GST Dept. issued clarification w.r.t. claiming of refund of tax wrongfully paid to the govt

GST Dept. issued clarification w.r.t. claiming of refund of tax wrongfully paid to the govt The GST Department issued Clarification in respect of ref…

Table of Contents

"77. Tax wrongfully collected and paid to Central Government or State Government. - (1) A registered person who has paid the Central tax and State tax or, as the case may be, the Central tax and the Union territory tax on a transaction considered by him to be an intra-State supply, but which is subsequently held.to be an inter-State supply, shall be refunded the amount of taxes so paid in such manner and subject to such conditions as may be prescribed.

(2) A registered person who has paid integrated tax on a transaction considered by him to be an inter-State supply, but which is subsequently held to be an intra-State supply, shall not be required to pay any interest on the amount of central tax and State tax or, as the case may be, the Central tax and the Union territory tax payable. "

Section 19 of the IGST Act, 2017 reads as follows:·"19. Tax wrongfully collected and paid to Central Government of State Government-----(1) A registered person who has paid integrated tax on a supply considered by him to be an inter-State supply, but which is subsequently held to be an intra-State supply, shall be granted refund of the amount of integrated tax so paid in such manner and subject to such condition as may be prescribed .

(2) A registered person who has paid central tax and State tax or Union territory tax, as the case may be, on a transaction considered by him to be an intra-State supply, but which is subsequently held to be an inter-State supply, shall not be required to pay any interest on the amount of integrated tax payable."

3. Interpretation of the term "subsequently held"

3.1 Doubts have been raised regarding the interpretation of the term ''subsequently held" in the aforementioned sections, and whether refund claim under the said sections is available only if supply made by a taxpayer as inter-State or intra-State, is subsequently held by tax officer as intra-State and inter-State respectively; either on scrutiny/ assessment/ audit/ investigation, or as a result of any adjudication, appellate or any other proceeding or whether the refund under the said sections is also available when the inter-State or intra-State supply made by a taxpayer, is subsequently, found by taxpayer himself as intra-State and inter-State respectively. 3.2 In this regard, it is clarified that the term "subsequently held" in section 77 of UPSGST Act, 2017 or under section 19 of IGST Act, 2017 covers both the cases where the inter-State or inter-State supply made by a taxpayer, is either subsequently found by taxpayer himself as intra-State or inter-State respectively or where the inter-State or intra-State supply made by a taxpayer is subsequently found/held as intra-State or inter-State respectively by the tax officer in any proceeding. Accordingly, refund claim, under the said sections can be claimed by the taxpayer in both the above mentioned situations, provided the taxpayer pays the required amount of tax in the correct head.4. The relevant date for claiming refund under Section 77 of the UPSGST Act/ Section 19 of the IGST Act, 2017

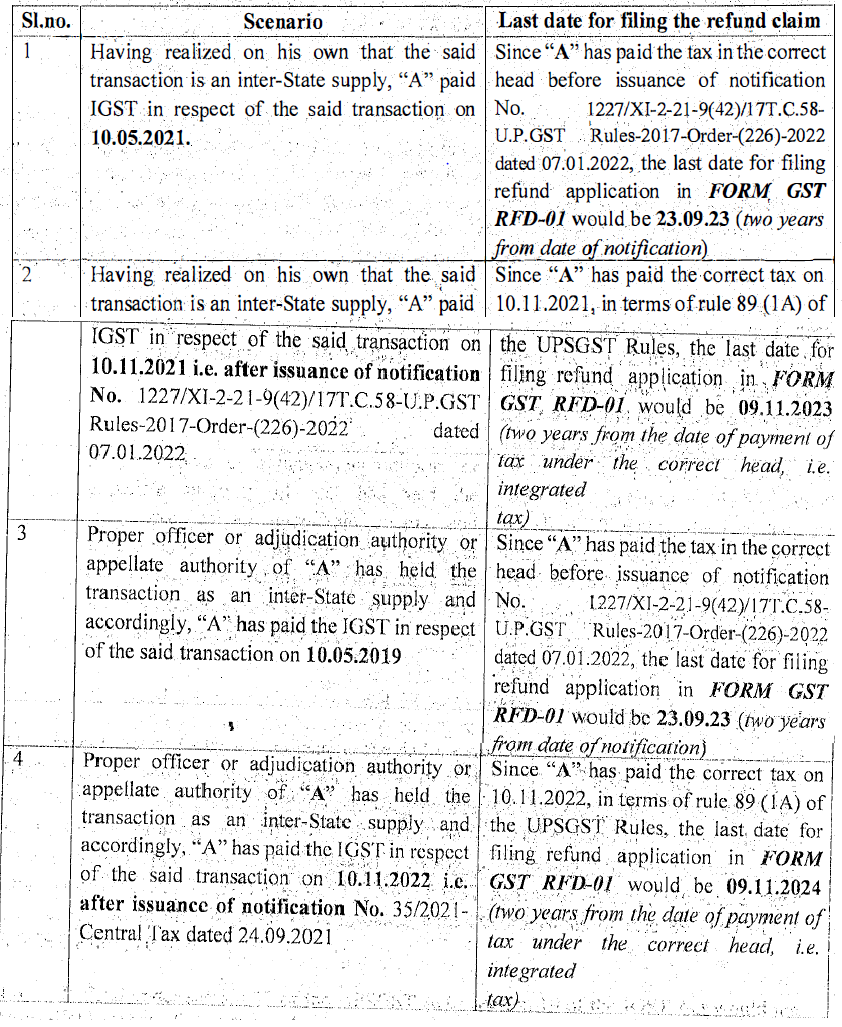

4.1 Section 77 of the UPSGST Act and Section 19 of the IGST Act, 2017 provide that in case a supply earlier considered by a taxpayer as intra-State or inter-State, is subsequently held as inter-State or intra-State respectively, the amount of central and state tax paid or integrated tax paid, as the case may be, on such supply shall be refunded in such manner and subject to such conditions as may be prescribed. In order to prescribe the manner and conditions for refund under section 77 of the UPSGST Act and section 19 of the IGST Act, sub-rule (1A) has been inserted after sub-rule (1) of rule 89 of the Uttar Pradesh Goods and Services Tax Rules, 2017(hereinafter referred to as "UPSGST Rules") vide notification No.1227/XI-2-21-9(42)/17T.C.58-U.P.GST Rules-2017-Order-(226)-2022 dated 07.01.2022. The said sub-rule (1A) of rule 89 of UPSGST Rules, 2017 read as follows:"(1A) Any person, claiming refund under section 77 of the Act of any tax paid by him, in respect of a transaction considered by him to be an intra-State supply, which is subsequently held to be an inter-State supply, may before the expiry, of a period of two years from the date of payment of the tax on the inter-State supply, file an application of electronically in FORM GST RFD-01 through the common portal, either directly or through a Facilitation Centre notified by the Commissioner:

Provided that the said application . may, as regard to any, payment of tax on inter-State supply before coming into force of this sub-rule, be filed before the expiry of a period of two years from the date on which this sub-rule comes into force."

4.2 The aforementioned amendment in the rule 89 of UPSGST Rules, 2017 clarifies that the refund under section 77 of UPSGST Act/ Section 19 of IGST Act, 2017 can be claimed before the expiry of two years from the date of payment of tax under the correct head, i.e integrated tax paid in respect of subsequently held inter-State supply, or central and state tax in respect of subsequently held intra-State supply, as the case may be. However, in cases, where the taxpayer has made the payment in the correct head before the date of issuance of notification No.1227/XI-2-21-9(42)/17T.C.58-UPGST Rules-2017-0rder-(226)-2022 dated 07.01.2022, the refund application under section 77 of the, UPSGST Act/ section 19 of the IGST Act can be, filed before the expiry of two years from the date of issuance of the said notification. i.e. from 24.09.2021. 4.3 Application of sub-rule (1A) of rule 89 read with section 77 of the UPSGST Act / section 19 of the IGST Act is explained through following illustrations.A taxpayer “A” has issued the invoice dated 10.03.2018 charging UPSGST and SGST on a transaction and accordingly paid the applicable tax (UPSGST and SGST) in the return for March, 2018 tax period. The following scenarios are explained hereunder:

To Read Full Representation Download PDF Given Below:

To Read Full Representation Download PDF Given Below:About Author

Reetu

Content Manager

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 8072

8072My Recent Articles

- Income Tax Guide for Indian Defence Personnel for Tax Filing, Taxable Allowances and Other Benefits

- Income Tax Return Breaking: ITR Forms released for AY 25-26

- Ex-DRT Officials Sentenced to 5 Years Rigorous Imprisonment by Madras High Court along with Rs.27 Lakh Fine

- GSTN issued Advisory on Case Sensitivity in IRN Generation

- RBI to issue Notes of Rs.10 and Rs.500 bearing Signature of Guv Malhotra

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts