Eway Bill: Documents Checklist at the Time of Transportation of Goods:

Know the mandatory documents for transporting goods under GST and the penalties if one does not comply with the GST rules for E-way Bills.

E-Way Bill: What are the Documents Required For Transporting Goods

Table of Contents

Eway Bill: Documents Checklist at the Time of Transportation of Goods

The E-Way Bill is a key part of India's Goods and Services Tax (GST) rules. As per Section 68 and Rule 138 of the GST Act, 2017, it is compulsory to generate an e-way bill when transporting goods worth over Rs. 50,000. Non-compliance can lead to penalties.

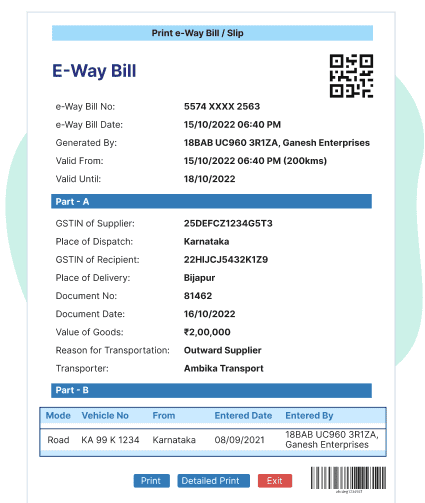

An E-Way Bill is a document you need to generate when transporting goods above the value of Rs. 50,000. It is made on the GST e-way bill portal and helps track the movement of goods during transport. It has two parts:

Part A: This includes GSTIN of both the seller and the buyer, the delivery location with its PIN code, the invoice or challan number along and the date, value of the goods, HSN code and transport document number or the reason why the goods are being transported.

Part A: This includes the information of the transporter, like the vehicle number or transporter ID.

After the E-Way Bill is created, an E-Way Bill Number (EBN) is given to the supplier, the person transporting the goods, and the recipient. This process enhances the transparency in the supply chain.

An E-Way Bill is a document you need to generate when transporting goods above the value of Rs. 50,000. It is made on the GST e-way bill portal and helps track the movement of goods during transport. It has two parts:

Part A: This includes GSTIN of both the seller and the buyer, the delivery location with its PIN code, the invoice or challan number along and the date, value of the goods, HSN code and transport document number or the reason why the goods are being transported.

Part A: This includes the information of the transporter, like the vehicle number or transporter ID.

After the E-Way Bill is created, an E-Way Bill Number (EBN) is given to the supplier, the person transporting the goods, and the recipient. This process enhances the transparency in the supply chain.

1. Registered person who causes movement of goods of consignment value exceeding fifty thousand rupees

1. Registered person who causes movement of goods of consignment value exceeding fifty thousand rupees

1. Penalties: As per Section 122 of the CGST Act, if goods are transported without a valid E-Way Bill, a fine of Rs. 10,000 or the tax that was evaded (which is higher) will be levied.

2. Confiscation of goods: In the event that the goods are being transported without supporting documents, these can be halted and confiscated under Section 129 of the CGST Act. For their release, the owner has to pay either 100% of payable tax or, in case of disagreement by the owner with respect to the tax, 50% of goods' value.

3. Interruption in Supply Chain: Not following E-Way Bill rules can interrupt business activities by leading to delays in transport and delivery. Additionally, vehicles may also be seized, leading to inefficiencies. It can also harm your business’s image.

1. Penalties: As per Section 122 of the CGST Act, if goods are transported without a valid E-Way Bill, a fine of Rs. 10,000 or the tax that was evaded (which is higher) will be levied.

2. Confiscation of goods: In the event that the goods are being transported without supporting documents, these can be halted and confiscated under Section 129 of the CGST Act. For their release, the owner has to pay either 100% of payable tax or, in case of disagreement by the owner with respect to the tax, 50% of goods' value.

3. Interruption in Supply Chain: Not following E-Way Bill rules can interrupt business activities by leading to delays in transport and delivery. Additionally, vehicles may also be seized, leading to inefficiencies. It can also harm your business’s image.

Here are the documents that you must submit to avoid any unnecessary penalties

Here are the documents that you must submit to avoid any unnecessary penalties

Make sure the GST rules related to generation of these documents are followed when creating them.

What is an E-Way Bill?

An E-Way Bill is a document you need to generate when transporting goods above the value of Rs. 50,000. It is made on the GST e-way bill portal and helps track the movement of goods during transport. It has two parts:

Part A: This includes GSTIN of both the seller and the buyer, the delivery location with its PIN code, the invoice or challan number along and the date, value of the goods, HSN code and transport document number or the reason why the goods are being transported.

Part A: This includes the information of the transporter, like the vehicle number or transporter ID.

After the E-Way Bill is created, an E-Way Bill Number (EBN) is given to the supplier, the person transporting the goods, and the recipient. This process enhances the transparency in the supply chain.

Persons Required to Generate E-Way Bill

1. Registered person who causes movement of goods of consignment value exceeding fifty thousand rupees

- in relation to a supply; or

- for reasons other than supply; or

- due to inward supply from an unregistered person

- The consignor or consignee, as a registered person or a transporter of the goods can generate the e-way bill.

- The unregistered transporter can enroll on the common portal and generate the e-way bill for movement of goods for his/her clients.

- Any citizen, other than the above, can also generate the e-way bill for movement of goods for his/her own use.

What Happens If You Do Not Comply With E-Way Bill Rules?

1. Penalties: As per Section 122 of the CGST Act, if goods are transported without a valid E-Way Bill, a fine of Rs. 10,000 or the tax that was evaded (which is higher) will be levied.

2. Confiscation of goods: In the event that the goods are being transported without supporting documents, these can be halted and confiscated under Section 129 of the CGST Act. For their release, the owner has to pay either 100% of payable tax or, in case of disagreement by the owner with respect to the tax, 50% of goods' value.

3. Interruption in Supply Chain: Not following E-Way Bill rules can interrupt business activities by leading to delays in transport and delivery. Additionally, vehicles may also be seized, leading to inefficiencies. It can also harm your business’s image.

Penalties for Transporting Goods Without Proper Documents or Tax Payment

If the supplier moves goods without paying any tax and submitting proper documents, the penalty is 100% of the tax on the goods' value. For exempt goods, it's 2% of the value or Rs. 25,000, whichever is less. In case tax is paid but valid documents are not submitted, the penalty is 50% of the goods' value. For exempt goods, it's 5% of the value or Rs. 25,000, whichever is less.Basic Document Checklist For Transporting Goods

| S. No | Type of Movement | Documents Required |

| 1 | Taxable Supply | Tax Invoice and E-Way Bill |

| 2 | Export | Export Invoice and E-Way Bill |

| 3 | Import | Bill of Entry and E-Way Bill |

| 4 | Sales Return | Delivery Challan and E-Way Bill |

| 5 | Sent for Job Work | Delivery Challan (Rule 55) and E-Way Bill |

| 6 | Return from Job Work | Endorsed Challan, Job Worker Invoice and E-Way Bill |

| 7 | Inter-branch Transfer | Tax Invoice and E-Way Bill |

| 8 | Goods for Own Use | Delivery Challan and E-Way Bill |

| 9 | Exhibition/Fair | Delivery Challan and E-Way Bill (Invoice later if sold) |

E-Way Bill penalty of Rs. 1000 for minor defaults

a) Spelling mistakes in the name of the consignor or the consignee but the GSTIN, wherever applicable, is correct; b) Error in the pin-code but the address of the consignor and the consignee mentioned is correct, subject to the condition that the error in the PIN code should not have the effect of increasing the validity period of the e-way bill; c) Error in the address of the consignee to the extent that the locality and other details of the consignee are correct; d) Error in one or two digits of the document number mentioned in the e-way bill; e) Error in 4 or 6 digit level of HSN where the first 2 digits of HSN are correct and the rate of tax mentioned is correct; f) Error in one or two digits/characters of the vehicle number. In case of minor discrepancies in the details mentioned in the e-way bill although there are no major lapses in the invoices accompanying the goods in movement, No detention and seizure of goods and conveyances should take place.About Author

Nidhi

Content Writer

Nidhi is a skilled content writer specializing in personal finance. She creates clear, engaging articles on mutual funds, investments, insurance, and wealth-building strategies. With a passion for simplifying complex financial topics, Nidhi helps readers make informed money decisions with confidence. She can be reached at [email protected]

Nidhi is a skilled content writer specializing in personal finance. She creates clear, engaging articles on mutual funds, investments, insurance, and wealth-building strategies. With a passion for simplifying complex financial topics, Nidhi helps readers make informed money decisions with confidence. She can be reached at [email protected]

Studycafe

Studycafe New Delhi, Delhi, India

New Delhi, Delhi, India 1832

1832My Recent Articles

- Karnataka High Court Gives Another Chance in GST Matter Due to Lack of Hearing

- Delay Should Be Condoned if Explanation is Unrefuted: ITAT

- Non-Service of Income Tax Notice, Ill health of taxpayer, ITAT condones Appeal filing delay

- Books of Accounts Cannot be Rejected Without Any Specific Defect: ITAT Kolkata

- Karnataka High Court Sends ITC Matter Back to GST Authorities for Reconsideration

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.