ITAT Grants Major Relief to Small Trader, Limits Tax Liability Using 8% Presumptive Income Rule:

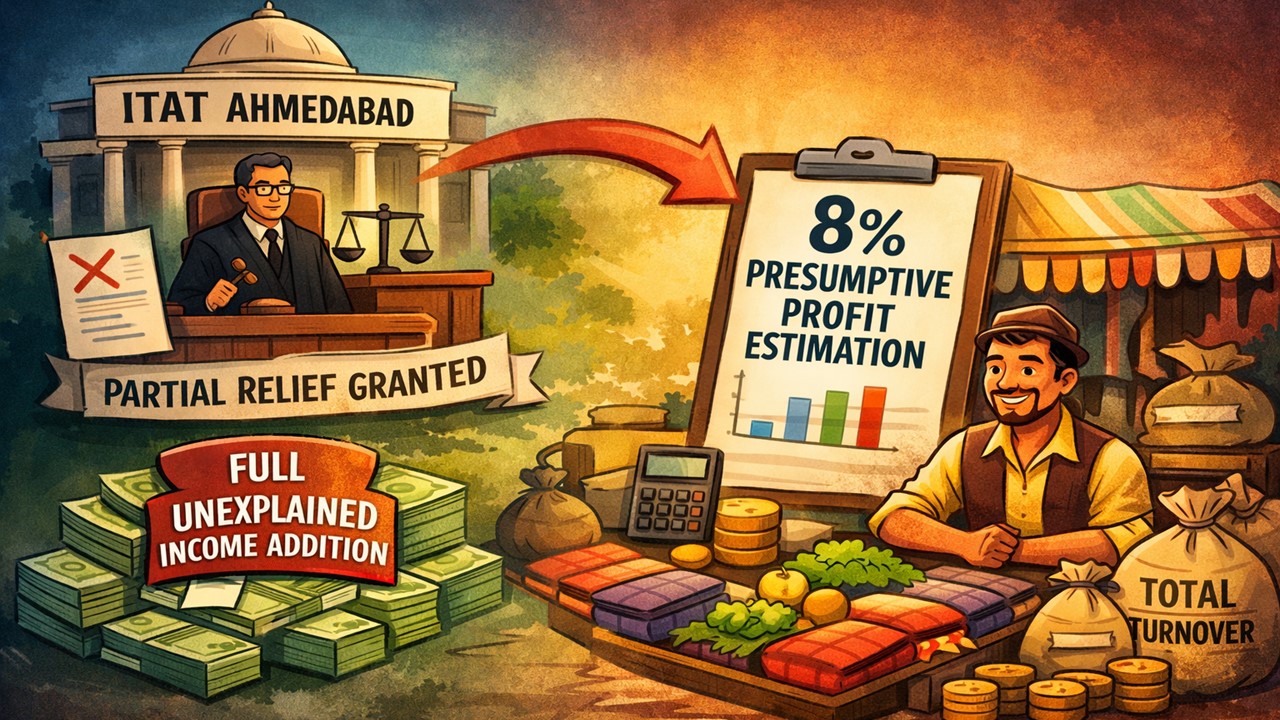

ITAT Ahmedabad granted partial relief to a small trader by replacing a full unexplained income addition with an 8% presumptive profit estimation on total turnover.

ITAT Rejects Full Addition Under Section 69A

ITAT Grants Major Relief to Small Trader, Limits Tax Liability Using 8% Presumptive Income Rule

The ITAT Ahmedabad has announced its final decision on an appeal filed by Rajesh Ramkishan Gupta against the Income Tax Department, challenging an order dated August 08, 2025, passed by the CIT(A), NFAC Delhi. The case belongs to the Assessment Year 2020-21. The impugned order had upheld the additions made by the Assessing Officer (AO) on the grounds of insufficient explanation.

In the present case, the Assessing Officer (AO) had reopened the case of the assessee on the ground that certain documents and materials confiscated during the search conducted in the case of Ambica Fireworks Group of Ashish Jayantilal Khajanji under Section 132 were found linked to the assessee. The AO noted that the assessee was a purchaser from Ambica and had made a cash transaction amounting to Rs 426,100 during the year in consideration.

Considering the same, the AO treated the amount as unexplained income and made an addition of the same under Section 69A. The assessee argued that, being a small retainer operating a seasonal business of firecrackers and kites, he had filed his income tax return (ITR) under Section 44AD and had also furnished all relevant documents during the proceedings. The assessee further claimed that he just could not respond to one of the notices due to a lack of technical knowledge and awareness of online communication. Considering the only non-compliance of not responding to the show cause notice (SCN), the AO made the impugned addition.

When the tribunal analysed the facts of the case, it noted that the assessee was a small trader with a total turnover of Rs 1,120,000. Considering fairness, legal principles, and practical realities, the Tribunal held that instead of treating the entire amount as unexplained income, it would be reasonable to estimate profit. The Tribunal directed the tax authorities to apply an 8% net profit rate on the total turnover, in line with presumptive taxation principles. Consequently, the tribunal partly allowed the appeal by reducing the tax burden.

About Author

Saloni Kumari

Content Writer

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 2515

2515My Recent Articles

- Missed July 31 ITR Deadline? Here’s What Taxpayers Need to Know Now

- Confused Between Belated, Revised and Updated Return? Here's Clarification on What You Should File

- Missed the July 31 ITR Deadline? File Your Belated Return to Avoid Penalties, Refund Loss, and Tax Notices

- Why Do You Need to File an ITR? 6 Key Reasons Every Taxpayer Must Know Before July 31 Deadline

- SC Directs IGP Kiran S. to Head Reconstituted SIT, Directs CA Appointment in Ayodhya Ram Temple Donation Theft Probe

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

Recent Posts

All Posts