Understanding recent SC Judgment on deduction of PF of special allowances

Understanding recent SC Judgment on deduction of PF of special allowances Hello Friends ! Here is the basic analysis of Supreme Courts Land

Understanding recent SC Judgment on deduction of PF of special allowances

Hello Friends ! Here is the basic analysis of Supreme Courts Land Mark Judgment in matter of Regional Provident Fund Commissioner (II) West Bengal Vs Vivekananda Vidyamandir and Others dated 28th February, 2019 which will help you in Understanding recent SC Judgment on deduction of PF of special allowances.

Legal Text Definition of Basic Wages is given below for reference:

Section 2 (b)(ii) of THE EMPLOYEES PROVIDENT FUNDS AND MISCELLANEOUS PROVISIONS ACT, 1952

basic wages means all emoluments which are earned by an employee while on duty or on leave or on holidays with wages in either case in accordance with the terms of the contract of employment and which are paid or payable in cash to him, but does not include-

(i) the cash value of any food concession;

(ii) any dearness allowance that is to say, all cash payments by whatever name called paid to an employee on account of a rise in the cost of living, house-rent allowance, overtime allowance, bonus, commission or any other similar allowance payable to the employee in respect of his employment or of work done in such employment;

(iii) any presents made by the employer;

Section 6 of THE EMPLOYEES PROVIDENT FUNDS AND MISCELLANEOUS PROVISIONS ACT, 1952

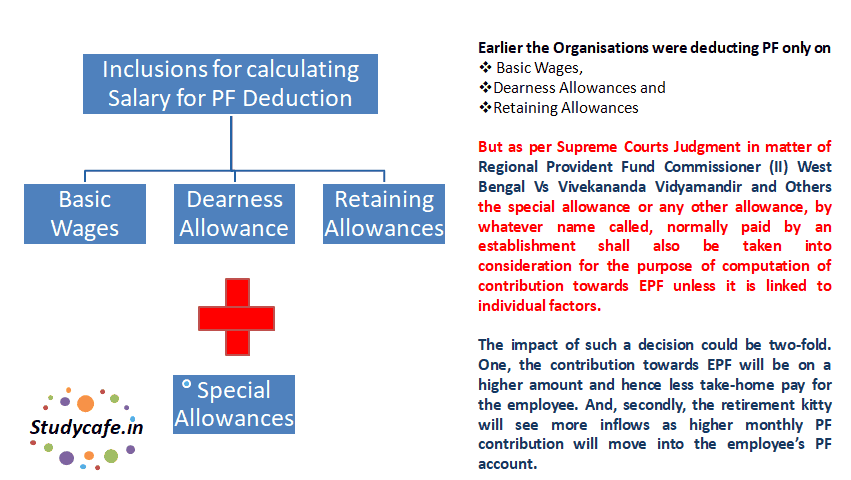

Contributions and matters which may be provided for in Schemes. The contribution which shall be paid by the employer to the Fund shall be ten percent. Of the basic wages, dearness allowance and retaining allowance, if any, for the time being payable to each of the employees whether employed by him directly or by or through a contractor, and the employee's contribution shall be equal to the contribution payable by the employer in respect of him and may, if any employee so desires, be an amount exceeding ten percent of his basic wages, dearness allowance and retaining allowance if any, subject to the condition that the employer shall not be under an obligation to pay any contribution over and above his contribution payable under this section:

Provided that in its application to any establishment or class of establishments which the Central Government, after making such inquiry as it deems fit, may, by notification in the Official Gazette specify, this section shall be subject to the modification that for the words ten percent, at both the places where they occur, the words 12 percent shall be substituted:

Provided further that where the amount of any contribution payable under this Act involves a fraction of a rupee, the Scheme may provide for rounding off of such fraction to the nearest rupee, half of a rupee, or quarter of a rupee.

Explanation I For the purposes of this section dearness allowance shall be deemed to include also the cash value of any food concession allowed to the employee.

Explanation II. For the purposes of this section, retaining allowance means allowance payable for the time being to an employee of any factory or other establishment during any period in which the establishment is not working, for retaining his services.

Understanding recent SC Judgment on deduction of PF of special allowances

Judgment of Supreme Court

Question Raised: The appeals raised a common question of law, which was that whether the special allowances paid by an establishment to its employees would fall within the expression basic wages under Section 2(b)(ii) read with Section 6 of the Act for computation of deduction towards Provident Fund.

In Simple terms the question was that: Whether contribution towards EPF is required to be paid on Special Allowance

Arguments placed by council of Provident Fund Organization:

The special allowance paid was nothing but camouflaged dearness allowance liable to deduction as part of basic wage.

