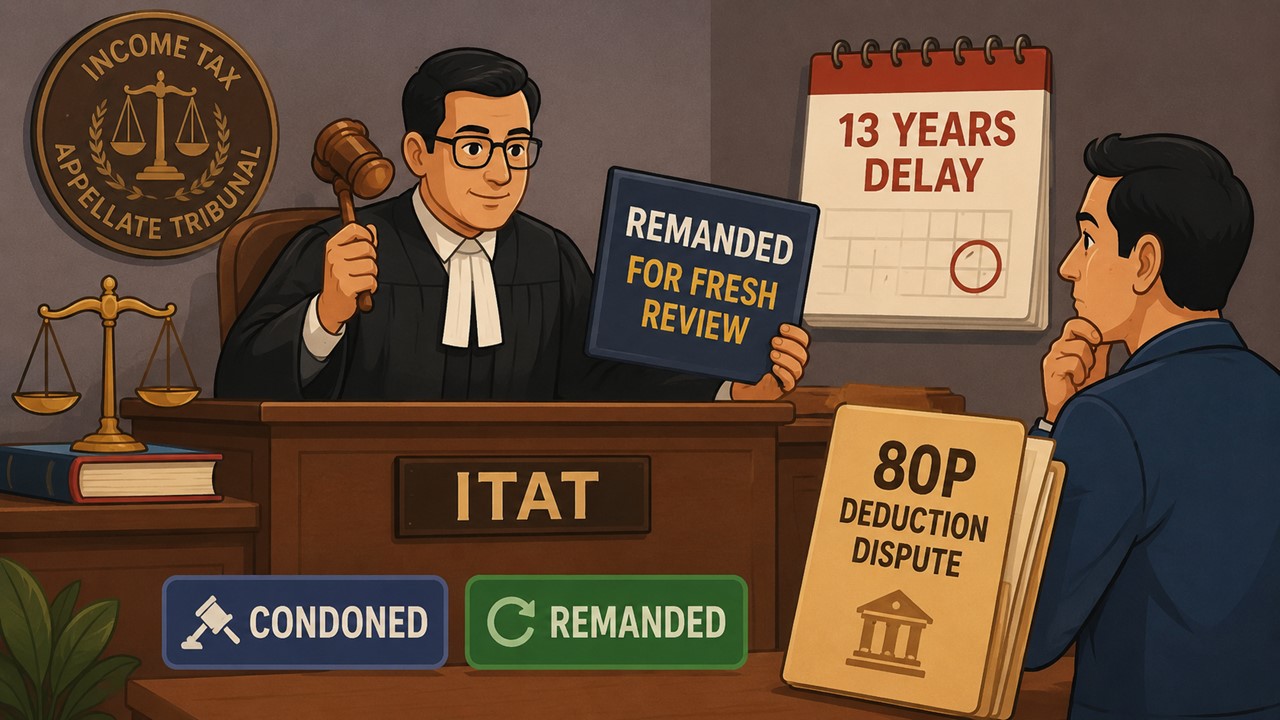

ITAT Condones 13-Year Delay, Remands Section 80P Deduction Dispute for Fresh Review:

ITAT condones a 13-year delay and remands co-operative housing society's Section 80P deduction claim to AO for fresh examination.

ITAT Restores Section 80P Deduction Dispute

Table of Contents

ITAT Condones 13-Year Delay, Remands Section 80P Deduction Dispute for Fresh Review

The Mumbai Bench of the Income Tax Appellate Tribunal (ITAT) has provided relief to Bakhtawar Co-operative Housing Society Ltd in a long-pending tax dispute related to a deduction under Section 80P of the Income Tax Act.

Background of the case

The Central Processing Centre (CPC), Bengaluru, had disallowed the society's claim of deduction of Rs.13,77,502 under Section 80P(2)(d) while processing its return under Section 143(1). As a result, the society's taxable income increased from Rs. 1,03,210 to Rs. 14,80,720. The society challenged this adjustment before the CIT(A). However, the appeal was dismissed because it was filed more than 13 years after the original assessment order, making it time-barred. Before the ITAT, the society explained the reasons for the delay. It said that its part-time accountant was of the view that the issue could be addressed directly with the Assessing Officer through rectification proceedings. Earlier, its tax consultant had also advised the society that an appeal was not required. Later, due to a change in the managing committee, staff turnover and disruption caused by the COVID-19 pandemic, the issue was left unattended for some years. The Tribunal found the explanation satisfactory and observed that there was no evidence of any deliberate delay or mala fide intention on the part of the society. Hence, in the interest of justice, the ITAT condoned the delay and admitted the appeal. While dealing with merits, the Tribunal observed that similar issues relating to co-operative housing societies had been decided earlier in favour of remanding the matter for fresh examination. The Bench relied on its recent decision in the case of Torino Co-operative Housing Society Ltd., wherein a similar delay was condoned, and the matter was remanded for reconsideration. Following the same approach, the ITAT set aside the orders of the lower authorities and remanded the matter to the Assessing Officer for fresh adjudication. The AO has been directed to reconsider the claim of the society for deduction under section 80P(2)(d) after verification of the relevant facts. The Tribunal has also directed to give a reasonable opportunity of hearing to the society in the fresh proceedings. At the same time, it advised the society to cooperate with the tax authorities fully. As a result, the appeal was allowed for statistical purposes.

About Author

Vanshika verma

Content Writer

Vanshika Verma is a Content Writer with 1+ year of experience at Studycafe.in. A B.Com graduate from Delhi University, She writes articles on Finance, Tax, ICAI, GST, and the latest financial news, with a focus on making complex topics easy for readers and professionals.

Vanshika Verma is a Content Writer with 1+ year of experience at Studycafe.in. A B.Com graduate from Delhi University, She writes articles on Finance, Tax, ICAI, GST, and the latest financial news, with a focus on making complex topics easy for readers and professionals.

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 1566

1566My Recent Articles

- ITAT: Section 271D Penalty Cannot Survive Without AO's Recorded SatisfactionPremium

- ITAT Remands Section 69C Addition Case, Orders Fresh Opportunity to TaxpayerPremium

- CBDT Issues Notification for Exemption from TDS on Certain Payments to IFSC Units under Income-tax Act, 2025

- ITAT Gives Taxpayer Second Chance, Quashes Ex-Parte Appellate OrderPremium

- ITAT Sets Aside Ex-Parte CIT(A) Order in Rs 42 Lakh Property Sale Tax CasePremium

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

Recent Posts

All Posts