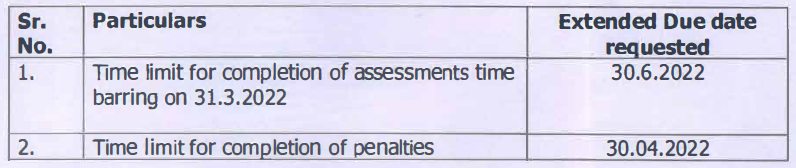

Extend Time Limit for Assessment cases time barring as on 31.03.22 under Income Tax Act

Extend Time Limit for Assessment cases time barring as on 31.03.22 under Income Tax Act The Lucknow CA Tax Practitioners Association made representat…

Table of Contents

Extend Time Limit for Assessment cases time barring as on 31.03.22 under Income Tax Act

The Lucknow CA Tax Practitioners Association made representation to Hon'ble Finance Minister Nirmala Sitharaman on Extension of Time Limit for Assessment cases time barring as on 31.03.22 under Income Tax Act 1961.

The Representation is Given Below:

Lucknow CA Tax Practitioners Association is a voluntary non-profit organization at Lucknow (U.P.) formed with Primary Object of educating and updating its members in Industry and in practice on the issues relating to Taxation and allied laws. It is always endeavour of our association to be a forum through which the issues and grievances of the stake holders can be addressed before the Tax Authorities/ Administration through effective representation.

At the outset we would like to apprise your goodslelf about the ongoing status of Assessment proceedings which are time barring as on 31.3.2022. These assessments include -i) Assessment as per the new faceless procedure u/s 144B of IT Act and ii) Reopened Assessments pending u/s 148 read with section 143(2) of IT Act. In addition to this there are thousands of penalties time barring as on 31.3.2022 which are also to be completed on Faceless module.

It is gathered that around 1,56,000 Assessment cases and around 56000 penalties are to be completed/disposed off by 31st march 2022.

Problems faced in completion of Reopened Assessment cases getting time barred on 31st March 2022:-

- Owing to the amendment made in the Finance Act, 2021 cases from AY 2014-15 to AY 2017-18 were reopened together on 31st March 2021 and which are now getting time barred on 31.3.2022, resulting in increase in quantum of cases in one year.

- Since these cases are to be completed on faceless module, there are teething problems being faced by tax payers/assessees in as much as in most cases reasons and satisfaction recorded for re-opening of assessment has not been provided to the assessees.

- In many cases the Faceless authorities have only send synopsis of reasons rather than sending the complete reasons which is in grave violation of judgement of Hon'ble Supreme Court in the case of GKN Drive Shafts (India)P. Ltd. reported in 259 ITR 19.

- Objection filed for re-opening of cases have not been disposed off by the Faceless authorities and they have proceeded to issue show cause notices.

- In several cases show notices for compliance have been issued for the first time only at the fag end of time barring period, giving time limit to make compliance in 2 or 3 days which is practically impossible and this will pave the way for passing ex-parte assessments which is certainly not the intent of the present government as this is creating unwarranted commotion and uncertainty amongst tax payers/assessees.

- In many cases Faceless authorities have not confronted the complete information/evidence available with them and as a result the assessee/ tax payers are unable to furnish proper reply.

- In several cases notice could not be served properly owing to non-availability of email id and phone numbers and such cases are lying un-complied on faceless module and no attempts have been made by department in serving the notices through physical mode of service and if such cases are completed ex-parte it will cause grave injustice.

- Recently the last date for filing of tax audit returns expired on 15.3.2022 and most of the tax payers/ assessees/ tax professionals were involved in the filing of returns and with issue of shown cause notices giving such fewer time is putting the taxpayers and tax practitioners under undue stress.

- Further, the department has also started issuing notices u/s 148A of the Income Tax Act, 1961 for AY 2018-19 as per the new procedure laid in Finance Act, 2021. All these notices have been issued only after 15.3.2022 leaving no or very less time for the tax payers to file their objections as per the procedure laid down u/s 148A(b) of IT Act. This is also creating utmost chaos as all the dates are overlapping with each other.

- It has been gathered that pushing of the cases to the Faceless Assessing Officers (FAO) were actually started in the month of November, 2021 thus restricting the effective period. It is also gathered from the officials that new cases have been allotted subsequently and it still continues.

Problems faced in completion of Assessment as per the new faceless procedure u/s 1448 of IT Act cases getting time barred on 31st March 2022:-

- In many cases show causes have not been issued and the assessees have not been granted Video Conferencing.

- In several cases compliances have been made by assessees but no show cause has been issued till date and it will not be possible for the tax payer to present its case if the final show cause is issued at the fag end of time barring assessments giving only one or two days' time to make compliance.

Problems faced in completion of Search Assessment cases getting time barred on 31st March 2022

- The Finance Bill 2022 provided extended time limit for search cases by retrospective amendment in section 153B and 153 but since the Bill has not been passed, it is creating uncertainty in completion of search cases and in absence of proper time it will result in high-pitched /expartee assessments.

Problems faced in Penalties time barring as on 31st March 2022

- In case of penalties there are several old penalties in which appeal has already been filed and are under abeyance. Yet the faceless penalty authorities are repeatedly issuing penalty show cause notices. It seems there is lack of data interface in Faceless regime as in cases where appeal is pending before first appellate authorities, penalty notices should not be issued. Non-compliance of these notice is resulting into levy of penalty even when appeal is pending.

- In cases filed under Vivad se Vishwas scheme penalty notices are also issued even when cases have been closed under VSV. It again shows that there is lack of data interface as the faceless penalty authorities should not issue penalty show causes where VSV has been opted.

- In several cases where immunity has been opted u/s 270AA of Income Tax Act, 1961 in respect of penalty u/s 270A, the Faceless penalty authorities are not considering the form 68 filed electronically through e-proceeding and are insisting on manual filing of form 68 even though there is no such procedure laid down under income tax rules nor mentioned in form 68.

PRAYER

Our association pleads for extension of the aforesaid time limits and considering our above grievances the same would be fair and reasonable and will maintain harmony amongst the taxpayers/ stake holders. For Official Copy of Representation Download PDF Given Below:About Author

Reetu

Content Manager

Reetu is a Content Writer with 4+ years of experience in GST, Income Tax, Finance, Company Law, Education and Career Related Content. She is a B.COM (Honrs.) Graduate.

Reetu is a Content Writer with 4+ years of experience in GST, Income Tax, Finance, Company Law, Education and Career Related Content. She is a B.COM (Honrs.) Graduate.

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 8072

8072My Recent Articles

- Income Tax Guide for Indian Defence Personnel for Tax Filing, Taxable Allowances and Other Benefits

- Income Tax Return Breaking: ITR Forms released for AY 25-26

- Ex-DRT Officials Sentenced to 5 Years Rigorous Imprisonment by Madras High Court along with Rs.27 Lakh Fine

- GSTN issued Advisory on Case Sensitivity in IRN Generation

- RBI to issue Notes of Rs.10 and Rs.500 bearing Signature of Guv Malhotra

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

Recent Posts

All Posts