GSTAT has No Jurisdiction to Extend Due Date: 30th June last date to clear backlog of appeals:

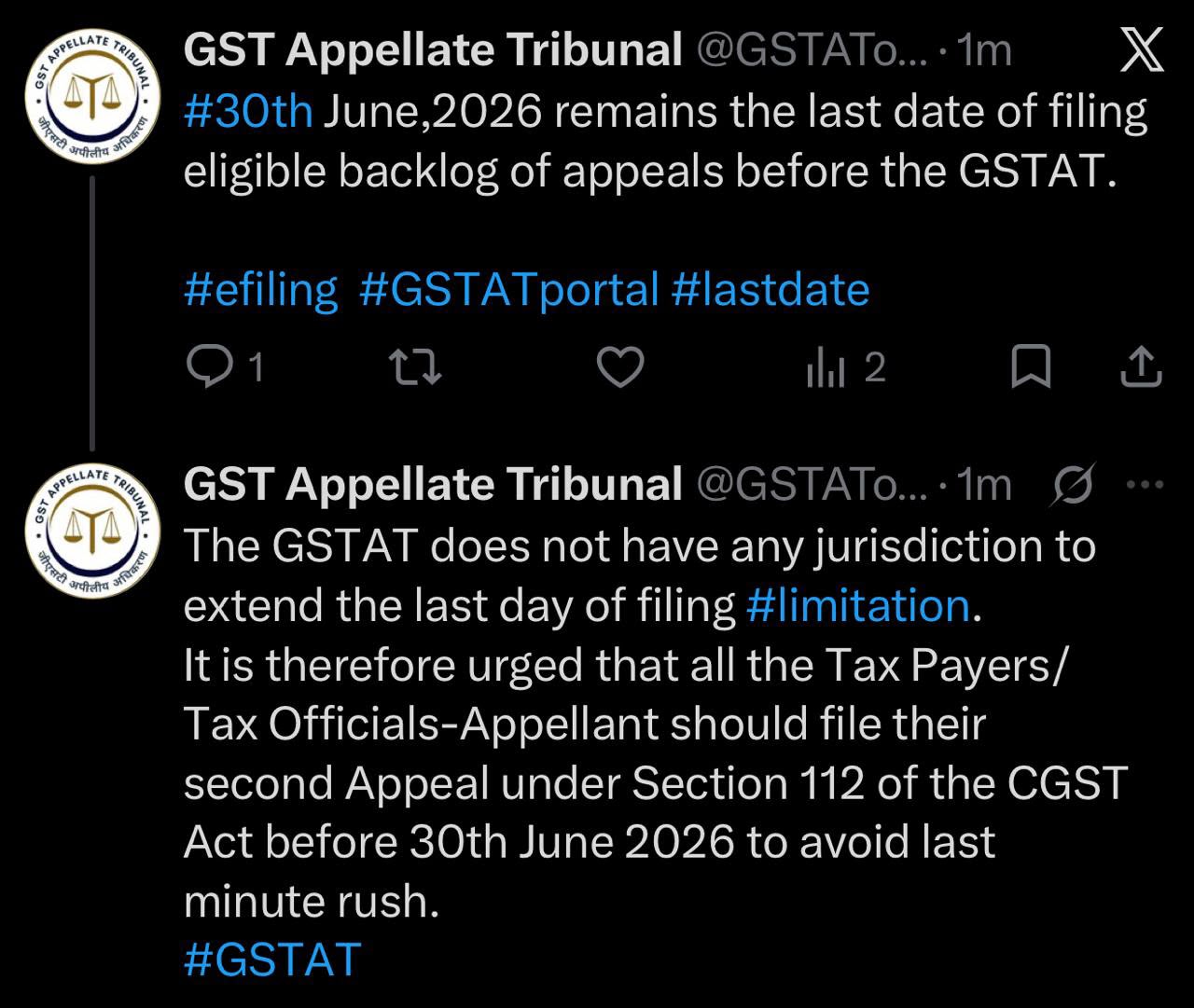

The GSTAT has officially clarified that it does not have the jurisdiction to extend the due date of filing a second appeal under Section 112 of the CGST act; taxpayers are urged to file appeals before June 30, 2026.

Taxpayers Advised to File Section 112 Second Appeal Before June 30

GSTAT has No Jurisdiction to Extend Due Date: 30th June last date to clear backlog of appeals

The GST Appellate Tribunal (GSTAT) in a recent announcement has clarified that it does not have authority or jurisdiction to extend the due date of filing a second appeal under Section 112 of the Central Goods and Services Tax (CGST) Act.

The due date for filing eligible backlog appeals before the Tribunal through the e-filing system is June 30, 2026. It has been strictly asserted that appeals filed after this date will not be entertained; consequently, taxpayers/tax officials who are appellants are advised to file the appeals before the prescribed deadline, as they will not be granted any extra time limit thereafter.

The GSTAT further highlighted that appellants should not wait until the last moment to submit their appeals, as this can result in unnecessary delays and technical issues. All eligible appellants are urged to make use of the e-filing portal and submit their second appeals well before the deadline to avoid a last-minute rush and procedural complications.

Deadlines for GSTAT appeals:

1. Backlog Appeals

The GSTAT further highlighted that appellants should not wait until the last moment to submit their appeals, as this can result in unnecessary delays and technical issues. All eligible appellants are urged to make use of the e-filing portal and submit their second appeals well before the deadline to avoid a last-minute rush and procedural complications.

Deadlines for GSTAT appeals:

1. Backlog Appeals

The GSTAT further highlighted that appellants should not wait until the last moment to submit their appeals, as this can result in unnecessary delays and technical issues. All eligible appellants are urged to make use of the e-filing portal and submit their second appeals well before the deadline to avoid a last-minute rush and procedural complications.

Deadlines for GSTAT appeals:

1. Backlog Appeals

- The due date to file an appeal challenging the GST orders issued before April 01, 2026, is June 30, 2026.

- Taxpayers are given the time limit of three months (from the date of issuance of the GST orders) to file an appeal challenging the orders issued on or after April 01, 2026. An additional three months' extension can be granted for these types of appeals if the taxpayer has a relevant and genuine reason for delay.

About Author

Saloni Kumari

Content Writer

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 2484

2484My Recent Articles

- ITAT Says Identity and Creditworthiness Irrelevant Where Loan Was Directly Paid to Haryana Mining DepartmentPremium

- Earlier Rejection Cannot Be Sole Ground to Reject Fresh Section 12AB and 80G Registration Applications, Says ITATPremium

- Cash Deposited During Demonetisation Cannot Be Taxed Under Section 69A if Linked to Business, Holds ITAT Premium

- ITAT Condones 1,731-Day Delay, Remands Cancer Trust's Section 12A Registration Application for Fresh ConsiderationPremium

- ITAT Lowers Estimated Profit Rate from 8% to 4% After Considering State Shutdown and Medicine Trade MarginsPremium

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts