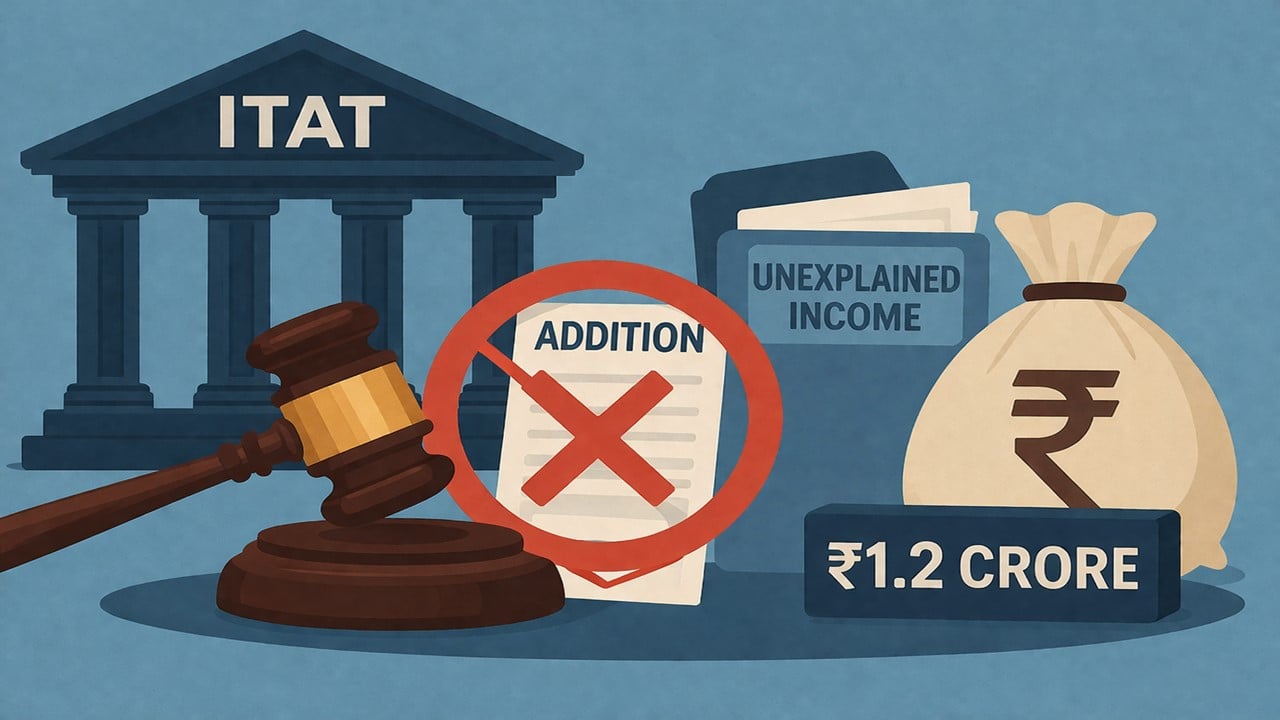

ITAT Delhi Quashes Rs 1.2 Crore Addition Due to Delayed Tax Notice and Lack of Jurisdiction:

The Tribunal found that the notice under Section 143(2) was issued after the prescribed time limit and also by an assessing officer who did not have jurisdiction over the assessee.

ITAT Quashes Rs 1.2 Crore Addition Towards Unexplained Income

Premium

ITAT Delhi Quashes Rs 1.2 Crore Addition Due to Delayed Tax Notice and Lack of Jurisdiction

The Tribunal found that the notice under Section 143(2) was issued after the prescribed time limit and also by an assessing officer who did not have jurisdiction over the assessee.

Also Read

ITAT Sets Aside Ex-Parte Income Tax Assessment for Breach of Natural JusticeITAT Rules Late Filing of Form 67 Cannot Defeat Foreign Tax Credit Claim Under Section 90 Income Tax Dept Releases ITR-6 Excel Utility for AY 2026-27 on E-Filing Portal; Check Step-by-Step Download GuideITAT Says Appeal Cannot Be Dismissed Without Examining Merits, Orders Fresh Decision

About Author

Nidhi

Content Writer

Nidhi is a skilled content writer specializing in personal finance. She creates clear, engaging articles on mutual funds, investments, insurance, and wealth-building strategies. With a passion for simplifying complex financial topics, Nidhi helps readers make informed money decisions with confidence. She can be reached at [email protected]

Nidhi is a skilled content writer specializing in personal finance. She creates clear, engaging articles on mutual funds, investments, insurance, and wealth-building strategies. With a passion for simplifying complex financial topics, Nidhi helps readers make informed money decisions with confidence. She can be reached at [email protected]

Studycafe

Studycafe New Delhi, Delhi, India

New Delhi, Delhi, India 1832

1832My Recent Articles

- Karnataka High Court Gives Another Chance in GST Matter Due to Lack of Hearing

- Delay Should Be Condoned if Explanation is Unrefuted: ITAT

- Non-Service of Income Tax Notice, Ill health of taxpayer, ITAT condones Appeal filing delay

- Books of Accounts Cannot be Rejected Without Any Specific Defect: ITAT Kolkata

- Karnataka High Court Sends ITC Matter Back to GST Authorities for Reconsideration

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

Recent Posts

All Posts