Section 2(b)(ii) defined dearness allowance as all cash payment by whatever name called paid to an employee on account of a rise in the cost of living.

The allowance shall therefore fall within the term dearness allowance, irrespective of the nomenclature, it being paid to all employees on account of rise in the cost of living.

The special allowance had all the indices of a dearness allowance and thus should be included in salary while calculating the amount which is liable for deduction of PF.

Arguments placed against Provident Fund Organization:

The common submission on behalf of the appellants in the remaining appeals was that basic wages defined under Section 2(b) contains exceptions and will not include what would ordinarily not be earned in accordance with the terms of the contract of employment.

Even with regard to the payments earned by an employee in accordance with the terms of contract of employment, the basis of inclusion in Section 6 and exclusion in Section 2(b)(ii) is that whatever is payable in all concerns and is earned by all permanent employees is included for the purpose of contribution under Section 6.

But whatever is not payable by all concerns or may not be earned by all employees of a concern are excluded for the purposes of contribution.

Dearness allowance was payable in all concerns either as an addition to basic wage or as part of consolidated wages.

Retaining allowance was payable to all permanent employees in seasonal factories and was therefore included in Section 6.

It is only those emoluments earned by an employee in accordance with the terms of employment which would qualify as basic wage and discretionary allowances or special allowances not earned in accordance with the terms of employment would not be covered by basic wage.

The statute itself excludes certain allowance from the term basic wages. The exclusion of dearness allowance in Section 2(b)(ii) is an exception but that exception has been corrected by including dearness allowance in Section 6 for the purpose of contribution.

Special Allowances are not made universally, ordinarily and necessarily paid to all employees and therefore will not fall within the definition of basic wage and therefore should not be included in salary while calculating the amount which is liable for deduction of PF.

Key Takeaways from the Ruling of Honble Court:

- Any variable earning which may vary from individual to individual according to their efficiency and diligence will stand excluded from the term basic wages was considered in Muir Mills Co. Ltd., Kanpur Vs. Its Workmen, AIR 1960 SC 985

- Where the wage is universally, necessarily and ordinarily paid to all across the board such emoluments are basic wages.

Where the payment is available to be specially paid to those who avail of the opportunity is not basic wages. By way of example it was held that overtime allowance, though it is generally in force in all concerns is not earned by all employees of a concern. It is also earned in accordance with the terms of the contract of employment but because it may not be earned by all employees of a concern, it is excluded from basic wages.

- Any payment by way of a special incentive or work is not basic wages.

Manipal Academy of Higher Education vs. Provident Fund Commissioner, (2008) 5 SCC 428

Conclusion : Special allowances in question being paid to its employees were neither variable nor were linked to any incentive for production resulting in greater output by an employee

Also the allowances in question were not paid across the board to all employees in a particular category or were being paid especially to those who avail the opportunity.

Judgment : Special allowances in question were essentially a part of the basic wage are liable to deduction and contribution to the provident fund account of the employees.

What we learnt : From the above ruling, it can be said that special allowance or any other allowance, by whatever name called, normally paid by an establishment shall be taken into consideration for the purpose of computation of contribution towards EPF unless it is linked to individual factors as detailed supra. The test as mentioned above needs to be applied for every payment/allowance and which may not necessarily lead to a cent percent conclusion and depends on the facts and circumstances of each payment.

Impact : The impact of such a decision could be two-fold. One, the contribution towards EPF will be on a higher amount and hence less take-home pay for the employee. And, secondly, the retirement kitty will see more inflows as higher monthly PF contribution will move into the employees PF account.

Disclaimer: The entire contents of this document have been prepared on the basis of relevant provisions and as per the information existing at the time of the preparation. Although care has been taken to ensure the accuracy, completeness and reliability of the information provided, I assume no responsibility therefore. Users of this information are expected to refer to the relevant existing provisions of applicable Laws. The user of the information agrees that the information is not a professional advice and is subject to change without notice. I assume no responsibility for the consequences of use of such information. In no event shall I shall be liable for any direct, indirect, special or incidental damage resulting from, arising out of or in connection with the use of the information.

About Author

CA Deepak Gupta

Co Founder

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 3423

3423My Recent Articles

- UltraTech Cement slapped with Rs. 808.78 Cr Income Tax Demand

- GST: High Court upheld constitutional validity of Section 16(2)(c), asks government to address ITC issues of genuine purchasers

- Old vs New Tax Regime for Tax Year 2026-27

- High court criticizes Income Tax Department for not releasing ITR Utilities despite 11 years of directions

- Fino Payments Bank CEO Rishi Gupta Gets Bail in GST Case, Bank Clarifies No Direct Link

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.