Taxman can now block ITC credit available in Electronic Credit Ledger

Taxman can now block ITC credit available in Electronic Credit Ledger Rule 86A . Conditions of use of amount available in electronic credit

Taxman can now block ITC credit available in Electronic Credit Ledger

Rule 86A. Conditions of use of amount available in electronic credit ledger.-

(1) The Commissioner or an officer authorised by him in this behalf, not below the rank of an Assistant Commissioner, having reasons to believe that credit of input tax available in the electronic credit ledger has been fraudulently availed or is ineligible in as much as-

a) the credit of input tax has been availed on the strength of tax invoices or debit notes or any other document prescribed under rule 36-

i.issued by a registered person who has been found non-existent or not to be conducting any business from any place for which registration has been obtained; or

ii.without receipt of goods or services or both; or

b) the credit of input tax has been availed on the strength of tax invoices or debit notes or any other document prescribed under rule 36 in respect of any supply, the tax charged in respect of which has not been paid to the Government; or

c) the registered person availing the credit of input tax has been found non-existent or not to be conducting any business from any place for which registration has been obtained; or

d) the registered person availing any credit of input tax is not in possession of a tax invoice or debit note or any other document prescribed under rule 36,

may, for reasons to be recorded in writing, not allow debit of an amount equivalent to such credit in electronic credit ledger for discharge of any liability under section 49 or for claim of any refund of any unutilised amount.

(2) The Commissioner, or the officer authorised by him under sub-rule (1) may, upon being satisfied that conditions for disallowing debit of electronic credit ledger as above, no longer exist, allow such debit.

(3) Such restriction shall cease to have effect after the expiry of a period of one year from the date of imposing such restriction.”.

[caption id="attachment_85856" align="aligncenter" width="858"] Taxman can now block ITC credit available in Electronic Credit Ledger[/caption]

Restriction on using of ITC credit available in Electronic Credit Ledger

Govt has imposed restriction on using of ITC credit available in Electronic Credit Ledger on GSTN Portal vide Ntf no. 75/2019(Central Tax) dtd. 26.12.2019.

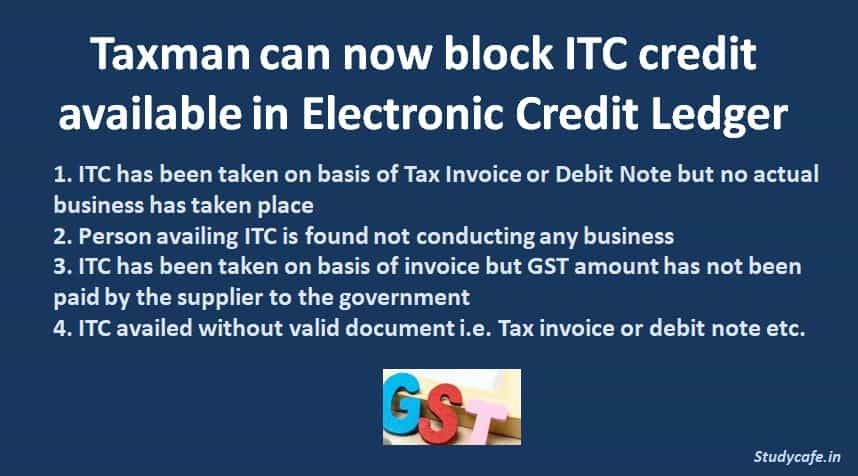

ITC may be blocked due to any of the below mentioned reasons:

1. ITC has been taken on basis of Tax Invoice or Debit Note but:

(a) issued by a registered person who has been found not conducting any business

(b) without receipt of goods or services or both

2. Person availing ITC is found not conducting any business

3. ITC has been taken on basis of invoice but GST amount has not been paid by the supplier to the government

4. ITC availed without valid document i.e. Tax invoice or debit note etc. Intention of government is to curb fraudulent transactions where no supply is made though includes billing only.

For Regular Updates Join : https://t.me/Studycafe

Tags : GST, Electronic Credit Ledger, Rule 86A

Taxman can now block ITC credit available in Electronic Credit Ledger[/caption]

Restriction on using of ITC credit available in Electronic Credit Ledger

Govt has imposed restriction on using of ITC credit available in Electronic Credit Ledger on GSTN Portal vide Ntf no. 75/2019(Central Tax) dtd. 26.12.2019.

ITC may be blocked due to any of the below mentioned reasons:

1. ITC has been taken on basis of Tax Invoice or Debit Note but:

(a) issued by a registered person who has been found not conducting any business

(b) without receipt of goods or services or both

2. Person availing ITC is found not conducting any business

3. ITC has been taken on basis of invoice but GST amount has not been paid by the supplier to the government

4. ITC availed without valid document i.e. Tax invoice or debit note etc. Intention of government is to curb fraudulent transactions where no supply is made though includes billing only.

For Regular Updates Join : https://t.me/Studycafe

Tags : GST, Electronic Credit Ledger, Rule 86AAbout Author

Pratibha Goyal

Admin

This Account belongs to Admistrator of Studycafe.

This Account belongs to Admistrator of Studycafe.

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 1080

1080My Recent Articles

- Chartered Accountants Association Embraces Income Tax Faceless Proceedings

- CBDT condones delay in filing form 10IC for AY 20-21: Know upto when to file the form to take concessional tax benefit

- ICAI Announced date of Live Coaching Classes for CA Intermediate Nov 2022 Exam

- ICAI Announced Registration Date for Online Home-Based Practical Training Assessment

- ICAI Released Mock Test Papers Series for May 2022 CA Exam

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts