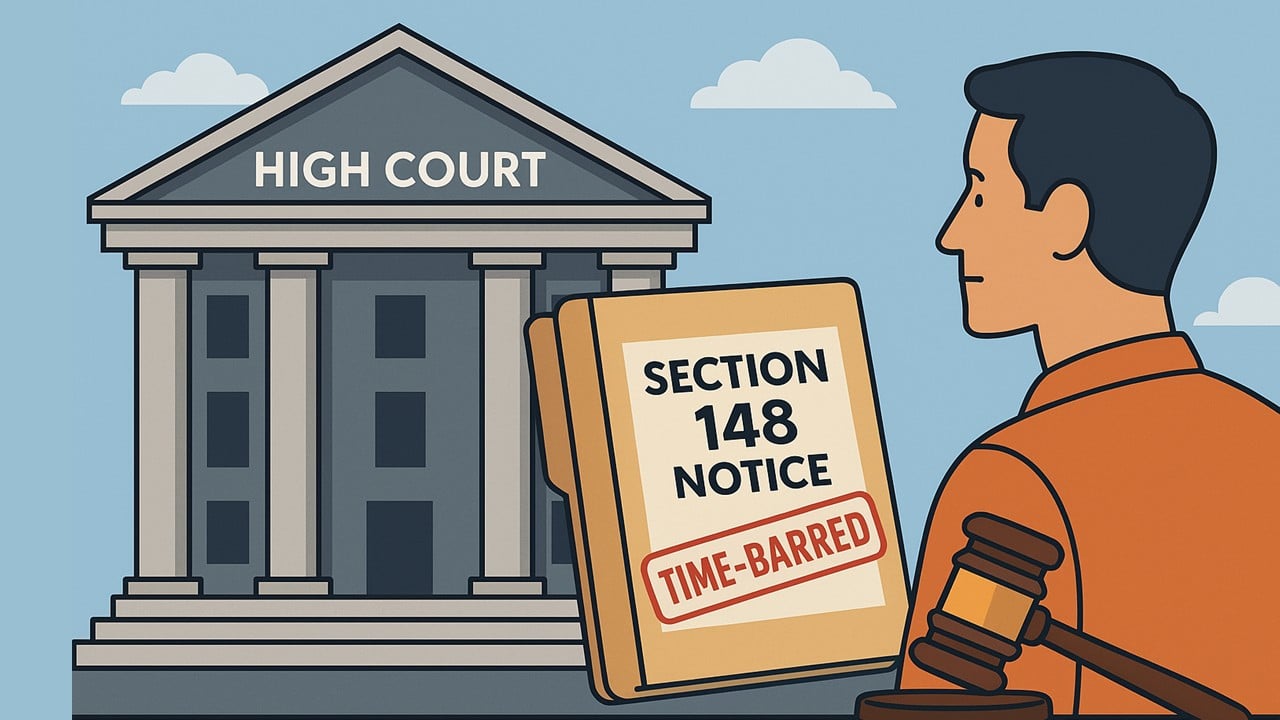

High Court Quashes Reassessment Notice u/s 148 as Time-Barred:

High Court quashes reassessment notice u/s 148 dated 31.07.2022 as time-barred; all consequential proceedings set aside.

Notice under Section 148 held invalid as issued beyond the surviving time period; consequential proceedings also quashed

High Court Quashes Reassessment Notice u/s 148 as Time-Barred

The petitioner came to the Court challenging the reassessment proceedings for AY 2016–2017. Notice under Section 148 of the Income-tax Act, 1961, was issued to him on 31.07.2022. In accordance with the petitioner, the notice was issued after the time limit prescribed and thus without jurisdiction. It was argued that once the statutory period available to the Assessing Officer had lapsed, no fresh notice under Section 148 could be sustained in law.

The Court recorded that an earlier notice under Section 148 was issued on 15.06.2021. Pursuant to the procedure, information was furnished to the petitioner on 27.05.2022 with a time of fifteen days for reply. The reply was filed on 15.06.2022. Thereafter, the Assessing Officer proceeded to pass an order under Section 148A(d) and again issued a notice under Section 148 on 31.07.2022.

Main Issue: Whether the Section 148 notice dated 31.07.2022 was issued within time within the mandated limitation period or was time-barred.

High Court's Ruling: The Court ruled that the time limit for issuing notice under Section 148 had expired on 26.06.2022. The notice of 31.07.2022 was therefore ex facie time-barred. As soon as the very basis of reassessment was rendered jurisdictionally infirm, the consequent order made under Section 148A(d) and all subsequent proceedings fell to the ground automatically. On comparing the dates and the time limit involved, the Court noted that the period of survival for giving notice ended on 26.06.2022. Therefore, the giving of fresh notice on 31.07.2022 was well past time. The Court therefore found substance in the petitioner’s grievance that the impugned proceedings were barred by limitation.

Therefore, the Court quashed and set aside the challenged notice of 31.07.2022 and the order made under Section 148A(d) and all the consequential actions. The petition was granted and the rule was made absolute. The issue was therefore decided in favor of the petitioner.

To Read Full Judgment, Download PDF Given Below

About Author

Meetu Kumari

Content Manager

Meetu Kumari is an Experienced Advocate and Content Writer with 4+ years of demonstrated history of working in the law practice industry. Skilled in Developing Content, Researching, and Drafting. Strong professional with a Bachelor of Science (B.Sc.) focused on Law from Gujarat National Law University.

Meetu Kumari is an Experienced Advocate and Content Writer with 4+ years of demonstrated history of working in the law practice industry. Skilled in Developing Content, Researching, and Drafting. Strong professional with a Bachelor of Science (B.Sc.) focused on Law from Gujarat National Law University.

Studycafe

Studycafe Jodhpur, Rajasthan, India

Jodhpur, Rajasthan, India 2220

2220My Recent Articles

- ITAT: Carbon Credit Receipts Are Capital, Not Taxable Under Income TaxPremium

- Gujarat HC Quashes Section 148 Notice After Reassessment Proceedings Were DroppedPremium

- High Court Denies GST Refund After Delayed Tribunal Appeal Beyond Section 112 TimelinePremium

- ITAT Allows Section 10(10B) Exemption on BSNL VRS Compensation Despite Return OmissionPremium

- High Court Refuses Interference in Anti-Dumping Duty Matter Due to Alternative RemedyPremium

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts