Guidelines for Compulsory Selection of Income tax Returns for Complete Scrutiny for FY 2023-24:

The Central Board of Direct Taxes(CBDT) has notified Guidelines for compulsory selection of returns for Complete Scrutiny during the Financial Year 2023-24.

Guidelines for Compulsory Selection of Returns

Guidelines for Compulsory Selection of Income tax Returns for Complete Scrutiny for FY 2023-24

The Central Board of Direct Taxes(CBDT) has notified Guidelines for compulsory selection of returns for Complete Scrutiny during the Financial Year 2023-24.

The parameters for compulsory selection of returns for Complete Scrutiny during Financial Year 2023-24 and procedure for compulsory selection in such cases are prescribed as under:

It is clarified that where return has been furnished in response to notice u/s 142(1) of the Act and such notice u/s 142(1) of the Act was issued due to the information contained in NMS Cycle/ AIS/ Statement of Financial Transactions (SFT)/ CPC-TDS information/ information received from Directorate of I&CI, such return will not be taken up for compulsory scrutiny. Selection of such cases for scrutiny will be done through CASS cycle.

The cases shall be selected for compulsory scrutiny by the International Taxation and Central Circle charges following the above prescribed parameters and procedure with prior administrative approval of Pr.CIT/Pr.DIT/CIT/DIT concerned. The information pertaining to Compulsory Scrutiny may not be transferred to NaFAC unless the case itself transferred. It is further clarified that communication to NaFAC for access and/or further action after selection for Compulsory Scrutiny will not apply to the International taxation and Central charges.

The cases which are selected for compulsory scrutiny by the International Taxation and Central Circle charges following the above parameters and procedure prescribed at Para 2, shall continue to be handled by International Taxation and Central Circle charges respectively, as earlier.

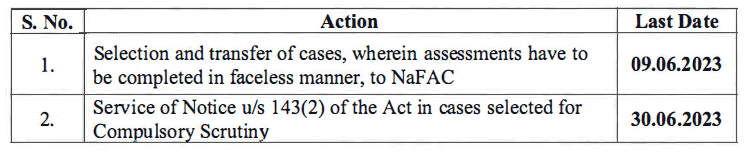

As per the amendments brought by Finance Act 2021, the time limit for service of notice u/s 143(2) of the Act has been reduced to three months from end of the Financial Year in which the return is filed.

(i) Therefore, for actions related to cases under Parameters at S.No.4(ii), 5, 6 and 7 of Para 2 above, the following timelines shall be followed:

It is clarified that where return has been furnished in response to notice u/s 142(1) of the Act and such notice u/s 142(1) of the Act was issued due to the information contained in NMS Cycle/ AIS/ Statement of Financial Transactions (SFT)/ CPC-TDS information/ information received from Directorate of I&CI, such return will not be taken up for compulsory scrutiny. Selection of such cases for scrutiny will be done through CASS cycle.

The cases shall be selected for compulsory scrutiny by the International Taxation and Central Circle charges following the above prescribed parameters and procedure with prior administrative approval of Pr.CIT/Pr.DIT/CIT/DIT concerned. The information pertaining to Compulsory Scrutiny may not be transferred to NaFAC unless the case itself transferred. It is further clarified that communication to NaFAC for access and/or further action after selection for Compulsory Scrutiny will not apply to the International taxation and Central charges.

The cases which are selected for compulsory scrutiny by the International Taxation and Central Circle charges following the above parameters and procedure prescribed at Para 2, shall continue to be handled by International Taxation and Central Circle charges respectively, as earlier.

As per the amendments brought by Finance Act 2021, the time limit for service of notice u/s 143(2) of the Act has been reduced to three months from end of the Financial Year in which the return is filed.

(i) Therefore, for actions related to cases under Parameters at S.No.4(ii), 5, 6 and 7 of Para 2 above, the following timelines shall be followed:

(ii) For all the cases selected for Compulsory Scrutiny, service of Notice u/s 143(2) of the Act shall be completed within the statutory time line i.e., by 30.06.2023.

For Official Guidelines Download PDF Given Below:

(ii) For all the cases selected for Compulsory Scrutiny, service of Notice u/s 143(2) of the Act shall be completed within the statutory time line i.e., by 30.06.2023.

For Official Guidelines Download PDF Given Below:

It is clarified that where return has been furnished in response to notice u/s 142(1) of the Act and such notice u/s 142(1) of the Act was issued due to the information contained in NMS Cycle/ AIS/ Statement of Financial Transactions (SFT)/ CPC-TDS information/ information received from Directorate of I&CI, such return will not be taken up for compulsory scrutiny. Selection of such cases for scrutiny will be done through CASS cycle.

The cases shall be selected for compulsory scrutiny by the International Taxation and Central Circle charges following the above prescribed parameters and procedure with prior administrative approval of Pr.CIT/Pr.DIT/CIT/DIT concerned. The information pertaining to Compulsory Scrutiny may not be transferred to NaFAC unless the case itself transferred. It is further clarified that communication to NaFAC for access and/or further action after selection for Compulsory Scrutiny will not apply to the International taxation and Central charges.

The cases which are selected for compulsory scrutiny by the International Taxation and Central Circle charges following the above parameters and procedure prescribed at Para 2, shall continue to be handled by International Taxation and Central Circle charges respectively, as earlier.

As per the amendments brought by Finance Act 2021, the time limit for service of notice u/s 143(2) of the Act has been reduced to three months from end of the Financial Year in which the return is filed.

(i) Therefore, for actions related to cases under Parameters at S.No.4(ii), 5, 6 and 7 of Para 2 above, the following timelines shall be followed:

(ii) For all the cases selected for Compulsory Scrutiny, service of Notice u/s 143(2) of the Act shall be completed within the statutory time line i.e., by 30.06.2023.

For Official Guidelines Download PDF Given Below:About Author

Reetu

Content Manager

Reetu is a Content Writer with 4+ years of experience in GST, Income Tax, Finance, Company Law, Education and Career Related Content. She is a B.COM (Honrs.) Graduate.

Reetu is a Content Writer with 4+ years of experience in GST, Income Tax, Finance, Company Law, Education and Career Related Content. She is a B.COM (Honrs.) Graduate.

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 8072

8072My Recent Articles

- Income Tax Guide for Indian Defence Personnel for Tax Filing, Taxable Allowances and Other Benefits

- Income Tax Return Breaking: ITR Forms released for AY 25-26

- Ex-DRT Officials Sentenced to 5 Years Rigorous Imprisonment by Madras High Court along with Rs.27 Lakh Fine

- GSTN issued Advisory on Case Sensitivity in IRN Generation

- RBI to issue Notes of Rs.10 and Rs.500 bearing Signature of Guv Malhotra

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

Recent Posts

All Posts