TCS on sale of goods above 50 Lakhs under Income Tax

TCS on sale of goods above 50 Lakhs under Income Tax Provisions of TCS on sale of goods have been inserted by the Finance Act 2020 vide sect

TCS on sale of goods above 50 Lakhs under Income Tax

Provisions of TCS on sale of goods have been inserted by the Finance Act 2020 vide section 206C(1H) of the Income Tax Act. Provisions of this section require the seller, to collect tax on the amount received as sale consideration if it exceeds Rs. 50 Lakhs. CBDT has issued Circular Number 17/2020, dated 29/09/2020 to clarify doubts of Tax Payers.

This article discusses Frequently Asked Questions (FAQs) about the requirement to collect TCS on the sale of goods with effect from 01-10-2020.

TCS on sale of goods above 50 Lakhs under Income Tax[/caption]

TCS on Sale of Goods | TDS on sale of goods or services through e-commerce Operator

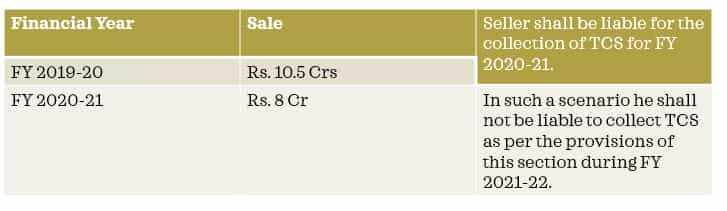

https://www.youtube.com/watch?v=7nS4sNNl3L8&t=98s1. Who is liable to collect tax on the sale of Goods?

Sellers whose business turnover exceeds Rs. 10 crores in the financial year immediately preceding the financial year of sale are liable to collect TCS on the sale of goods. This situation has been explained by the below-mentioned example: [caption id="attachment_91685" align="aligncenter" width="727"] TCS on sale of goods above 50 Lakhs under Income Tax[/caption]

2. From whom, the tax shall be collected?

TCS shall be collected if the following conditions are satisfied:- There is a sale of goods

- The seller receives any amount as consideration for the sale of any goods of the value or aggregate of such value exceeding Rs. 50 lakhs in any previous year.

3. Is there an exemption from provisions of TCS on sale Goods?

TCS on sale of goods shall not be collected in case of:- Export of goods

- Sale of goods to below-mentioned persons:

- Central Government;

- State Government;

- An Embassy, High Commission, a Legation, a Commission, a Consulate or Trade Representation of a Foreign state;

- Local Authority;

- A person importing goods into India; and

- Any other notified person.

TCS on Sale of Goods | Sale of Goods पर लगा नया Tax | Income Tax Press Release

https://www.youtube.com/watch?v=W8vOyPDlhdM&t=46s4. What shall be the timing of the collection of TCS on sale Goods?

Tax should be collected at the time of receipt of the amount from the buyer if the value of sale consideration received in a previous year exceeds Rs. 50 lakhs. The below-mentioned example has been used to explain this concept:| Particulars | FY2019-20 | FY2020-21 | FY2021-22 | FY2022-23 |

| Sale (A) | 6,000,000.00 | 8,000,000.00 | 7,000,000.00 | 7,000,000.00 |

| Balance Receivable on First Day of Year (B) | - | Rs. 4000000, (Rs. 55 lakhs received on or before 30-09-2020) | 2,000,000.00 | 4,500,000.00 |

| Balance Received (C) | 2,000,000.00 | 10,000,000.00 | 4,500,000.00 | 5,500,000.00 |

| Balance Receivable on Last Day of Year (D) | 4,000,000.00 | 2,000,000.00 | 4,500,000.00 | 6,000,000.00 |

| TCS | Nil, As Section 206C(1H) is applicable from 01-10-2020, no tax to be collected in the financial year 2019-20. | Rs. 3375, Tax will be collected only in respect of sale consideration received on or after 01-10- 2020, i.e. Rs. 45,00,000 * 0.075% = Rs. 4,500 [TCS Rate is 0.1%, but because of COVID the rate has been reduced by 25%] | Nil, as the amount of sale consideration received during the year does not exceed Rs. 50 lakhs. | Rs. 500, tax shall be collected on receipt in excess of Rs. 50 lakhs, i.e. 5,00,000 * 0.1% = 500 |

5. TCS on sale Goods is required to be collected in case of Exports?

TCS on sale of goods is not be collected in case of Export of goods.6. Whether a transaction in securities through stock exchanges shall be subject to TCS under this provision?

The CBDT has clarified that provisions of this section shall not be applicable in relation to transactions in securities (and commodities) which are traded through recognised stock exchanges or cleared and settled by the recognized clearing corporation, including recognised stock exchanges or recognized clearing corporations located in International Financial Service Centre (IFSC).7. In case of transaction of sale of immovable property, whether provisions of this section applicable?

The definition of goods is not given in the Income Tax Act. Definition of goods in various other Acts is given below: Sale of Goods Act, 1930 ‘Goods’ means every kind of movable property other than actionable claims and money; and includes stock and shares, growing crops, grass, and things attached to or forming part of the land which are agreed to be severed before sale or under the contract of sale” Central Goods and Services Tax Act, 2017 ‘Goods’ means every kind of movable property other than money and securities but includes actionable claim, growing crops, grass, and things attached to or forming part of the land which are agreed to be severed before supply or under a contract of supply” On basis of the above definitions, it can be said that the provision of this section is not applicable to the sale of immovable property.8. Whether TCS shall be collected on the sale of a motor vehicle?

The CBDT vide Circular No. 17, dated 29-09-2020 has clarified collection of TCS in case of sale of motor vehicles:- The tax shall be collected under Section 206C(1F) in the case of the sale of a motor vehicle to a consumer (B2C Transaction).

- Section 206C(1H) shall apply for the sale of a motor vehicles to the dealers or distributors (B2B).

- Further, sales to consumers where the consideration for a single vehicle is less than Rs. 10 lakhs but the aggregate value of which exceeds Rs. 50 Lakhs during a previous year, shall be subject to TCS underprovision of section 206C(1H) (B2C Transaction).

9. Whether TCS is liable to be collected from the re-sale of goods?

Where a person, who is re-selling the goods, falls within the definition of the seller, he will be liable for the collection of tax. However, if a person, re-selling the goods, is not engaged in carrying on of any business, no tax shall be collected under this provision. For Example, Mr X (a salaried person) buys jewellery of Rs. 55 lakhs from a Jeweller. The Jeweller collects a tax of Rs. 500 (0.1% of Rs. 5 lakhs) under section 206C(1H). If Mr X re-sells the jewellery for Rs. 60 lakhs to the same jeweller, he shall not be liable to collect tax as he is not engaged in any business or profession.10. At what rate TCS is required to be collected?

The tax shall be collected by the seller of goods at the rate of 0.1% of the sale consideration exceeding Rs. 50 lakhs if the buyer has furnished his PAN or Aadhaar, otherwise, the tax shall be collected at the rate of 1%. To provide more funds at the disposal of the taxpayers for dealing with the economic situation arising out of COVID-19 pandemic, the rates of TCS for the specified receipts have been reduced by 25% for the period from 14-05-2020 to 31-03-2021. Hence, the rate of TCS on sale of goods shall be 0.075% till 31-03-2021. However, if the buyer does not submit the PAN or Aadhaar the benefit of the reduced rate shall not be available.11. What is the date from which threshold limit of Rs. 50 Lakh shall be computed?

Threshold limit of Rs. 50 Lakh shall be computed from 1st April 2020. This is because the threshold is based on the yearly receipt. In this connection, it may be noted that this TCS shall be applicable only on the amount received on or after 1st October 2020. For example, a seller who has received Rs. 1 crore before 1st October 2020 from a particular buyer and receives Rs. 5 lakh after 1st October 2020 would be required to collect tax on Rs. 5 lakh only and not on Rs. 55 lakh [i.e Rs.1.05 crore - Rs. 50 lakh (threshold)] by including the amount received before 1st October 2020.12. Whether TCS is to be collected on the total invoice value including the GST?

Yes, TCS is to be collected on the total invoice value including the GST.13. Whether TCS provisions are applicable on advance received from buyers?

Yes, TCS provisions are applicable on the advance amount received for the sale of goods.14. What if the advance for the sale of goods is received before 1st Oct 2020 and sale is effected on or after 1st Oct 2020?

As per provisions of the section, the tax should be collected where the amount is received on or after 01-10-2020. Thus, where the event of receipt of sale consideration has occurred before the date of applicability of provision, no liability to collect tax will arise.15. What if the sale has been effected before 1st Oct 2020 but the consideration is received on or after 1st Oct 2020?

As per provisions of the section, the tax should be collected where the amount is received on or after 01-10-2020. Thus, where the event of receipt of sale consideration has occurred after the date of applicability of provision, liability to collect tax will arise.16. What if the loan has been received from the buyer, and later it is adjusted with Outstanding Sales Liability?

- As per provisions of the section, the tax should be collected where the amount for sales consideration for sales of goods is received.

- But in this case, money is received as a loan and not as consideration for the sale of goods.

- Here liability to collect TCS will arise when the loan amount is adjusted with Outstanding Sales Liability.

17. Whether TCS provisions will be applicable in case of Branch Transfers?

In the case of branch transfer, we cannot construe it as a sale from one distinct person to another. Thus TCS provisions are not applicable on the same.18. What is the process of Payment of TCS?

- TCS should be deposit in Challan No. 281

- TCS will have to deposit through internet banking.

- Indicate accurate TAN in challan

- Minor Head of Challan – 200 : TCS payable by tax payer

- Minor Head of Challan – 400: TCS Regular assessment raised by Income Tax Department.

- Amount of TCS, Interest, Late filing fee, penalty etc, should be separately shown while filing the challan

- Note down BSR code, Challan serial number, Date of payment, and amount of challan. This will help you in case challan is misplaced.

19. What is the due date of Payment of TCS?

| Taxpayer | Date of Deposit |

| Is office of the Govt. and tax is paid without production of income tax challan. | On the same day on which tax is deducted |

| Is office of the Govt. and tax is paid with production of income tax challan. | On or before 7 days from the end of month in which tax is collected. |

| Tax is collected by a person other than office of Government | On or before 7 days from the end of month in which tax is collected. |

20. What is the due date of filing TCS Return?

| Quarter | Period | Due Date |

| 1st Quarter | 1st April to 30th June | 15th July of the Finacial Year |

| 2nd Quarter | 1st July to 30th September | 15th Oct of the Finacial Year |

| 3rd Quarter | 1st October to 31st December | 15th Jan of the Finacial Year |

| 4th Quarter | 1st January to 31st March | 15th May of the financial year immediately following the financial year in which collection is made |

21. CONSEQUENCE ON DEFAULT IN TCS PROVISIONS

| Failure to collect tax at source and paid. [Sec 206C (7)] | Tax with interest @ 1% per month |

| Failure in furnish TCS return within stipulated time [U/S 234E] | Rs. 200 per day and shall not exceed the amount of tax deducted/collected. |

| Penalty for failure to furnish quarterly TCS return [271H] | Rs. 10000/- to Rs. 100000/- |

About Author

CA Pratibha Goyal

Co Founder

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

Studycafe

Studycafe New Delhi, Delhi, India

New Delhi, Delhi, India 1486

1486My Recent Articles

- Biggest Labour Reform in Indian History: 4 Labour Codes Effective from today

- Tax Audit and ITR Due date not extended in this case: Know More

- Government notifies Agreement and Protocol between India and Qatar [Read Notification]

- CA Breaking: Results of ICAI Examination to be announced soon, Know probable Date

- Breaking: GSTR-3B Due Date for September 2025 extended by CBIC amid Diwali Festivities

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.