ITAT Remands Section 270A Penalty Appeal, Holds CIT(A) Must Decide Matter on Merits Instead of Dismissing for Non-Prosecution:

The Income Tax Appellate Tribunal (ITAT) Chennai has restored penalty proceedings to the CIT(A) after observing that the appeal had been dismissed solely on account of non-participation by the assessee.

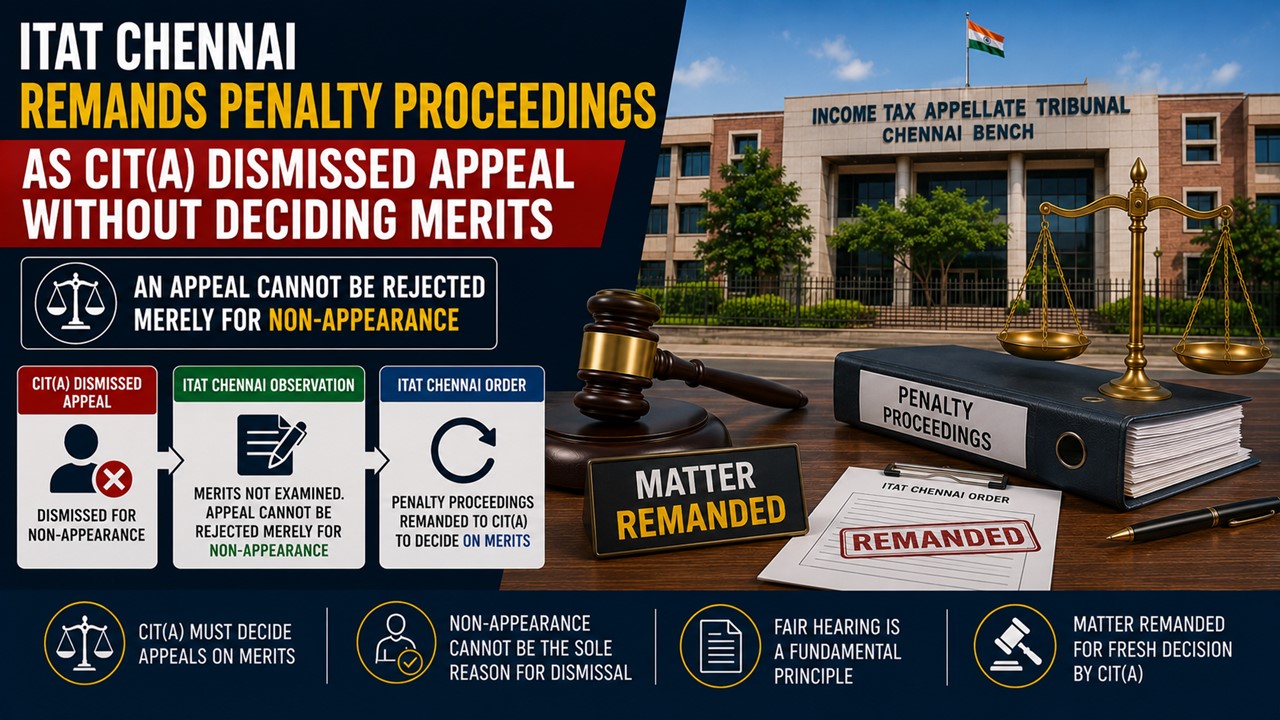

An Appeal Cannot be Rejected Merely for Non-Appearance

ITAT Remands Section 270A Penalty Appeal, Holds CIT(A) Must Decide Matter on Merits Instead of Dismissing for Non-Prosecution

The Income Tax Appellate Tribunal (ITAT) Chennai held that an appellate authority cannot dismiss an appeal merely on account of the assessee's nonappearance without adjudicating the issues raised on merits.

Ceeyes Engineering Industries Private Limited had not filed its return of income for assessment year 2018-19 under Section 139(1) of the Income Tax Act, 1961. On the basis of information regarding financial transactions amounting to Rs 1.57 crore, the AO reopened the assessment under Section 147 and issued a notice under Section 148. In response to the notice, the assessee filed its return declaring total income of Rs 92.90 lakh. After examination of the records, the AO completed the assessment without making any addition and accepted the returned income.

However, under Section 270A, penalty proceedings were initiated because income had been disclosed only in response to a notice issued under Section 148 and a penalty of Rs 11.96 lakh was imposed for underreporting of income. Aggrieved by the penalty through an order dated 18 September 2024, the assessee preferred an appeal before the CIT(A).

The CIT(A) granted seven opportunities of hearing to the assessee but still no response was furnished so, the appeal was dismissed and the penalty imposed by the AO was confirmed. Before the Tribunal, the assessee contended that the appellate authority had dismissed the appeal merely for non-filing of detailed submissions and had not adjudicated the issues raised in the appeal.

The Tribunal observed that although the assessee had not participated in the appellate proceedings, the grounds of appeal and relevant details had already been placed before the CIT(A). The appellate authority had dismissed the appeal without examining the issues on their merits. Considering the principles of natural justice and in the interest of justice, the Bench set aside the orders of the lower authorities relating to penalty proceedings and remitted the matter back to the file of the CIT(A).

The Tribunal, while allowing the appeal for statistical purposes, directed the CIT(A) to consider the grounds raised by the assessee and give a reasonable opportunity to be heard before passing a reasoned order.

About Author

Saima

Content Writer

Saima is a Law graduate with a passion for research and content writing. She writes for Finance, Taxation and Legal Updates at Studycafe.in, simplifying complex legal decisions by the ITAT, High Court, AAR and GSTAT into uncomplicated and clear explanations.

Saima is a Law graduate with a passion for research and content writing. She writes for Finance, Taxation and Legal Updates at Studycafe.in, simplifying complex legal decisions by the ITAT, High Court, AAR and GSTAT into uncomplicated and clear explanations.

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 237

237My Recent Articles

- ITAT Quashes Reassessment Notice Issued Beyond Surviving Limitation Period Prescribed Under TOLAPremium

- ITAT Holds Charitable Trust Cannot Be Assessed as Association of PersonsPremium

- ITAT Restricts Section 69A Addition to Rs 3 Lakh Premium

- ITAT Rules No PE in India if Services are Rendered Entirely from Outside IndiaPremium

- Supreme Court Upholds Constitutionality of Section 16(2)(c) CGST Act Premium

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts