Do we need to file Nil statement of financial transaction [SFT] or Not

![Do we need to file Nil statement of financial transaction [SFT] or Not](https://assets.studycafe.in/uploads/2020/05/Filing-Nil-SFT.jpg)

It is a query of many if we need to file a nil statement of financial transaction [SFT] if there are no prescribed transactions. One can always give preliminary response.

Table of Contents

Do we need to file Nil statement of financial transaction [SFT] or Not

SFT or statement of financial transaction : Section 285BA of the Income Tax requires specified reporting persons to furnish statement of financial transaction. Rule 114E of the Income Tax Rules, 1962 specifies that the statement of financial transaction required to be furnished under sub-section (1) of section 285BA of the Act shall be furnished in Form 61A

Do we need to file Nil statement of financial transaction [SFT] or Not

What is the periodicity and due date of furnishing statement of financial transaction

The statement of financial transactions (online return in Form No. 61A with digital signature) shall be furnished on or before 31st of May, immediately following the financial year in which the transaction is registered or recorded. Section 285BA (5) empower the tax authorities to issue a notice to a person who is required to furnish a statement as above and who has not filed the statement within prescribed time, requiring person to furnish the statement within a period not exceeding 30 days from the date of service of such notice and in such case, the person shall furnish the statement within the time as specified in the notice

Do we need to file Nil SFT or Not

Language of Act:

Obligation to furnish statement of financial transaction or reportable account.

285BA.(1) Any person, being

(a) an assessee; or

(b) the prescribed person in the case of an office of Government; or

(c) a local authority or other public body or association; or

(d) the Registrar or Sub-Registrar appointed under section 6 of the Registration Act, 1908 (16 of 1908); or

(e) the registering authority empowered to register motor vehicles under Chapter IV of the Motor Vehicles Act, 1988 (59 of 1988) ; or

(f) the Post Master General as referred to in clause (j) of section 2 of the Indian Post Office Act, 1898 (6 of 1898) ; or

(g) the Collector referred to in clause (g) of section 3 of the Right to Fair Compensation and Transparency in Land Acquisition, Rehabilitation and Resettlement Act, 2013 (30 of 2013) ; or

(h) the recognised stock exchange referred to in clause (f) of section 2 of the Securities Contracts (Regulation) Act, 1956 (42 of 1956) ; or

(i) an officer of the Reserve Bank of India, constituted under section 3 of the Reserve Bank of India Act, 1934 (2 of 1934) ; or

(j) a depository referred to in clause (e) of sub-section (1) of section 2 of the Depositories Act, 1996 (22 of 1996) ; or

(k) a prescribed reporting financial institution,

who is responsible for registering, or, maintaining books of account or other document containing a record of any specified financial transaction or any reportable account as may be prescribed, under any law for the time being in force, shall furnish a statement in respect of such specified financial transaction or such reportable account which is registered or recorded or maintained by him and information relating to which is relevant and required for the purposes of this Act, to the income-tax authority or such other authority or agency as may be prescribed.

[Furnishing of statement of financial transaction.

114E.(1) The statement of financial transaction required to be furnished under sub-section (1) of section 285BA of the Act shall be furnished in respect of a financial year inForm No. 61Aand shall be verified in the manner indicated therein.

(2) The statement referred to in sub-rule (1) shall be furnished by every person mentioned in column (3) of the Table below in respect of all the transactions of the nature and value specified in the corresponding entry in column (2) of the said Table in accordance with the provisions of sub-rule (3), which are registered or recorded by him on or after the 1st day of April, 2016

Conclusion : As per Section 285BA of Income Tax Act Read with Rule 114E of Income Tax Rules, Specified Persons having Specified financial transaction or reportable account shall furnish statement of financial transaction with Income Tax Authorities.

Income Tax Act does not specifically mandate filing of nil SFT.

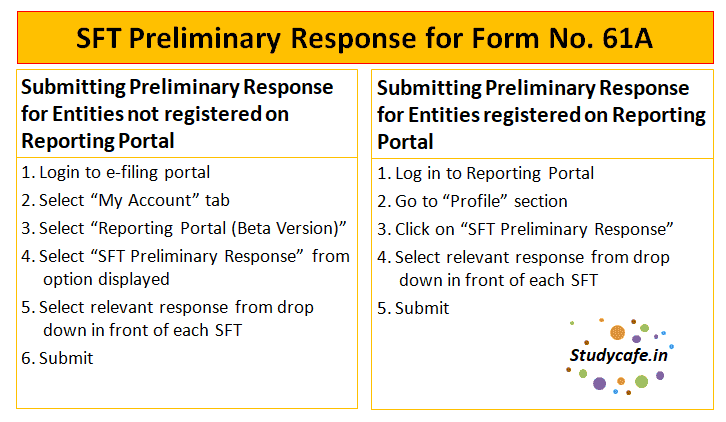

Further CBDT has released aPress Release on 26/05/2017 which says that The registration of reporting person (ITDREIN registration) is mandatory only when at least one of the Transaction Type is reportable. A functionality "SFT Preliminary Response" has been provided on the e-Filing portal for the reporting persons to indicate that a specified transaction type is not reportable for the year.

Therefore it can be concluded that is not Mandatory to file NIL Statement. However it is advisable to submit SFT Preliminary Response.

About Author

CA Deepak Gupta

Co Founder

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 3423

3423My Recent Articles

- UltraTech Cement slapped with Rs. 808.78 Cr Income Tax Demand

- GST: High Court upheld constitutional validity of Section 16(2)(c), asks government to address ITC issues of genuine purchasers

- Old vs New Tax Regime for Tax Year 2026-27

- High court criticizes Income Tax Department for not releasing ITR Utilities despite 11 years of directions

- Fino Payments Bank CEO Rishi Gupta Gets Bail in GST Case, Bank Clarifies No Direct Link

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.