Revision in Perquisite Limits for Salary Income [Budget 2025]:

![Revision in Perquisite Limits for Salary Income [Budget 2025]](https://assets.studycafe.in/uploads/2025/02/Perquisite-Limits-for-Salary-Income.jpg)

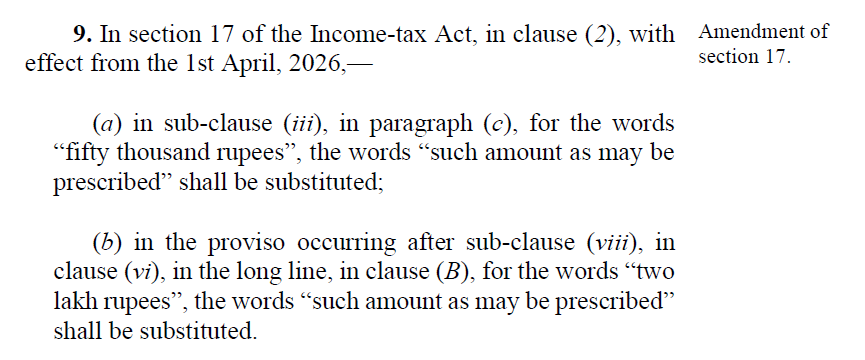

It is proposed that the provisions of section 17 may be amended so that the power to prescribe rules may be obtained to increase the limit on the gross total income of the employees.

Perquisite Limits for Salary Income Revised

Revision in Perquisite Limits for Salary Income [Budget 2025]

The existing provisions of Section 17(2) provide, inter-alia, that ‘perquisite’ includes the value of any benefit or amenity granted or provided free of cost or at concessional rate by any employer (including a company) to an employee whose income under the head "Salaries" as a monetary benefit does not exceed Rs.50,000. This upper limit on income was determined by the Finance Act 2001.

Further, the proviso to Section 17(2) provides that any expenditure incurred by the employer for travel outside India on the medical treatment of an employee or any member of the employee’s family shall not be included in ‘perquisite’, subject to the condition that the gross total income of such employee does not exceed Rs.2,00,000. This upper limit on income was determined by the Finance Act, 1993.

These limits on the income of the employees for the purpose of calculating perquisites were put in place more than 20 and 30 years ago respectively. Thus, there is a need to adjust these limits accordingly to take into account changes in standard of living and economic conditions.

It is proposed that the provisions of section 17 may be amended so that the power to prescribe rules may be obtained to increase the limit on the gross total income of the employees so that:

It is proposed that the provisions of section 17 may be amended so that the power to prescribe rules may be obtained to increase the limit on the gross total income of the employees so that:

It is proposed that the provisions of section 17 may be amended so that the power to prescribe rules may be obtained to increase the limit on the gross total income of the employees so that:

- the amenities and benefits received by such employees would be exempt from being treated as perquisites.

- the expenditure incurred by the employer for travel outside India on the medical treatment of such employee or his family member would not be treated as a prerequisite.

About Author

CA Pratibha Goyal

Co Founder

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

Studycafe

Studycafe New Delhi, Delhi, India

New Delhi, Delhi, India 1486

1486My Recent Articles

- Biggest Labour Reform in Indian History: 4 Labour Codes Effective from today

- Tax Audit and ITR Due date not extended in this case: Know More

- Government notifies Agreement and Protocol between India and Qatar [Read Notification]

- CA Breaking: Results of ICAI Examination to be announced soon, Know probable Date

- Breaking: GSTR-3B Due Date for September 2025 extended by CBIC amid Diwali Festivities

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.