ICAI releases Indian Accounting Standards (Ind AS) 2021

ICAI releases Indian Accounting Standards (Ind AS) 2021 Approach to IFRS-converged Indian Accounting Standards (Ind AS) First Step towards IFRS The I…

Table of Contents

First Step towards IFRS

The Institute of Chartered Accountants of India (ICAI) being the premier accounting standards-setting body in India, way back in 2006, initiated the process of moving towards the International Financial Reporting Standards (IFRS) issued by the International Accounting Standards Board (IASB) with a view to enhance acceptability and transparency of the financial information communicated by the Indian corporates through their financial statements. This move towards IFRS was subsequently accepted by the Government of India. The Government of India in consultation with the ICAI decided to converge and not to adopt IFRS issued by the IASB. The decision of convergence rather than adoption was taken after the detailed analysis of IFRS requirements and extensive discussion with various stakeholders. Accordingly, while formulating IFRS-converged Indian Accounting Standards (Ind AS), efforts have been made to keep these Standards, as far as possible, in line with the corresponding IFRS Standards (which comprise pronouncements with IAS, IFRS, SIC and IFRIC) and departures have been made where considered absolutely essential. These changes have been made considering various factors, such as, terminology related changes to make it consistent with the terminology used in law, e.g., ‘statement of profit and loss’ in place of ‘statement of comprehensive income’ and ‘balance sheet’ in place of ‘statement of financial position’. Certain other changes have been made considering the economic environment, customs and laws of the country. The ICAI while updating Ind AS, also reconsidered the carveouts made in Ind AS finalised in 2011 and decided not to continue with certain carve-outs. It was also decided to make certain new carveouts/ carve-in based on the feedback received from various stakeholders.Government of India commitment to IFRS converged Ind AS

As per the original roadmap for implementation of IFRS-converged Ind AS issued by the Government of India, initially Ind AS were expected to be implemented from the year 2011. However, keeping in view the fact that certain issues including tax issues were still to be addressed, the Ministry of Corporate Affairs decided to postpone the date of implementation of Ind AS. In 2014, the then Hon'ble Union Finance Minister of India, Late Shri Arun Jaitely, in his Budget Speech in July 2014 stated that –“There is an urgent need to converge the current Indian accounting standards with the International Financial Reporting Standards (IFRS). I propose for adoption of the new Indian Accounting Standards (Ind AS) by the Indian companies from the financial year 2015-16 voluntarily and from the financial year 2016-17 on a mandatory basis. Based on the international consensus, the regulators will separately notify the date of implementation of Ind AS for the Banks, Insurance companies etc. Standards for the computation of tax would be notified separately”.

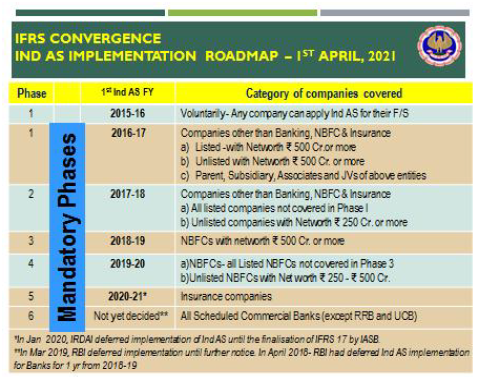

Pursuant to the above announcement, various steps were taken to facilitate the implementation of IFRS-converged Indian Accounting Standards (Ind AS). Moving in this direction, the Ministry of Corporate Affairs (MCA) has issued the Companies (Indian Accounting Standards) Rules, 2015 vide Notification dated February 16, 2015 including the revised roadmap of implementation of Ind AS for companies other than Banking companies, Insurance Companies and NBFCs. As per the Notification, Ind AS converged with IFRS shall be implemented on voluntary basis from 1st April, 2015 and mandatorily from 1st April, 2016. Further, the MCA on March 30, 2016, had also notified the Roadmap for implementation of Ind AS for Scheduled Commercial Banks, Insurance companies and NBFCs from 1st April, 2018 onwards and also amendments to Ind AS in line with the amendments made in IFRS/IAS vide Companies (Indian Accounting Standards) Amendment Rules, 2016. However, IRDAI vide press release dated June 28, 2017 had deferred the implementation of Ind AS for the Insurance Sector in India for a period of two years, whereby the effective date was deferred to FY 2020-21. Thereafter, vide circular dated January 21, 2020, IRDAI has deferred Implementation of Ind AS in the Insurance Sector till further notice. Additionally, the insurance companies are no longer required to submit proforma Ind AS financial statements to IRDAI on quarterly basis as was required earlier. The Reserve Bank of India vide its circular dated April 05, 2018 had deferred the implementation of Ind AS for Schedule Commercial Banks (SCBs), excluding Regional Rural Banks (RRBs) by one year i.e., to be made effective from 1st April, 2019 onwards. However, vide circular dated 22nd March, 2019, the implementation of Ind AS for Scheduled Commercial Banks (SCBs) has been further deferred until further notice by the Reserve Bank of India. Ind AS Implementation Roadmap is summarised below One of the most significant steps in moving towards to Ind AS taken by the ICAI was to provide a stable platform to the Indian entities for smoother and for effective implementation of Ind AS it has been decided to converge early by notifying Ind AS corresponding to IFRS 9, Financial Instruments (effective from January 01, 2018) issued by the IASB. The ICAI continues with its march towards continuous convergence with IFRS Standards at all times and closely monitors the amendments in IFRS Standards with timely incorporation of those changes in Ind ASs

The IASB issued IFRS 15, Revenue from Contracts with Customers with effect from January 01, 2018 and IFRS 16 Leases with effect from January 01, 2019. Consequently to keep in pace with the global standards, ICAI formulated Ind AS 115, Revenue from Contracts with Customers which was notified by MCA in March, 2018 effective for F.Y. 2018-19 onwards and Ind AS 116 Leases, which was notified by MCA in March, 2019 for F.Y. 2019-20 onwards. The current status of Ind AS vis-à-vis the IFRS is given in the Appendix A.

One of the most significant steps in moving towards to Ind AS taken by the ICAI was to provide a stable platform to the Indian entities for smoother and for effective implementation of Ind AS it has been decided to converge early by notifying Ind AS corresponding to IFRS 9, Financial Instruments (effective from January 01, 2018) issued by the IASB. The ICAI continues with its march towards continuous convergence with IFRS Standards at all times and closely monitors the amendments in IFRS Standards with timely incorporation of those changes in Ind ASs

The IASB issued IFRS 15, Revenue from Contracts with Customers with effect from January 01, 2018 and IFRS 16 Leases with effect from January 01, 2019. Consequently to keep in pace with the global standards, ICAI formulated Ind AS 115, Revenue from Contracts with Customers which was notified by MCA in March, 2018 effective for F.Y. 2018-19 onwards and Ind AS 116 Leases, which was notified by MCA in March, 2019 for F.Y. 2019-20 onwards. The current status of Ind AS vis-à-vis the IFRS is given in the Appendix A.

Roadmap1 for implementation of Indian Accounting Standards (Ind AS) for corporates: A Snapshot

(For Companies other than Banks, NBFCs and Insurance Companies) Phase I: 1st April 2015 or thereafter (with Comparatives): Voluntary Basis for any company and its holding, subsidiary, JV or associate company1st April 2016: Mandatory Basis

(a) Companies listed/in process of listing on Stock Exchanges in India or Outside India having net worth of INR 500 crore or more;

(b) Unlisted Companies having net worth of INR 500 crore or more;

(c) Parent, Subsidiary, Associate and JV of above.

Phase II: 1st April 2017: Mandatory Basis (with comparatives):(a) All companies which are listed/or in process of listing inside or outside India on Stock Exchanges not covered in Phase I (other than companies listed on SME Exchanges);

(b) Unlisted companies having net worth of INR 250 crore or more but less than INR 500 crore;

(c) Parent, Subsidiary, Associate and JV of above.

- Companies listed on SME exchange are not required to apply Ind AS

- Once Ind AS are applicable, an entity shall be required to follow the Ind AS for all the subsequent financial statements.

- Companies not covered by the above roadmap shall continue to apply Accounting Standards notified in Companies (Accounting Standards) Rules, 2006 (These rules have been superseded by Companies (Accounting Standards) Rules, 2021.

Roadmap2 for Implementation of Indian Accounting Standards (Ind AS) for NBFCs: A Snapshot

NBFCs

Phase I: From 1st April, 2018 (with comparatives):- NBFCs (whether listed or unlisted) having net worth of INR 500 crore or more

- Holding, Subsidiary, JV and Associate companies of above NBFC other than those already covered under corporate roadmap shall also apply from said date

- NBFCs that are unlisted having net worth of INR 250 crore or more but less INR 500 crore

- Holding, Subsidiary, JV and Associate companies of above other than those already covered under corporate roadmap shall also apply from said date

- Applicable for both Consolidated and individual Financial Statements

- NBFC having net worth below INR 250 crore shall not apply Ind AS.

- Adoption of Ind AS is allowed only when required as per the roadmap. Voluntary adoption of Ind AS is not allowed.

Insurers/ Insurance companies

IRDAI vide press release dated June 28, 2017 had deferred the implementation of Ind AS for the Insurance Sector in India for a period of two years, whereby the effective date was deferred to FY 2020-21. Thereafter, again in January 2020, IRDAI has deferred Implementation of Ind AS in the Insurance Sector till further notice.Scheduled Commercial banks (excluding Regional Rural Banks)

RBI vide press release dated April 05, 2018 had deferred the implementation of Ind AS for the Scheduled Commercial Banks (excluding Regional Rural Banks) for a period of one year i.e. effective from 1st April 2019., Thereafter, again in March 2029, RBI vide notification dated March 22, 2019 had again deferred the implementation of Ind AS for the Scheduled Commercial Banks (excluding Regional Rural Banks) till further notice. To Read Full Overview of Ind AS Download PDF Given Below :About Author

Reetu

Content Manager

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 8072

8072My Recent Articles

- Income Tax Guide for Indian Defence Personnel for Tax Filing, Taxable Allowances and Other Benefits

- Income Tax Return Breaking: ITR Forms released for AY 25-26

- Ex-DRT Officials Sentenced to 5 Years Rigorous Imprisonment by Madras High Court along with Rs.27 Lakh Fine

- GSTN issued Advisory on Case Sensitivity in IRN Generation

- RBI to issue Notes of Rs.10 and Rs.500 bearing Signature of Guv Malhotra

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts