ICAI submit Suggestions on GSTR 9 & 9C : GST Annual Return and Audit

ICAI submit Suggestions on GSTR 9 & 9C : GST Annual Return and Audit The Institute of Chartered Accountants of India considers it a priv

ICAI submit Suggestions on GSTR 9 & 9C : GST Annual Return and Audit

The Institute of Chartered Accountants of India considers it a privilege to submit its suggestions on Reconciliation Statement and Certificate in Form GSTR We shall be pleased to discuss these suggestions provided in this communication during a meeting in person, to illustrate the points made by us.

We look forward to contribute in the drafting of simple, transparent and fair GST laws in India.

Executive Summary ofSuggestions on GSTR 9 & 9C : GST Annual Return and Audit by ICAI

DETAILED SUGGESTIONS

1 . Calculation of Turnover of Rs. 2 Crore for the applicability of GST Audit

In terms of Rule 80(3) of the CGST Rules every registered person whose aggregate turnover during a financial year exceeds two crore rupees shall get his accounts audited.

Issue: Limit of Turnover of Rs. 2 Crore would be calculated from July onwards for the FY 2017-18 or the Financial year 2017-18 would be considered for the same.

Suggestion: It is suggested to provide suitable clarification in this regard.

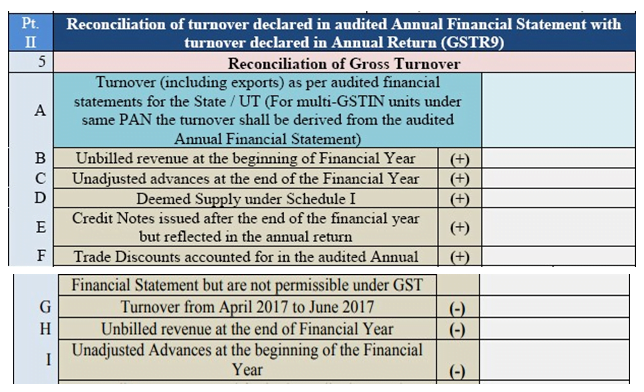

2.Turnover of multi GSTN units under same PAN

Issue:

1. Part 5B Unbilled revenue at the beginning of Financial year seems to lead to some confusion.

2. Part 5I Unadjusted advances at the beginning of the financial year seems to lead to some confusion.

3. This confusion is on account of the fact that the GST regime was effective from July 1, 2017. The question that arises is, when the form states beginning of financial year, whether information as at April 1, 2017 should be considered or as at July 1, 2017. It is clear that in respect of GST reconciliation, information must be reckoned from its inception and not earlier. For this reason, it is advisable to clear this confusion by suitably stating with reference to the date of inception of GST, that is, as at July 1, 2017.

Suggestion:

It is suggested to substitute the words at the beginning of the financial year in part 5B and 5I with words as on 30th June, 2017

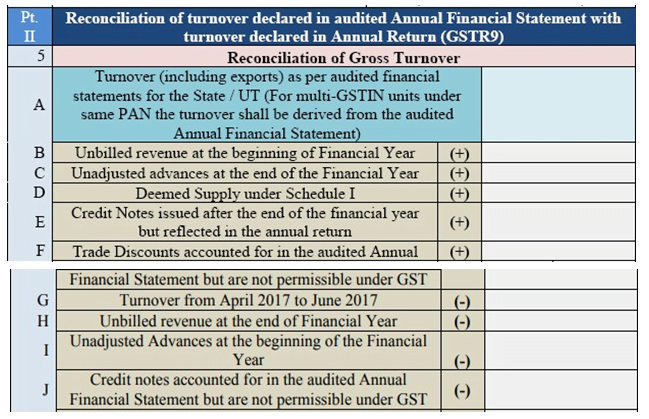

3. Credit notes issued after the end of financial year

Issue:

1. Part 5B Unbilled revenue at the beginning of Financial year seems to lead to some confusion.

2. Part 5I Unadjusted advances at the beginning of the financial year seems to lead to some confusion.

3. This confusion is on account of the fact that the GST regime was effective from July 1, 2017. The question that arises is, when the form states beginning of financial year, whether information as at April 1, 2017 should be considered or as at July 1, 2017. It is clear that in respect of GST reconciliation, information must be reckoned from its inception and not earlier. For this reason, it is advisable to clear this confusion by suitably stating with reference to the date of inception of GST, that is, as at July 1, 2017.

Suggestion:

It is suggested to substitute the words at the beginning of the financial year in part 5B and 5I with words as on 30th June, 2017

3. Credit notes issued after the end of financial year

Issue: Part 5E require reporting of credit notes issued after the end of financial year but reflected in the annual return as addition to turnover whereas part 5J requires credit notes accounted for in the audited annual financial statement but not permissible under GST as deduction.

Since the reconciliation is derived from turnover as per financial statements towards annual return, the amount of credit notes not reduced from turnover inFS till March-18 but reduced from turnover Annual Return cannot be added but be reduced from turnover in FS so as to reconcile the amount with turnover Annual Return. The symbol + is creating the confusion. Therefore, the symbol -would clear any confusion.

Also, credit notes accounted for in the audited annual financial statement but are contrary to section 34 (stated as, not permissible under GST) must not be reduced from turnover as per Financial Statements Annual Return but they should be added back so as to reconcile the amount with Annual Return.

Suggestion: It is suggested to make following modifications in the form GSTR- 9C.

Issue: Part 5E require reporting of credit notes issued after the end of financial year but reflected in the annual return as addition to turnover whereas part 5J requires credit notes accounted for in the audited annual financial statement but not permissible under GST as deduction.

Since the reconciliation is derived from turnover as per financial statements towards annual return, the amount of credit notes not reduced from turnover inFS till March-18 but reduced from turnover Annual Return cannot be added but be reduced from turnover in FS so as to reconcile the amount with turnover Annual Return. The symbol + is creating the confusion. Therefore, the symbol -would clear any confusion.

Also, credit notes accounted for in the audited annual financial statement but are contrary to section 34 (stated as, not permissible under GST) must not be reduced from turnover as per Financial Statements Annual Return but they should be added back so as to reconcile the amount with Annual Return.

Suggestion: It is suggested to make following modifications in the form GSTR- 9C.

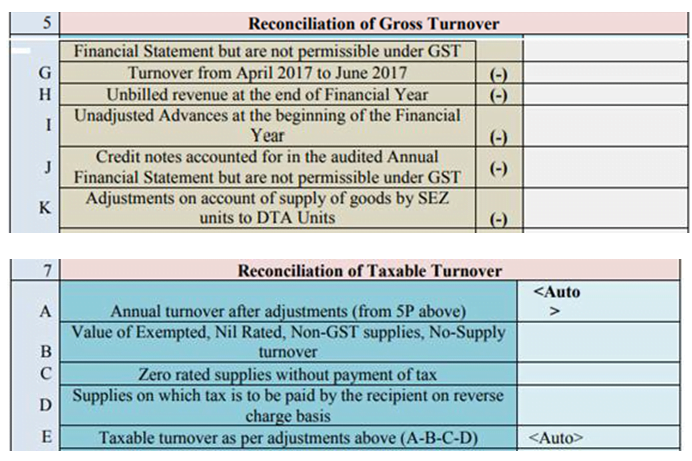

4. Adjustment on account of supply of goods by SEZ to DTA units

Issue: There are certain SEZ units who remove goods to DTA on their own account by filing self-bill of entry, pay corresponding IGST and move the goods under an Invoice with IGST on forward charge basis. Clause 5K, does not appear to clearly state this situation causing confusion.

Suggestion: It is suggested that this requirement to separately report the supplies of SEZ to DTA units in 5K be clarified that the turnovers to be reported in this clause would only be situations where the SEZ units do not file bill of entry in their name and IGST is paid by DTA buyer on reverse charge basis.

5. Expense wise reconciliation

Table 14 of GSTR 9C

Issue: There are certain SEZ units who remove goods to DTA on their own account by filing self-bill of entry, pay corresponding IGST and move the goods under an Invoice with IGST on forward charge basis. Clause 5K, does not appear to clearly state this situation causing confusion.

Suggestion: It is suggested that this requirement to separately report the supplies of SEZ to DTA units in 5K be clarified that the turnovers to be reported in this clause would only be situations where the SEZ units do not file bill of entry in their name and IGST is paid by DTA buyer on reverse charge basis.

5. Expense wise reconciliation

Table 14 of GSTR 9C

Table 4 of GSTR 3B

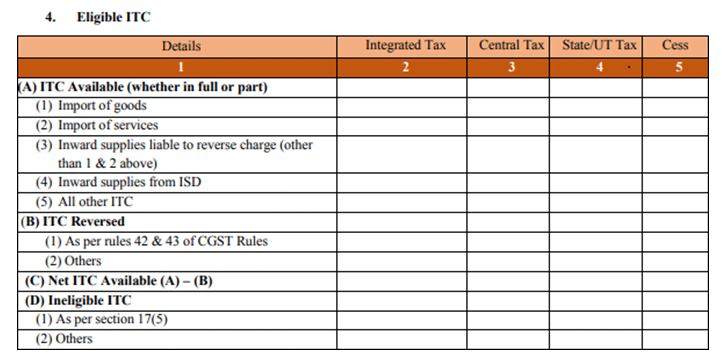

Issue:

1. Table 14 of GSTR-9C requires expense-wise reporting of ITC available and availed whereas it is not feasible for auditors to verify expense wise ITC.

2. Table 14 of GSTR 9C require reporting of total ITC and eligible ITC separately which is also the requirement in form GSTR 3B but some assesses have reported only the net amount of ITC eligible while filing GSTR 3B. In such cases, it will become difficult to identify these figures separately as assessees would have expensed such ineligible ITC in the respective head of expense at the time of booking.

One must appreciate the fact that the relevant Form GSTR 9C was notified after the end of the financial year. Units have not maintained this data to be able to furnish the same accurately.

Issue:

1. Table 14 of GSTR-9C requires expense-wise reporting of ITC available and availed whereas it is not feasible for auditors to verify expense wise ITC.

2. Table 14 of GSTR 9C require reporting of total ITC and eligible ITC separately which is also the requirement in form GSTR 3B but some assesses have reported only the net amount of ITC eligible while filing GSTR 3B. In such cases, it will become difficult to identify these figures separately as assessees would have expensed such ineligible ITC in the respective head of expense at the time of booking.

One must appreciate the fact that the relevant Form GSTR 9C was notified after the end of the financial year. Units have not maintained this data to be able to furnish the same accurately.

Issue: There is no clarity between non-GST supply and no-supply turnover due which it is difficult to bifurcate for e.g. whether high seas supply taken place out of country will be classifiable as no supply turnover or exempted turnover is not clear.

Suggestion: It is suggested to specifically define no-GST supplies or Non-GST turnover for classification of the same.

7. Cash flow statement requirement

Issue: There is a requirement to attach cash flow statement with form GSTR-9C. However, for small scale businesses it is difficult to comply with as they are not required to prepare the same.

Suggestion: It is suggested to make the attachment of cash flow statement optional for small scale businesses.

8. Certification by Auditor

Verification:

I hereby solemnly affirm and declare that the information given herein above is true and correct to the best of my knowledge and belief and nothing has been concealed there from.

Issue: The certification wordings places the entire responsibility of reporting on the Auditor whereas the information is provided by the Auditee (Registered Person) and the Auditor can only verify information to the extent provided and certify the same.

Suggestion: It is suggested that the verification wordings be suitable modified as I hereby solemnly affirm and declare that the information given herein above is true and correct as per the information provided to us by the Registered Person and to the best of my knowledge and belief and nothing has been concealed there from.

9. Pt. V- Auditor's recommendation on additional Liability due to non- reconciliation

Issue:

i. The recommendations by the Auditor in Pt. V are understood to be a note or disclosure. While it is a statement of fact, it need not be an opinion. There can also be situations which could be an opinion of the Auditor whereas the Registered Person may differ. Such situations need not necessarily result in payment of tax. Auditors recommendations may be clarified to be binding or non-binding recommendation that the Registered Person will engage with the revenue authorities for its final determination. Clarity in this regard is much needed.

ii. As Auditors recommendation may not necessarily be in favour of revenue. Such comments in the recommendations will most certainly not lead to payment of tax immediately. In fact, in this Part, the Auditor may be permitted to disclose such situations also. However, it appears that only where taxes are found payable only are being dealt with in this Part. Clarity in this regard is also required.

iii. Payment of tax under auditors recommendation through cash. There may be instances where Registered Persons who have surplus ITC but a genuine error resulting in payment of tax was identified at the time of GST audit. In such situations, the form must provide to enable payment of such dues, to adjust the available credit and pay the dues. Whether the system permits this understanding is to be clarified.

Suggestion: It is suggested that:-

iv. Nature of recommendation by Auditor (binding or non-binding) to be clarified

v. Recommendations to pay or not pay tax be permitted in this Part.

vi. Payment of tax be allowed through ITC as well as cash.

Part B Certificate

Financial Statements comprise of Balance Sheet, Profit and Loss account and Cash flow Statement. These are not prepared for each Registered Person. It may be clarified whether the Financial Statements of the Entity alone is to be annexed or not.

Comments by the Auditor regarding the books of accounts already subject to audit under any other statute may appear to contradict with the findings by that auditor. Such situations are to be avoided. GST Auditor may limit his findings to GST and not travel beyond into the Financial Statements.

Suggestion Revised Part B Provided below :

PART B- CERTIFICATION

I. Certification in cases where the reconciliation statement (FORM GSTR-9C) is drawn up by the person who had conducted the audit:

* I/we have conducted audit of the books of accounts of M/s (Name and address of incorporation of the Person) having GSTIN and registration in the State at .. (Name and Principal Place of Business of Registered Person) comprising of

(a) balance sheet as at

(b) the *profit and loss account/income and expenditure account for the period beginning from ..to ending on .,

(c) the *cash flow statement for the period beginning from ..to ending on , are attached herewith, and

(d) documents declared by the said Act to be part of, or annexed to, the *profit and loss account/income and expenditure account and balance sheet.

2. Based on our audit I/we report that the said Person

*has maintained the books of accounts, records and documents in respect of transactions of the Registered Person as required by the IGST/CGST/<<>>GST Act, 2017 and the rules/notifications made/issued thereunder subject to the following observations / limitations:

1.

2.

3.

3. *I/we further report, in respect of the transactions of the Registered Person, that, -

(A) *I/we have obtained all the information and explanations which, to the best of *my/our knowledge and belief, were necessary *were / were not provided/partially provided to us.

(B) In *my/our opinion, proper books of accounts pertaining to the Registered Person *have/have not been kept by the Person so far as appears from*my/ our examination of the said books of accounts maintained at the principal place of business at and additional place of business within the State..

4. I/we certify that the transactions pertaining to the Registered Person recorded in the said books of accounts *are / are not in agreement with the audited financial statements, that is, balance sheet, the *profit and loss / income and expenditure account and the cash flow statement issued in respect of the Person The documents required to be furnished under section 35 (5) of the CGST Act and Reconciliation Statement required to be furnished under section 44(2) of the CGST Act is annexed herewith in Form No. GSTR-9C.

5. In *my/our opinion and to the best of *my/our information and according to examination of books of accounts pertaining to the Registered Person including other relevant documents and explanations given to *me/us, the particulars given in the said Form No.9C are true and correct subject to the following observations / qualifications, if any:

(a)

(b)

(c)

** (Signature and stamp/Seal of the Auditor)

Place:

Name of the signatory

Membership No

Date:

Full address

* delete whichever is not applicable

II. Certification in cases where the reconciliation statement (FORM GSTR-9C) is drawn up by a person other than the person who had conducted the audit of the accounts:

*I/we report that the audit of the books of accounts M/s. (Name and address of incorporation of the Person) having GSTIN and registration in the State at (Name and Principal Place of Business of Registered Person) was conducted by M/s. .. (full name and address of auditor along with status), bearing membership number in pursuance of the provisions of the Act, and *I/we annex hereto a copy of their audit report along with the audited financial statements of the Person dated comprising of :-

(a) balance sheet as at

(b) the *profit and loss account/income and expenditure account for the period beginning from to ending on ,

(c) the *cash flow statement for the period beginning from ..to ending on , and

(d) documents declared by the said Act to be part of, or annexed to, the *profit and loss account/income and expenditure account and balance sheet.

2. I/we report that the said Person

*has maintained the books of accounts, records and documents in respect of transactions of the Registered Person as required by the IGST/CGST/<<>>GST Act, 2017 and the rules/notifications made/issued thereunder subject to the following observations / limitations:

1.

2.

3.

3. The documents required to be furnished under section 35 (5) of the CGST Act and Reconciliation Statement required to be furnished under section 44(2) of the CGST Act is annexed herewith in Form No.GSTR-9C.

4. In *my/our opinion and to the best of *my/our information and according to examination of books of accounts pertaining to the Registered Person including other relevant documents and explanations given to *me/us, the particulars given in the said Form No.9C are true and correct subject to the following observations / qualifications, if any:

(a) ..

(b) ..

(c) ..

** (Signature and stamp/Seal of the Auditor)

Place:

Name of the signatory

Membership No

Date:

Full address .

* delete whichever is not applicable

10. Requirement of Audit in case of exempted outward supplies only

In terms of Rule 80(3) of the CGST Rules every registered person whose aggregate turnover during a financial year exceeds two crore rupees shall get his accounts audited as specified under sub-section (5) of Section 35 of the Act.

Issue : A taxpayer has obtained registration due to application of provision of Section 24 of CGST Act, 2017 read with Section 9(3), however dealing in exclusively exempted supply only.

Suggestion : We understand that in the aforesaid scenario, Audit would be required as aggregate turnover includes exempt supply, However clarificatory circular may be issued in this regard.

| S. No. | Topic(s) | Suggestion (s) |

| 1. | Calculation of Turnover of Rs. 2 Crore for the applicability of GST Audit | Limit of Turnover of Rs. 2 Crore would be calculated from July onwards for the FY 2017-18 or the Financial year 2017-18 would be considered for the same. Therefore, It is suggested to provide suitable clarification in this regard. |

| 2. | Turnover of multi GSTN units under same PAN | Requirements at the beginning of the financial year in part 5B and 5I seems to lead to some confusion. Therefore it is suggested to substitute it with words as on 30th June, 2017 |

| 3. | Credit notes issued after the end of financial year | Credit notes accounted for in the audited annual financial statement must not be reduced from turnover as per Financial Statements but they should be added back so as to reconcile the amount with Annual Return. |

| 4. | Adjustment on account of supply of goods by SEZ to DTA units | It is suggested that this requirement to separately report the supplies of SEZ to DTA units in 5K be clarified that the turnovers to be reported in this clause would only be situations where the SEZ units do not file bill of entry in their name and IGST is paid by DTA buyer on reverse charge basis. |

| 5. | Expense wise reconciliation | Table 14 of GSTR-9C requires expense-wise reporting of ITC available and availed whereas it is not feasible for auditors to verify expense wise ITC. Therefore, It is suggested to give relaxation in furnishing such breakup, to the extent maintained. |

| 6. | Classification of turnover between Nil, exempted,non-GST and no-supplyturnover. | There is no clarity between non-GST supply and no-supply turnover due which it is difficult to bifurcate for e.g. whether highseas supply taken place out of country will be classifiable as no supply turnover or exempted turnover is not clear. Therefore, it is suggested to specifically define no-GST supplies or Non-GST turnover for classification of the same. |

| 7. | Cash flow statement requirement | There is a requirement to attach cash flow statement with form GSTR-9C. However, for small scale businesses it is difficult to comply with as they are not required to prepare the same. Therefore, It is suggested to make the attachment of cash flow statement optional for small scale businesses. |

| 8. | Certification by Auditor | The certification wordings places the entire responsibility of reporting on the Auditor whereas the information is provided by the Auditee (Registered Person) and the Auditor can only verify information to the extent provided and certify the same. Therefore, It is suggested that the verification wordings be suitable modified as : I hereby solemnly affirm and declare that the information given herein above is true and correct as per the information provided to us by the Registered Person and to the best of my knowledge and belief and nothing has been concealed there from. |

| 9. | Pt. V- Auditor's recommendation on additional Liability due to non-reconciliation | It is suggested that:- i. Nature of recommendation by Auditor (binding or non-binding) to be clarified ii. Recommendations to pay or not pay tax be permitted in this Part. iii. Payment of tax be allowed through ITC as well as cash. |

| 10. | Requirement of Audit incase of exempted outward supplies only | Where a taxpayer has obtained registrationdue to application of provision of Section 24 of CGST Act, 2017 read with Section 9(3), in this case, Audit would be required as aggregate turnover includes exempt supply, However clarification circular may be issued in this regard. |

Issue:

1. Part 5B Unbilled revenue at the beginning of Financial year seems to lead to some confusion.

2. Part 5I Unadjusted advances at the beginning of the financial year seems to lead to some confusion.

3. This confusion is on account of the fact that the GST regime was effective from July 1, 2017. The question that arises is, when the form states beginning of financial year, whether information as at April 1, 2017 should be considered or as at July 1, 2017. It is clear that in respect of GST reconciliation, information must be reckoned from its inception and not earlier. For this reason, it is advisable to clear this confusion by suitably stating with reference to the date of inception of GST, that is, as at July 1, 2017.

Suggestion:

It is suggested to substitute the words at the beginning of the financial year in part 5B and 5I with words as on 30th June, 2017

3. Credit notes issued after the end of financial year

Issue: Part 5E require reporting of credit notes issued after the end of financial year but reflected in the annual return as addition to turnover whereas part 5J requires credit notes accounted for in the audited annual financial statement but not permissible under GST as deduction.

Since the reconciliation is derived from turnover as per financial statements towards annual return, the amount of credit notes not reduced from turnover inFS till March-18 but reduced from turnover Annual Return cannot be added but be reduced from turnover in FS so as to reconcile the amount with turnover Annual Return. The symbol + is creating the confusion. Therefore, the symbol -would clear any confusion.

Also, credit notes accounted for in the audited annual financial statement but are contrary to section 34 (stated as, not permissible under GST) must not be reduced from turnover as per Financial Statements Annual Return but they should be added back so as to reconcile the amount with Annual Return.

Suggestion: It is suggested to make following modifications in the form GSTR- 9C.

| E | Credit notes accounted for in the audited annual financial statement but are not permissible under GST | (+) |

| J | Credit notes issued after the end of the financial year but reflected in the annual return | (-) |

Issue: There are certain SEZ units who remove goods to DTA on their own account by filing self-bill of entry, pay corresponding IGST and move the goods under an Invoice with IGST on forward charge basis. Clause 5K, does not appear to clearly state this situation causing confusion.

Suggestion: It is suggested that this requirement to separately report the supplies of SEZ to DTA units in 5K be clarified that the turnovers to be reported in this clause would only be situations where the SEZ units do not file bill of entry in their name and IGST is paid by DTA buyer on reverse charge basis.

5. Expense wise reconciliation

Table 14 of GSTR 9C

| 14 | Reconciliation of ITC declared in Annual Return (GSTR9) with ITC availed on expenses as per audited Annual Financial Statement or books of account | |||

| Description | Value | Amount of Total ITC | Amount of eligible ITC availed | |

| 1 | 2 | 3 | 4 | |

| A | Purchases | |||

| B | Freight / Carriage | |||

| C | Power and Fuel | |||

| D | Imported goods (Including received from SEZs) | |||

| E | Rent and Insurance | |||

| F | Goods lost, stolen, destroyed, written off or disposed of by way of gift or free samples | |||

| G | Royalties | |||

Issue:

1. Table 14 of GSTR-9C requires expense-wise reporting of ITC available and availed whereas it is not feasible for auditors to verify expense wise ITC.

2. Table 14 of GSTR 9C require reporting of total ITC and eligible ITC separately which is also the requirement in form GSTR 3B but some assesses have reported only the net amount of ITC eligible while filing GSTR 3B. In such cases, it will become difficult to identify these figures separately as assessees would have expensed such ineligible ITC in the respective head of expense at the time of booking.

One must appreciate the fact that the relevant Form GSTR 9C was notified after the end of the financial year. Units have not maintained this data to be able to furnish the same accurately.

Suggestion:

It is suggested to give relaxation in furnishing such breakup, to the extent maintained. 6. Classification of turnover between Nil, exempted, non-GST and no-supply turnover.| 7 | Reconciliation of Taxable Turnover | |

| 7A | Annual turnover after adjustments (from 5P above) | <Auto> |

| 7B | Value of Exempted, Nil Rated, Non-GST supplies, No-Supply Turnover | |

About Author

CA Deepak Gupta

Co Founder

CA Deepak Gupta,is Co-founder of Studycafe. He is Microsoft Office Specialist and Corporate Trainer of AI Tools, Microsoft Excel.

He is Finance Influencer having more than 250K followers on Social Media. CA Deepak Gupta, is Having more than 14 plus years of experience, and he has Worked with best brands Like, Hero, Wipro, Ericsson before Starting Studycafe. He has Trained more than 20000 Persons in Microsoft Excel, PowerPoint, Power BI, Google Sheet, Google Forms and Other Tools.

CA Deepak Gupta,is Co-founder of Studycafe. He is Microsoft Office Specialist and Corporate Trainer of AI Tools, Microsoft Excel.

He is Finance Influencer having more than 250K followers on Social Media. CA Deepak Gupta, is Having more than 14 plus years of experience, and he has Worked with best brands Like, Hero, Wipro, Ericsson before Starting Studycafe. He has Trained more than 20000 Persons in Microsoft Excel, PowerPoint, Power BI, Google Sheet, Google Forms and Other Tools.

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 3423

3423My Recent Articles

- UltraTech Cement slapped with Rs. 808.78 Cr Income Tax Demand

- GST: High Court upheld constitutional validity of Section 16(2)(c), asks government to address ITC issues of genuine purchasers

- Old vs New Tax Regime for Tax Year 2026-27

- High court criticizes Income Tax Department for not releasing ITR Utilities despite 11 years of directions

- Fino Payments Bank CEO Rishi Gupta Gets Bail in GST Case, Bank Clarifies No Direct Link

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.