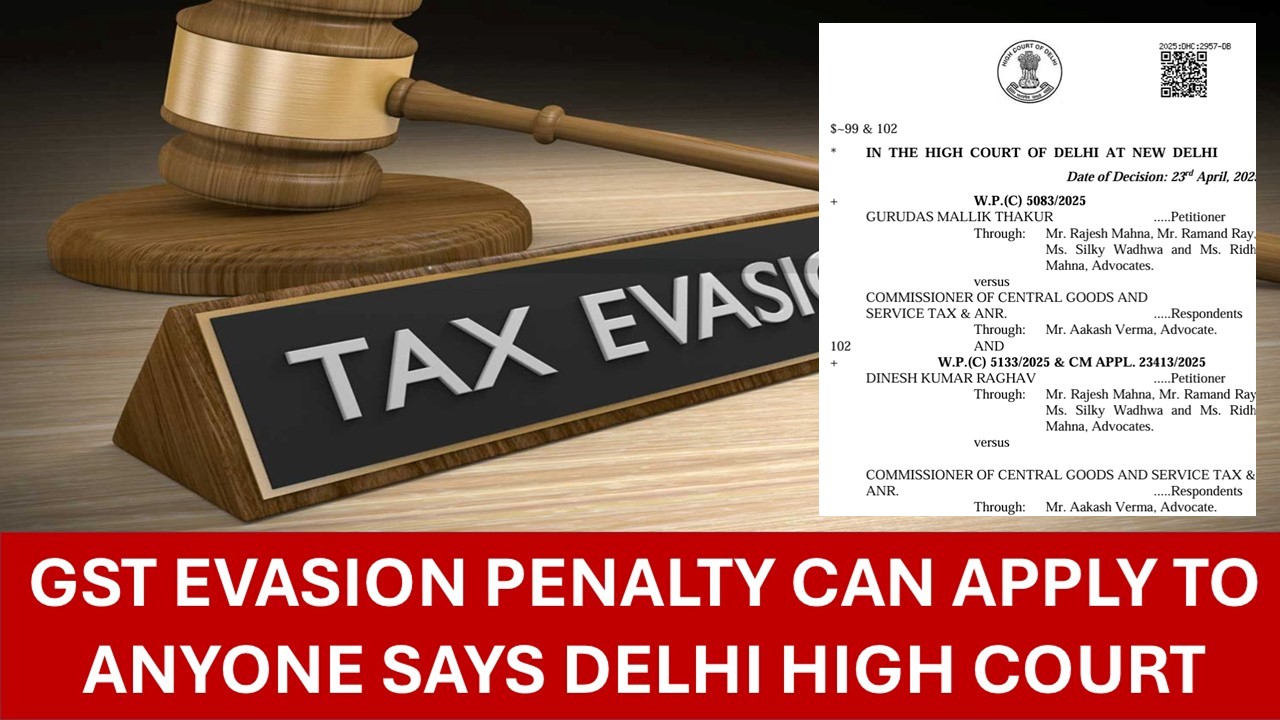

Delhi High Court: GST Evasion Penalty Can Apply to Anyone, Not Just Taxpayers:

The Delhi High Court has made it clear that a penalty for GST avoidance under Section 122(1A) of the Central Goods and Services Tax Act 2017 can be levied against 'any person,' whether a taxable person or not.

GST Evasion Penalty can Apply to Anyone says Delhi High Court

Delhi High Court: GST Evasion Penalty Can Apply to Anyone, Not Just Taxpayers

The Delhi High Court has made it clear that a penalty for GST avoidance under Section 122(1A) of the Central Goods and Services Tax Act 2017 can be levied against 'any person,' whether a taxable person or not.

Justices Prathiba M. Singh and Rajneesh Kumar Gupta pointed out that Section 122(1A) specifically uses the term 'any person,' which is different from the term 'taxable person' used elsewhere in the Act. The court referenced a Bombay High Court ruling in the case of Bharat Parihar V. State of Maharashtra, which established that 'any person' includes non-taxable persons as well.

The facts were such that directors of M/s Planman HR Private Limited, a recruitment agency, were involved in the case. The investigation discovered that the company had claimed CENVAT credit in an improper manner, aggregating to Rs.22,41,07,389/-.

One of the petitioners, Gurudas Mallik Thakur, was arrested on August 21, 2020, for making false entries in Service Tax Returns under the Finance Act, 1994. Following this, a Show Cause Notice was issued, and the company's Goods and Service Tax Returns were thoroughly examined.

The GST Department discovered that the company had not filed complete returns. GSTR-1M returns were only filed until February 2019, while GSTR-3B was filed only until December 2018.

When asked to file the missing returns, both directors claimed that one Mr. Arindam Chaudhary, who owned 90% of the company shares, was the primary decision-maker.

After taking statements from both petitioners and reviewing company documents, including balance sheets, the Department determined there was a shortfall of Rs. 40,61,37,843 in GST payments. This value was to be recovered under Section 74 of the CGST Act. The company was also charged with taking inadmissible Input Tax Credit and not submitting copies of tax invoices and debit notes.

The investigation covered the two petitioners, Mr. Arindam Chaudhary and Mr. Varun Khanna. According to the findings, none of the directors accepted responsibility for filing the company's GST returns. The petitioners claimed they resigned in 2020 and that Mr. Chaudhary ran the company, with Mr. Khanna serving as CEO.

After perusing all submissions, the adjudicating authority held both the company and its directors (the petitioners) responsible for the demands and levied penalties upon them.

The petitioners contended that they were not taxable persons under Sections 122 or 122(1A) of the CGST Act and hence could not be prosecuted.

The court recognized that the petitioners were, in fact, company directors but observed that their precise roles, the degree of control, and any advantages they enjoyed would have to be established from records filed before the Appellate Authority. The court upheld that the order could be appealed under Section 107 of the CGST Act.

The court observed that penalties were imposed on various directors who had active roles according to the challenged order. It determined that the correct course of action for the petitioners would be to approach the Appellate Authority.

The petitioners pointed out a procedural issue: non-taxable persons cannot file appeals through the portal. Since they claimed to be non-taxable persons who had been penalized, the Department would need to create a mechanism for them to file appeals.

The court directed the Department to inform the petitioners within two weeks about how they could file their appeals. Once notified, the petitioners would have 30 days to file their appeals.

About Author

Janvi Koli

Digital Marketing Executive

Janvi is an expert content writer focused on taxation and compliance. She writes insightful articles on income tax, GST, company law, and government policies. Known for her practical approach, she simplifies complex regulations to help readers stay informed and compliant. She can be reached at [email protected]

Janvi is an expert content writer focused on taxation and compliance. She writes insightful articles on income tax, GST, company law, and government policies. Known for her practical approach, she simplifies complex regulations to help readers stay informed and compliant. She can be reached at [email protected]

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 325

325My Recent Articles

- Ethereum Fundamentals for Finance Students through Understanding Blockchain Beyond Bitcoin

- Major Financial Changes Effective from November 1, Every Indian Should Aware Of

- Top 20 CA Firms in Mumbai for Articleship

- Know How to Setup EV Charging Stations: Step by Step Guide

- Unlock business growth this Independence Day with Bajaj Finserv Business Loan

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.