ITR Processing: Everything You Need to Know About Section 143(1) Intimation:

A simple guide to understanding Section 143(1) intimation, including tax refunds, demands, errors, and the steps taxpayers should take after receiving it.

Here’s What You Need To Do After Receiving a Section 143(1) Notice

ITR Processing: Everything You Need to Know About Section 143(1) Intimation

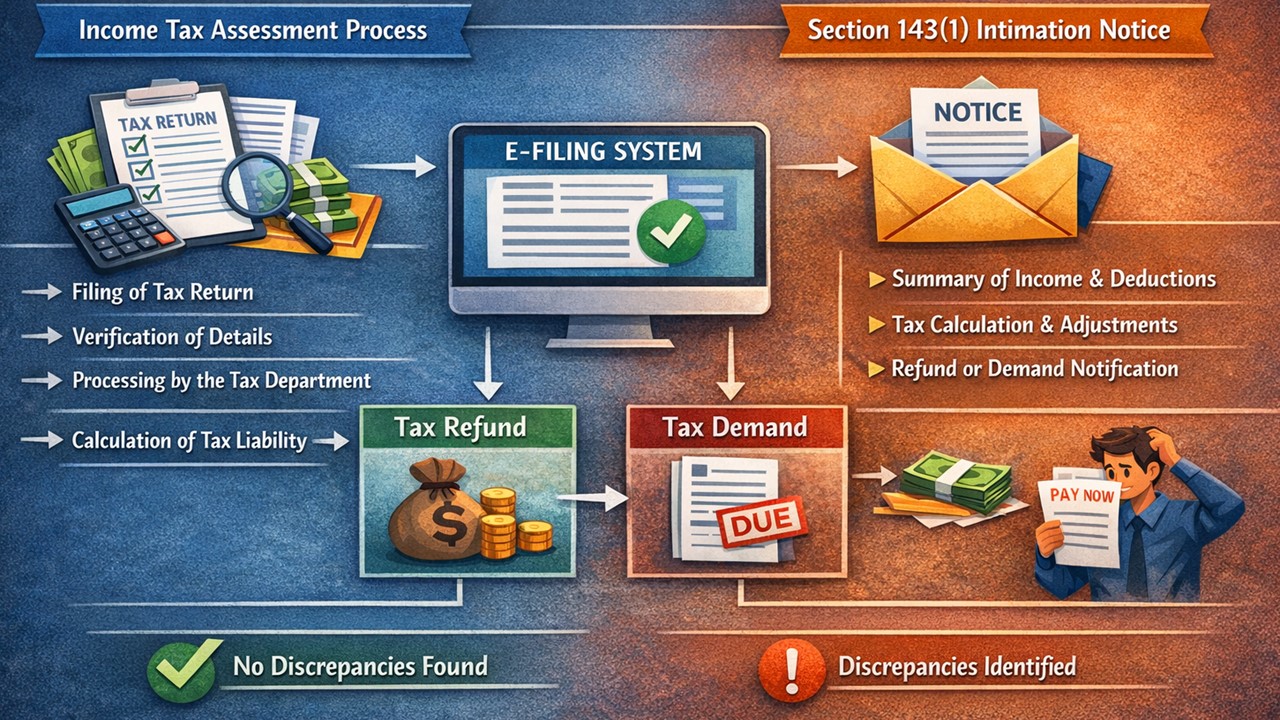

The process of analysing an income tax return (ITR) by the Income Tax Department, after its filing by a taxpayer, is called assessment. This process is completely computer-based and is done through the Central Processing Centre (CPC). In this process, any kind of calculation error in the return, difference in tax payment or other discrepancies is checked. If any discrepancy is found, an intimation is sent to the concerned taxpayer under section 143(1).

When is a Section 143(1) Intimation Sent?

- Every taxpayer can receive a Section 143(1) intimation after the return is processed. If excess tax has been deposited, then a refund is issued if it exceeds Rs 100 and all bank/account details are valid. If the tax is less deposited, then a challan is issued for the demand amount and payment. Sometimes this is simply confirmation that the return has been found to be correct.

- This notice contains many important pieces of information, like the date of notice, PAN number, assessment year, acknowledgement number of ITR and document identification number. Along with this, a comparison of income, deductions and tax calculations made by the taxpayer and the department is also shown.

- In this process, mathematical mistakes made in the returns are checked. Apart from this, wrong claims, like showing income at one place and not showing it at another place, are also checked. The process also includes incorrect set-off of losses from previous years and non-inclusion of expenses shown in the audit report in the returns.

- The Income Tax Department sends this intimation within nine months from the end of the financial year in which the return is filed. For example, if the return for FY 2023-24 is filed in July 2024, the notice can come anytime upto December 31, 2025. If no notice is received within this period, it means the return has been accepted without any changes.

- This notice is password-protected. Your PAN (in lowercase) and your DOB (in DDMMYYYY format, with no spaces) are the password. For example, if PAN is ABCDE1234E and the date of birth is 01 January 2000, then the password will be abcde1234e01012000.

- After receiving the notice, first of all, ensure that the information given in it, like name, PAN, assessment year and ITR acknowledgement number, is correct. If any mistake is made while filing the return, it can be corrected through a revised return. If you do not agree with the changes made by the department, an application for rectification can be made under section 154.

- If tax is demanded in the notice and you agree to it, you will have to pay. While making payment, it is necessary to select the option "Tax on Regular Assessment (400)" in the challan. If the issue is not resolved, a complaint can be filed on the e-filing portal, or the Assessing Officer can be contacted. If the notice contains a tax demand, it is mandatory for the taxpayer to respond within 30 days, whether he agrees or disagrees with it. Responding at the right time can avoid further legal action.

About Author

Kashish Bhardwaj

Content Writer

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 176

176My Recent Articles

- Supreme Court Judge Strength to Increase from 33 to 37 for Faster Justice

- Builder Cleared of Profiteering Charges After Passing Excess ITC Benefit to Homebuyers: GSTAT

- Jubilant Ingrevia to Challenge Rs 2.03 Crore GST Demand Before GSTAT

- Rs 70 Crore Claim Row: Ex-CFO Gobind Jain Moves Bombay High Court Against IndusInd Bank Over Alleged Wrongful Dismissal

- Dream Sports Launches Dream Street: AI-Powered Entry into India’s Retail Broking Market

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

Recent Posts

All Posts