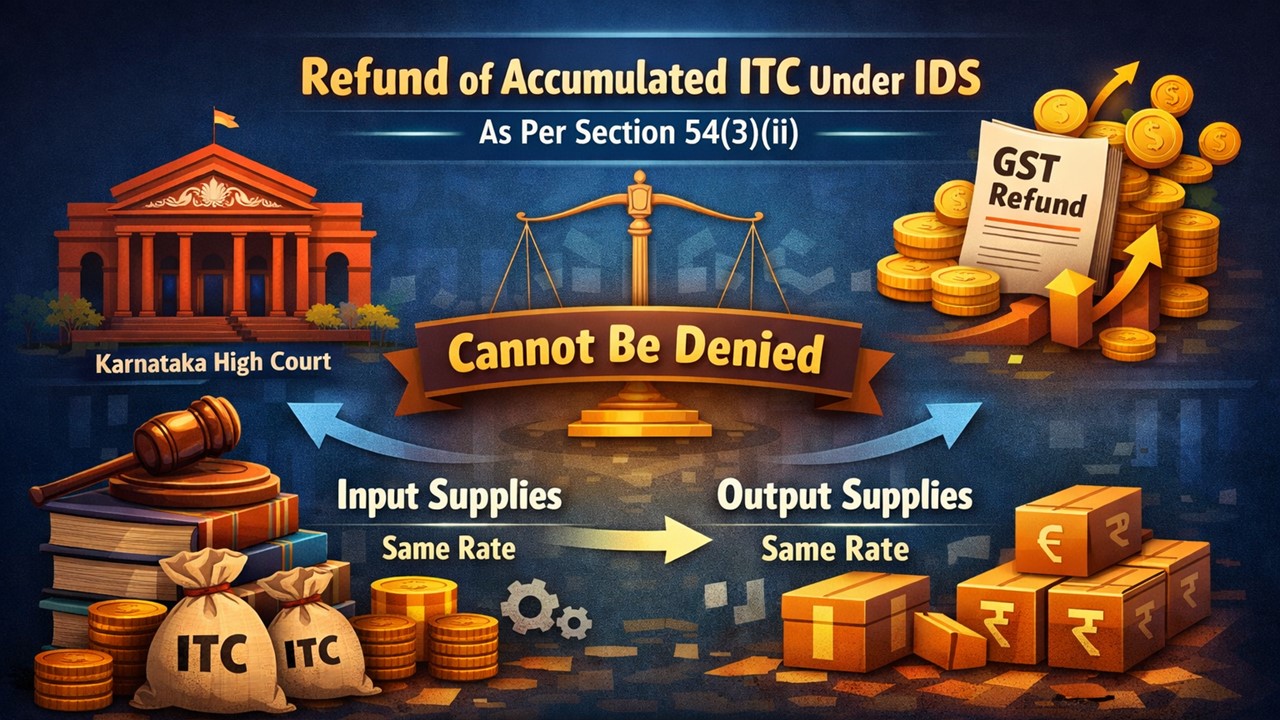

ITC Refund under IDS Cannot Be Denied Merely Because Input Output Goods are identical:

The HC holds that the refund of accumulated ITC under IDS as per Section 54(3)(ii) cannot be denied simply because the input and output supplies are identical or taxed at the same rate.

HC Clarifies Scope of Section 54(3)(ii) under GST

ITC Refund under IDS Cannot Be Denied Merely Because Input Output Goods are identical

The Karnataka High Court holds that the refund of accumulated ITC under IDS as per Section 54(3)(ii) cannot be denied simply because the input and output supplies are identical or taxed at the same rate. The court rules that the petitioner is entitled to a refund on the accumulated ITC.

The Karnataka High Court has delivered a significant judgement dated December 12, 2025, in a writ petition filed by the South Indian Oil Corporation against the Assistant Commissioner of Central Tax Division 1 (Income Tax Authorities), challenging an order dated May 23, 2023, passed by the tax authorities. The case was heard by the Honourable Justice S. R. Krishna Kumar. The present case is related to the refund of accumulated Input Tax Credit (ITC) under the Goods and Services Tax (GST) law.

The petitioner, South Indian Oil Corporation, is engaged in procuring various edible oils. The petitioner purchases these oils at a 5% GST rate, falling under HSN Code 15. Thereafter, they are packed into smaller containers of net weights of 250 ml, 500 ml, 1 litre, and 5 litres for sale to businesses and customers. During this process, the company used several inputs and services that attracted higher GST rates than the 5% charged on the final packaged edible oil. This created an "inverted duty structure", meaning the tax paid on inputs was higher than the tax on output supplies. As a result, the company accumulated unutilised ITC and applied for a refund under Section 54(3)(ii) of the CGST Act.

However, tax authorities rejected the refund claims, arguing that the input and output goods were the same and, therefore, the refund was not allowed. When the company filed a writ petition before the High Court, challenging the aforesaid rejection, the court noted that Section 54(3)(ii) of the CGST Act allows a refund of unutilised ITC when the tax rate on inputs is higher than the tax rate on output supplies. The court held that the law does not prohibit refunds simply because the input and output goods are the same. It also noted that a later government circular in 2022 removed the restriction that denied refunds in such cases, and this clarification should apply retrospectively.

The court cited earlier high court judgements based on identical circumstances; among these judgements was the case of Indian Oil Corporation Limited, heard by this court. All these cases favoured the assessee. The court ruled, "In view of the aforesaid facts and circumstances and the judgement of this Court in Mrs Indian Oil Corporation's case supra, the impugned orders deserve to be set aside, and the refund claim of the petitioner deserves to be allowed."

Hence, the court concluded that the petitioner was entitled to the refund. The court set aside the impugned orders rejecting the refund claim made by the petitioner. Additionally, the tax authorities are directed to refund the amount due to the petitioner together with applicable interest in accordance with law within a period of three months from the date of receiving the present order.

About Author

Saloni Kumari

Content Writer

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 2537

2537My Recent Articles

- High Court Pulls Up ITAT Over Repeated Non-Compliance With Rule 34; Directs to Pronounce Orders Within 90 DaysPremium

- CBI Brings Back Vishakha Rathod from UAE in Rs 88 Crore Investment Scam; Husband Sent to 10-Day Police Custody

- Income Tax Dept Releases ITR-6 Excel Utility for AY 2026-27 on E-Filing Portal; Check Step-by-Step Download Guide

- Everest Industries Receives Rs 3.17 Crore GST Show Cause Notice; Company to Contest Allegations

- Corporate Laws (Amendment) Bill, 2026 Proposes Major Changes in Company Compliance Rules

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts