Understanding What is Statement of Financial Transaction (SFT), Who is Required to File:

To keep an eye on large financial transactions made by taxpayers, the Income-tax Law has developed the SFT or Reportable Account. Know who is required to file it.

Understanding Statement of Financial Transaction (SFT)

Table of Contents

Understanding What is Statement of Financial Transaction (SFT), Who is Required to File

To keep an eye on large financial transactions made by taxpayers, the Income-tax Law has developed the Statement of Financial Transaction (SFT) or Reportable Account. This system assists tax authorities collect details about certain high-value transactions that people carry out during the year.

Some specific organizations or people (which we’ll talk about later) are required to file this statement. In the statement, they must report details of certain big financial transactions or accounts they have handled during the year.

With this information, the Income-tax Department can track important transactions made by individuals or businesses. In the following sections, you’ll learn more about the rules and requirements related to these statements and who has to file them.

According to Section 285BA of the Income Tax Act, 1961, certain institutions (called Filers) must file a statement of financial transactions or reportable accounts (SFT). This statement includes details of specific financial activities or accounts that they have recorded or handled during the financial year. The statement must be submitted to the Income Tax Department or another authority as prescribed.

Due Date to File SFT

The statement shall be furnished on or before 31st May immediately following the financial year in which the transaction is registered or recorded.

This means for Financial Year 2024-25, the SFT has to be filed before 31st May 2025.

Therefore it can be concluded that is not Mandatory to file NIL Statement.

Therefore it can be concluded that is not Mandatory to file NIL Statement.

However it is advisable to submit SFT Preliminary Response.

However it is advisable to submit SFT Preliminary Response.

Who are the persons Required to File Statement of Financial Transaction (SFT) or Reportable Account

The below-mentioned individuals are required to file a Statement of Financial Transaction (SFT) or reportable account that they handled during the financial year to the specified authority:- A banking company or a cooperative bank

- Post Master General

- Nidhi Company

- Non-banking financial company

- The institution issuing credit card

- A company or institution issuing bonds or debentures

- A company issuing shares

- A company listed on a recognised stock exchange purchasing its own securities under section 68 of the Companies Act, 2013

- A trustee of a Mutual Fund or such other person managing the affairs of the Mutual Fund

- Authorised person under Foreign Exchange Management Act, 1999

- Inspector-General or Registrar or Sub-Registrar appointed under the Registration Act, 1908

- Any person who is liable for audit under section 44AB of the Act

What are the Transactions that are required to be reported?

A banking company or a cooperative bank or any other company or institution issuing credit card to report Payment of Credit Card in Cash Payment of 1 lakh rupees or more in cash or 10 lakh rupees or more by any other mode made to settle Credit Card Bill is reported by the banking company or co-operative bank to which the banking regulation applies in Statements of Financial Transactions (SFT). A banking company or a cooperative bank to report Cash Deposits in a Savings Account A banking company or co-operative bank to which the banking regulation applies is required to report Cash deposits aggregating to ten lakh rupees or more in a financial year, in one or more accounts (other than a current account and time deposit) of a person. A banking company or a cooperative bank to report Cash Payment for RBI Pre-Payment Instruments: A banking company or co-operative bank to which the banking regulation applies is required to report Payments made in cash aggregating to ten lakh rupees or more during the financial year for the purchase of pre-paid instruments issued by Reserve Bank of India under section 18 of the Payment and Settlement Systems Act, 2007 (51 of 2007). A banking company or a cooperative bank to report Cash Deposits in a Current Account A banking company or co-operative bank to which the banking regulation applies is required to report Cash deposits or cash withdrawals (including through bearer's cheque) aggregating to fifty lakh rupees or more in a financial year, in or from one or more current accounts of a person. Inspector-General or Registrar or Sub-Registrar appointed under the Registration Act, 1908 to report Sale or Purchase of Immovable Property Purchase or sale by any person of immovable property for an amount of thirty lakh rupees or more or valued by the stamp valuation authority referred to in section 50C of the Act at thirty lakh rupees or more is required to be reported by Inspector-General appointed under section 3 of the Registration Act, 1908 or Registrar or Sub-Registrar appointed under section 6 of that Act. A trustee of a Mutual Fund or such other person managing the affairs of the Mutual Fund to report Investment in Mutual Funds, shares Debentures, and Bonds in Cash Cash Purchases of more than Rs. 10 Lakh of Mutual Funds, shares Debentures, and Bonds are reported in Statements of Financial Transactions (SFT). A banking company or a cooperative bank to report Cash Purchase of Fixed Deposit or Recurring Deposit Depositing more than Rs. 10 Lakh in cash to invest in Fixed Deposit (FD) or Recurring Deposit (RD) is reported by Banks in SFT and can invite Income Tax Notice. Authorised person under Foreign Exchange Management Act, 1999 to report Sale And Credit of Forex Card or Sale of Foreign Currency Receipt from any person for sale of foreign currency including any credit of such currency to a foreign exchange card or expense in such currency through a debit or credit card or through the issue of traveller's cheque or draft or any other instrument of an amount aggregating to Rs. 10 Lakh or more during a financial year can invite Income Tax Notice. Any person who is liable for audit under section 44AB of the Act Receipt of cash payment exceeding Rs. 2 lakh for sale, by any person, of goods or services of any nature will be reported by any person who is liable for audit under section 44AB of the Act. A company listed on a recognised stock exchange purchasing its own securities under section 68 of the Companies Act, 2013 to report Buy back of shares from any person (other than the shares bought in the open market) for an amount or value aggregating to Rs. 10 lakh or more in a financial year.Reportable transactions in SFT that are reflected in ITR

1. Capital gains on transfer of listed securities or units of Mutual Funds- Recognised Stock Exchange;

- Depository; CDSL and NSDL

- Recognised Clearing Corporation;

- Registrar to an issue and share transfer agent registered under section 12(1) of the SEBI Act, 1992.

- A Banking company, Non-banking financial company or a Co-op. Bank

- Post Master General

Made Mistake in SFT Report! What to Do?

Person filing the SFT finds the Mistake: Suppose any person, after filing the statement, comes to know or discovers any inaccuracy in the information provided in the statement. In that case, he shall inform such inaccuracy to the prescribed income- tax authority within a period of ten days and furnish the correct information. Income Tax Authority finds the mistake: On the other hand, the prescribed income-tax authority may also intimate the defect to the person and give him an opportunity of rectifying the defect within a period of thirty days from the date of such intimation or within such extended period as may be allowed by prescribed income-tax authority. What if the defect is not corrected? If a person fails to rectify the defect in the statement, it shall be deemed as such person had furnished inaccurate information in the statement. Penalty of Rs. 50000 is applicable: The prescribed income-tax authority may direct that such person shall pay, by way of penalty, a sum of fifty thousand rupees. Penalty of Rs. 5,000 is applicable: A penalty of Rs. 5,000 would be levied on reporting financial institution if there is any inaccuracy in SFT and such inaccuracy is due to false or inaccurate information submitted by the holder of reportable accounts. The reporting financial institution may also recover such penalty amount from the holder of the reportable account.What if I did not file SFT? Is Penalty Applicable for Non-Filing?

Yes, Non-furnishing of statement of financial transaction or reportable account will attract penalty under section 271FA. Penalty can be levied of Rs. 500 per day of default. However, section 285BA(5) empower the tax authorities to issue a notice to the person directing him to file the statement within a period not exceeding 30 days from the date of service of such notice and in such a case person shall furnish the statement within the time specified in the notice. If person fails to file the statement within the specified time, then a penalty of Rs. 1,000 per day will be levied from the day immediately following the day on which the time specified in such notice for furnishing the statement expires.What if there is no Such Transaction? Do we need to file Nil statement of financial transaction?

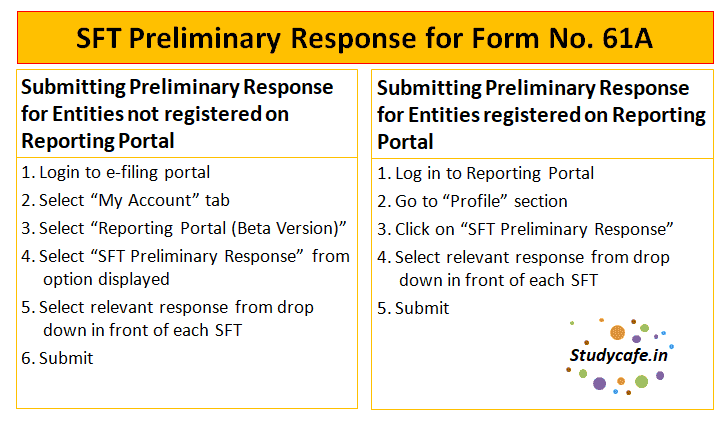

Income Tax Act does not specifically mandate filing of nil SFT. Further CBDT has released a Press Release on 26/05/2017 which says that The registration of reporting person (ITDREIN registration) is mandatory only when at least one of the Transaction Type is reportable. A functionality "SFT Preliminary Response" has been provided on the e-Filing portal for the reporting persons to indicate that a specified transaction type is not reportable for the year.

Therefore it can be concluded that is not Mandatory to file NIL Statement.

However it is advisable to submit SFT Preliminary Response.About Author

Saloni Kumari

Content Writer

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 2487

2487My Recent Articles

- ITAT Grants Fresh Opportunity to Explain Rs 2.39 Crore Demonetisation Cash Deposit Addition After Main Director’s DeathPremium

- ITAT Grants Taxpayer Fresh Opportunity to Contest Rs 44.16 Lakh Addition After Finding No Decision on MeritsPremium

- Trust’s Sections 12AB and 80G Registration Cannot Be Denied Before Charitable Project Is Completed, Holds ITATPremium

- ITAT Says Identity and Creditworthiness Irrelevant Where Loan Was Directly Paid to Haryana Mining DepartmentPremium

- Earlier Rejection Cannot Be Sole Ground to Reject Fresh Section 12AB and 80G Registration Applications, Says ITATPremium

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.