTR-3B Due Date for September 2025 extended by CBIC amid Diwali Festivities

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.