Kerala Flood Cess Frequently Asked Questions

Kerala Flood Cess Frequently Asked Questions or FAQ's on Kerala Flood Cess We all are well aware of massive floods that hit Kerala in August

Table of Contents

Kerala Flood Cess Frequently Asked Questions or FAQ's on Kerala Flood Cess

We all are well aware of massive floods that hit Kerala in August 2018. In wake of those floods and to re-establish lost glory of State of Kerala, Government has introduced applicability of Kerala Flood Cess effective from 1st July 2019. Through these FAQ's, let's discuss various points related to Applicability of Kerala Flood Cess Rules 2019 in simplified manner.

Kerala Flood Cess Frequently Asked Questions

1. What is the Sole Purpose of Applicability of Kerala Flood Cess

A Cess is a special Type of Tax, which is made applicable for serving a specific purpose. For Example, Swatch Bharat Cess was made applicable to serving purpose of cleaning India, Education Cess was made applicable for Promoting Literacy, Similarly Kerala Flood Cess is being made applicable of re-establishing the State of Kerala.

2. What is the due date of Applicability of Kerala Flood Cess

Kerala Flood Cess would be applicable with effect from 1st July, 2019.

3. Who is required to pay Kerala Flood Cess

Kerala Flood Cess shall be levied on intra-state supplies of goods or services or both made by a taxable person to an unregistered person.

Provided that no such cess shall be leviable on-

(i) supplies made by a taxable person who has decided to opt for

composition levy

(ii) supplies of exempted goods and services or both

(iii) supplies of goods and services or both made by a registered taxable

person to another registered taxable person.

For Example if Supply is as follows:

Mr A Supplies Goods to Mr B. Both are register supplier in state of Kerala. In this case this cess would not be applicable.

But now Mr B supplies the goods to Mr C who is a consumer or unregistered supplier, In this case Kerala Cess would be applicable.

4. What is rate of Kerala Flood cess and What are the supplies on which this cess is applicable

|

SI. No. |

Description of goods or services or both |

Rate of cess |

|

1. |

Supplies of goods for which tax rate is fixed at 1.5 (Gold & Silver) |

0.25% |

|

2. |

Supplies of services for which tax rate is fixed at 2.5 |

1% |

|

3. |

Supplies of goods and services or both for which tax rate is fixed at 6%, 9% and 14% |

1% |

5. How to Calculate Kerala Flood cess

Calculation of Kerala Flood Cess has been explained with the help of Below mentioned example:

Mr B supplies the goods of Value Rs. 100 on which KGST Rate of 14% is applicable to Mr C who is a consumer or unregistered supplier, In this case Kerala Cess would be applicable.

| Value of Supply | 100 |

| CGST | 14 |

| KGST | 14 |

| Kerala Flood Cess | 1 |

| Gross Value | 129 |

6. How will I Pay Kerala Flood Cess to Government Account

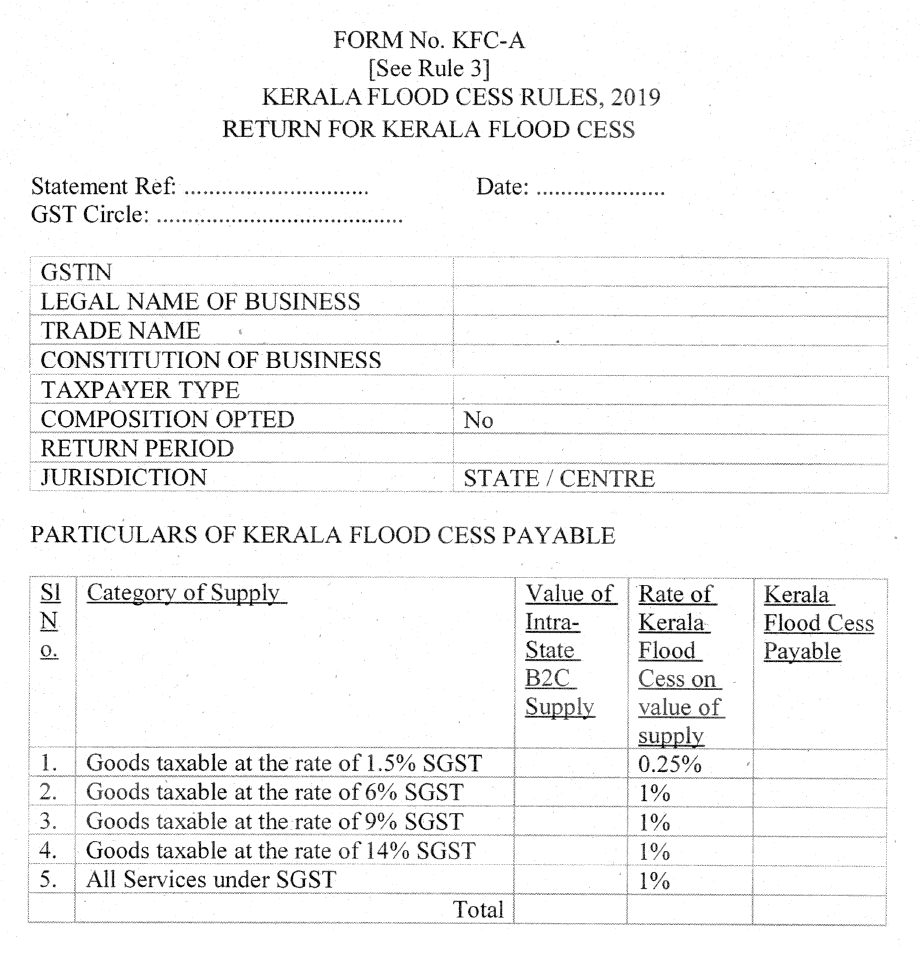

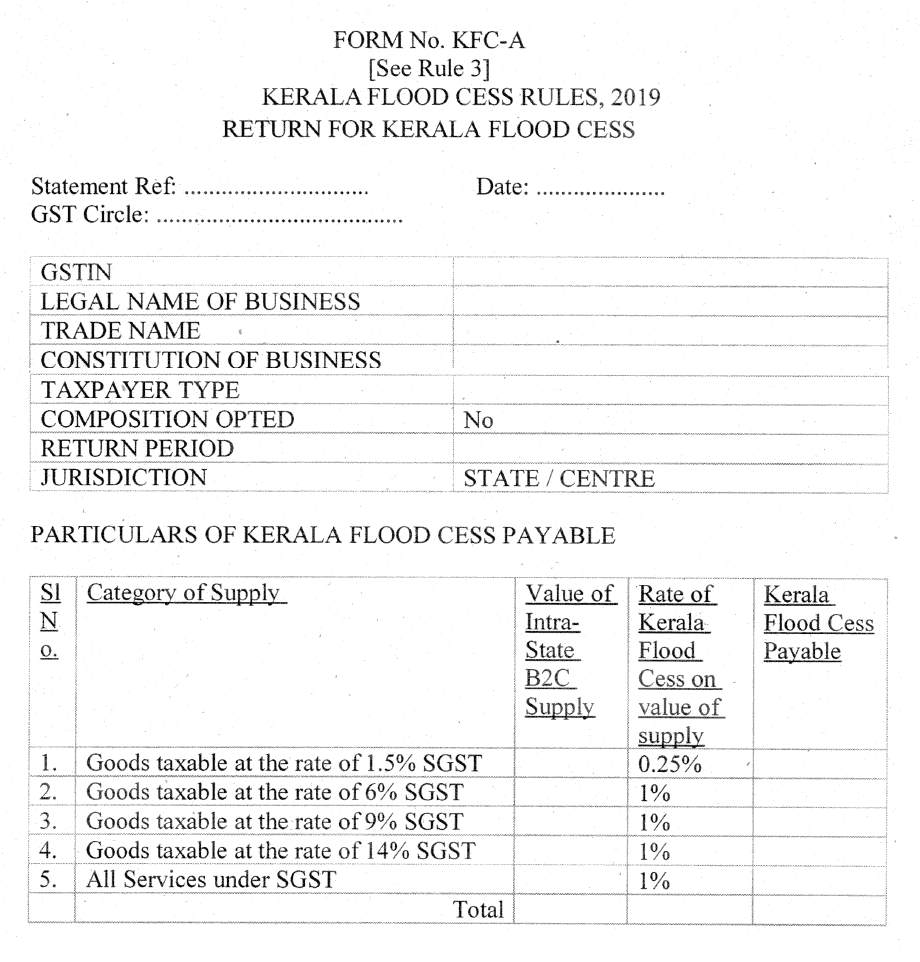

Online payment of Kerala Flood Cess due shall be made while filing monthly return in Form No: KFC-A on portal www.keralataxes.gov.in.

7. Is there any specific return required to be filed by businesses on which this liability is applicable

Yes businesses on which this liability is applicable will file Form No: KFC-A on portal www.keralataxes.gov.in.

8. What is the due date of filing Form No: KFC-A

Due date of filing Form No: KFC-A is 20th of Next Month.

9. Will I get Input Tax Credit of Kerala Flood Cess paid

No credit is allowed on the cess paid as the same is levied on transactions between the unregistered end consumers and the taxable persons. B2B transactions are not covered in Kerala Flood Cess.

10. Will I get Refund of Kerala Flood Cess

There shall be no refund of the Kerala Flood Cess paid along with the returns.

11. What is the Term upto which this cess is applicable

Kerala Flood Cess is applicable for the term of 2 years i.e. 30th June 2019.

Disclaimer: The entire contents of this document have been prepared on the basis of relevant provisions and as per the information existing at the time of the preparation. Although care has been taken to ensure the accuracy, completeness and reliability of the information provided, I assume no responsibility therefore. Users of this information are expected to refer to the relevant existing provisions of applicable Laws. The user of the information agrees that the information is not a professional advice and is subject to change without notice. I assume no responsibility for the consequences of use of such information. In no event shall I shall be liable for any direct, indirect, special or incidental damage resulting from, arising out of or in connection with the use of the information

About Author

CA Pratibha Goyal

Co Founder

Studycafe

Studycafe New Delhi, Delhi, India

New Delhi, Delhi, India 1486

1486My Recent Articles

- Biggest Labour Reform in Indian History: 4 Labour Codes Effective from today

- Tax Audit and ITR Due date not extended in this case: Know More

- Government notifies Agreement and Protocol between India and Qatar [Read Notification]

- CA Breaking: Results of ICAI Examination to be announced soon, Know probable Date

- Breaking: GSTR-3B Due Date for September 2025 extended by CBIC amid Diwali Festivities

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.