Reporting F&O income in ITR:

F&O Traders can opt for Presumptive Taxation Scheme u/s 44AD of Income Tax Income Tax Return F&O Traders can opt for Presumptive Taxation Scheme u/s 44AD of Income Tax

Income Tax Return

Table of Contents

Reporting F&O income in ITR

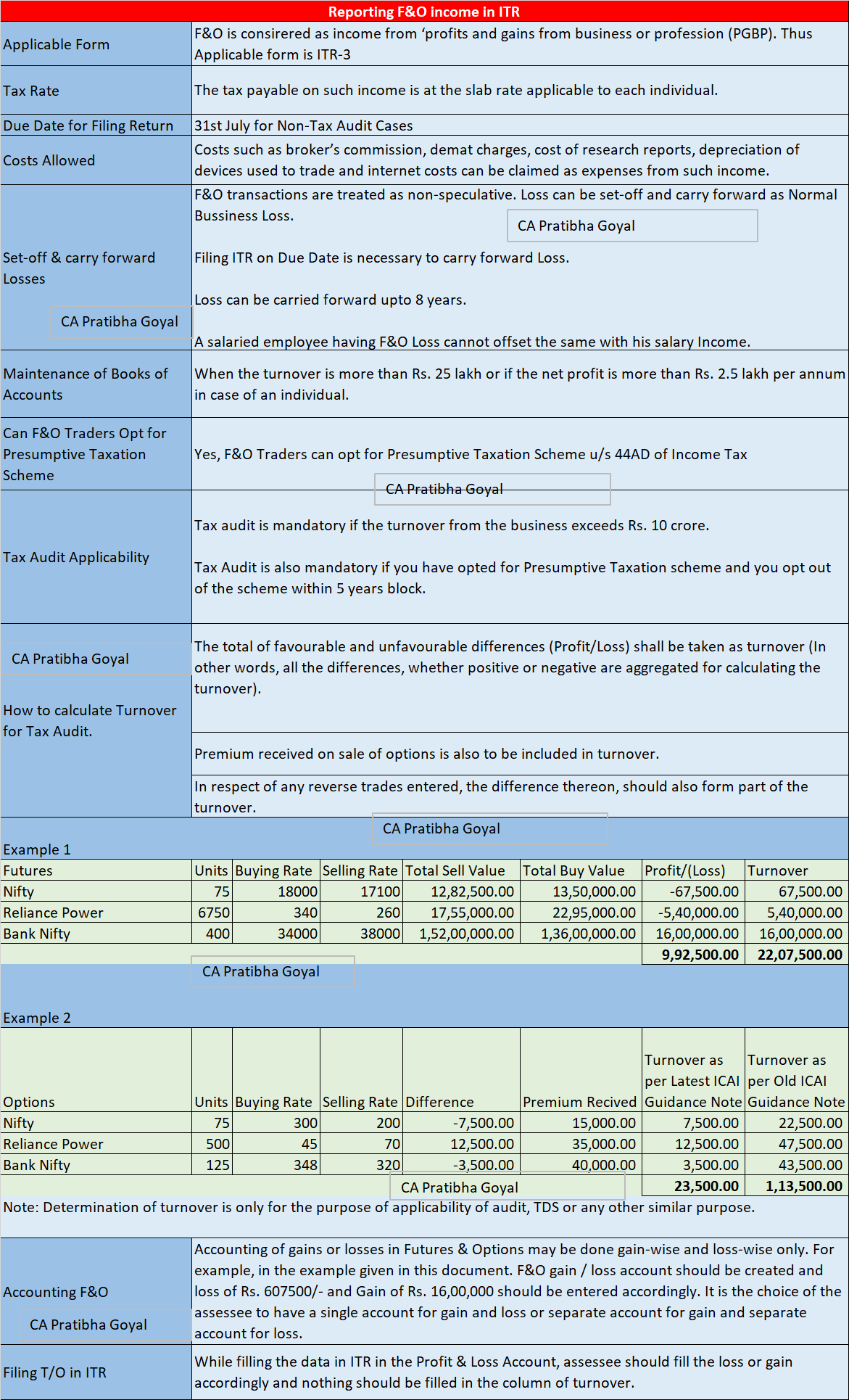

Applicable Form: F&O is consirered as income from ‘profits and gains from business or profession (PGBP). Thus Applicable form is ITR-3

Tax Rate: The tax payable on such income is at the slab rate applicable to each individual.

Due Date for Filing Return: 31st July for Non-Tax Audit Cases and 31st Oct if Tax Audit is applicable

Reporting F&O income in ITR[/caption]

Reporting F&O income in ITR[/caption]

Costs Allowed

Costs such as broker’s commission, demat charges, cost of research reports, depreciation of devices used to trade and internet costs can be claimed as expenses from such income.Set-off & carry forward Losses

- F&O transactions are treated as non-speculative. Loss can be set-off and carry forward as Normal Bussiness Loss.

- Filing ITR on Due Date is necessary to carry forward Loss.

- Loss can be carried forward upto 8 years.

- A salaried employee having F&O Loss cannot offset the same with his salary Income.

Maintenance of Books of Accounts

When the turnover is more than Rs. 25 lakh or if the net profit is more than Rs. 2.5 lakh per annum in case of an individual.Can F&O Traders Opt for Presumptive Taxation Scheme?

Yes, F&O Traders can opt for Presumptive Taxation Scheme u/s 44AD of Income TaxTax Audit Applicability

- Tax audit is mandatory if the turnover from the business exceeds Rs. 10 crores.

- Tax Audit is also mandatory if you have opted for the Presumptive Taxation scheme and you opt out of the scheme within 5 years block.

How to calculate Turnover for Tax Audit?

- The total of favourable and unfavourable differences (Profit/Loss) shall be taken as turnover (In other words, all the differences, whether positive or negative are aggregated for calculating the turnover).

- In respect of any reverse trades entered, the difference thereon, should also form part of the turnover.

Accounting F&O

Accounting of gains or losses in Futures & Options may be done gain-wise and loss-wise only. For example, in the example given in this document. F&O gain / loss account should be created and loss of Rs. 607500/- and Gain of Rs. 16,00,000 should be entered accordingly. It is the choice of the assessee to have a single account for gain and loss or separate account for gain and separate account for loss.Filing T/O in ITR

While filling the data in ITR in the Profit & Loss Account, assessee should fill the loss or gain accordingly and nothing should be filled in the column of turnover. [caption id="attachment_230767" align="aligncenter" width="1171"] Reporting F&O income in ITR[/caption]About Author

CA Pratibha Goyal

Co Founder

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

Studycafe

Studycafe New Delhi, Delhi, India

New Delhi, Delhi, India 1486

1486My Recent Articles

- Biggest Labour Reform in Indian History: 4 Labour Codes Effective from today

- Tax Audit and ITR Due date not extended in this case: Know More

- Government notifies Agreement and Protocol between India and Qatar [Read Notification]

- CA Breaking: Results of ICAI Examination to be announced soon, Know probable Date

- Breaking: GSTR-3B Due Date for September 2025 extended by CBIC amid Diwali Festivities

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts