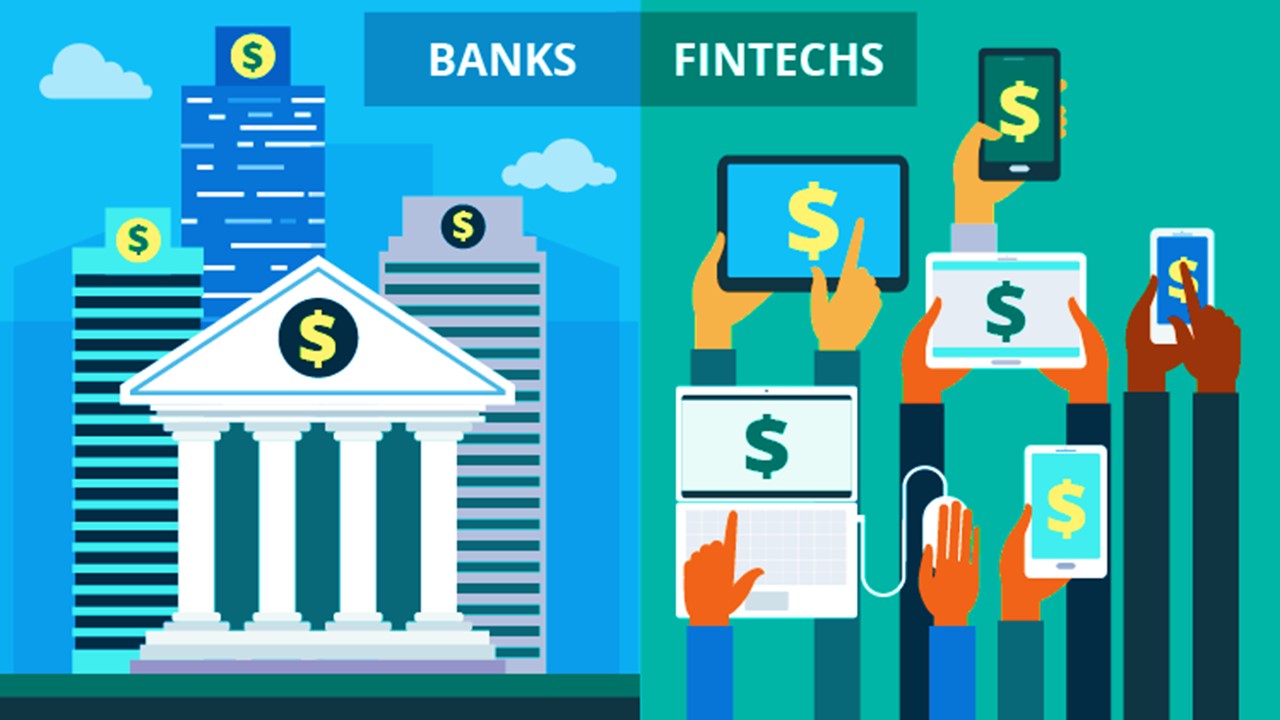

Difference Between Banks and Fintech Startups

Difference Between Banks and Fintech Startups Banking , which began in Italy during the Renaissance in the 14th century, conjures up images of tradit…

Table of Contents

Difference Between Banks and Fintech Startups

Banking, which began in Italy during the Renaissance in the 14th century, conjures up images of tradition and dependability. Startups, on the other hand, which sprung up all over the world at the turn of the millennium, are linked with vitality and unconventional thinking.

Fintech businesses, which have revolutionised the area of finance by introducing technological marvels, are regarded to have the ability to give banks a run for their money.

To get a better picture of the future of finance, let's go over the benefits and downsides of both traditional banking and fintech businesses.

Strengths of Banks

When it comes to billion-dollar infrastructure and priceless trustworthiness, banks unquestionably have the upper hand. Retail banking, business banking, corporate banking, private banking, and investment banking are the major categories of banking activity. Individuals and small businesses are dealt with directly in retail banking, whilst mid-level and large enterprises are dealt with in business banking and corporate banking, respectively. Private banking focuses on offering wealth management services to individuals and families with a high net worth. Investment banking primarily focuses on generating funds for businesses, as well as aiding mergers and acquisitions and market-making (for derivative securities).Strengths of Fintechs

Fintech businesses aren't bound by traditional working practices or red tape. They have the creative vision, unwavering determination, technology support, and audacity to see it through. These firms have attracted the attention of several venture investors, who have invested billions of dollars in them annually since 2010. Around 128 billion dollars was spent in Fintech in 2018, with a forecast of 310 billion dollars by 2022.How are Fintechs Challenging Banks?

Fintech firms are attempting to take on banks by developing cutting-edge digital services and products that pose a threat to traditional banking. Some fintech start-ups represent a direct threat by using established organisations' shortcomings and inadequacies. Peer-to-peer payments, which are part of retail banking, are one of the areas that could be significantly impacted. A slew of firms provides low-cost fast money transfers from the convenience of your smartphone screen. Some even provide international money transfer services. This is something that retail banks should be concerned about. Startups are primarily concerned with obtaining and analysing data and providing personalised services. As a result, business and corporate banking are mostly unaffected by the fintech threat. Fintech businesses, on the other hand, employ advanced research and prediction technologies, making them perfect for those looking to engage in capital and derivative markets. Luxury goods brokerage and crowdfunded loans are two more fields where several fintech startups are thriving. An innovative European firm analyses the investing patterns and payoffs of its customers and offers helpful feedback and guidance. This makes them appealing to small investors who appreciate the assistance but are wary of receiving it from banks for a high cost. Fintech businesses are also venturing into the sphere of quick currency conversion for travellers.Where does Fintechs face Challenges?

Institutional banks operate on a massive scale that fintech firms will be unable to match, at least for the time being. Without banks, fintech firms would not exist. Because the vast majority of people keep their money in banks, practically all fintech services now available rely on financial information about users that only banks have access to. If banks chose to use their competitive advantage (access to customers' financial information) against fintech startups, it might spell disaster for the latter, which lack the resources and brand awareness to compete effectively without it. Both banks and fintech firms have their strengths, but banks have a more established network and customer base that startups cannot readily entice away. Banks, on the other hand, must strengthen their position by examining and upgrading their technology. If financial services that are directly challenged by fintech firms are to stay competitive, they may need to reduce fees and become more consumer-friendly.Final Thoughts

The original harsh competitive competition between banks and startups is being progressively replaced by concepts of collaboration and mentorship. ICICI Bank and Kotak Mahindra bank, for example, have taken on a few fintech firms and are collaborating with them. A majority of European and American banks are in the same boat. Banks are eager to collaborate with startups because it gives them a fresh viewpoint, new business models, process efficiencies, and income prospects. In this manner, entrepreneurs can acquire the funding they need while maintaining their identity and autonomy. Cooperation, rather than rivalry, is the way forward, and the entire financial industry is benefiting from it!About Author

Deepshikha Mahapatra

Editor

Studycafe

Studycafe Bhubaneswar, Orissa, India

Bhubaneswar, Orissa, India 226

226Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts