Wrongly Rejected IMS Records? GSTN advises How to Fix Them Fast:

Know the different situations for correcting ITC claims of rejected invoices on IMS.

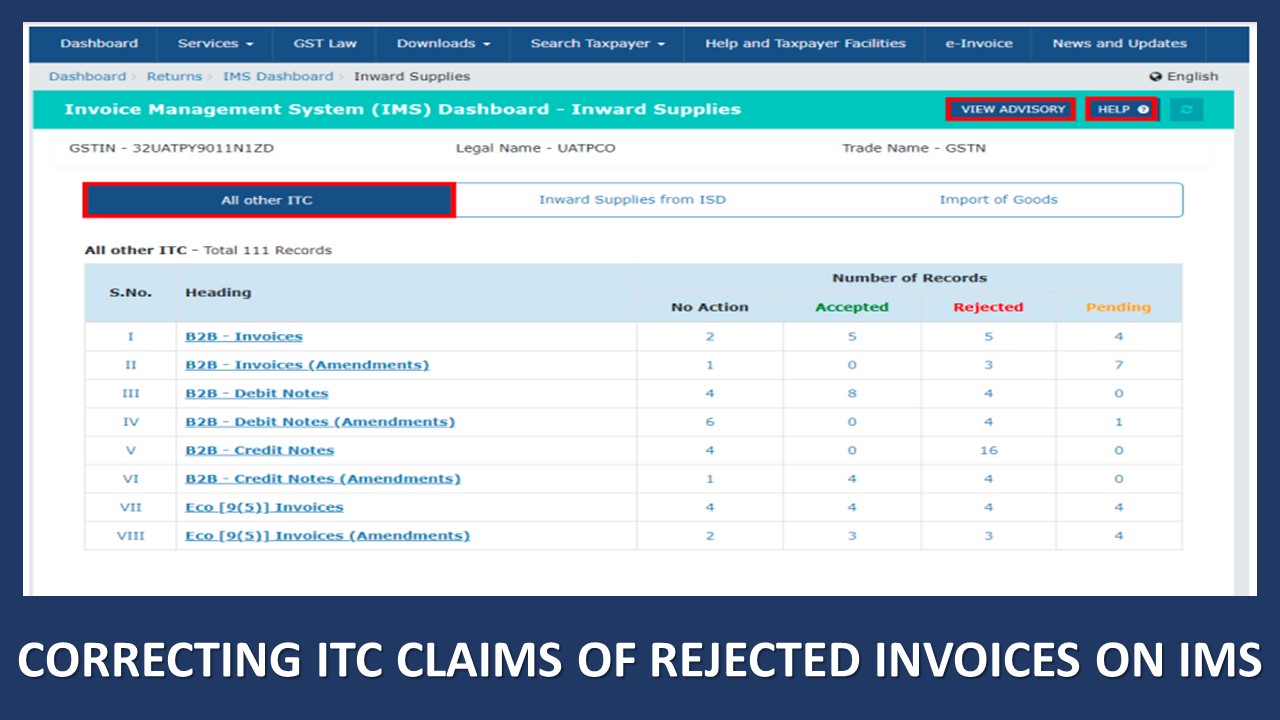

Managing ITC Claims of Rejected Invoices on IMS

Table of Contents

Wrongly Rejected IMS Records? GSTN advises How to Fix Them Fast

The Integrated Management System (IMS) on the GST portal helps to manage the invoices and their tax credits. It allows the taxpayers to review, accept, reject, or mark invoices pending. This helps in boosting the accuracy in claiming ITC and also reduces the manual workload on businesses so that businesses can operate efficiently. This system also promotes transparency and reduces disputes between suppliers and recipients.

Let us understand different situations for correcting ITC claims of rejected invoices on IMS:

How to avail ITC of wrongly rejected Invoices/ Debit notes/ECO-Documents?

If a recipient has claimed ITC of a wrongly rejected invoice, debit note, or ECO document or debit note in IMS, and has already filed GSTR-3B for that period, they can still claim the ITC. To do this, the recipient should request the supplier to submit the same document again (without making any changes) in GSTR-1A or in the amendment table of a GSTR-1/IFF. After the supplier does this, the recipient will get the ITC of the complete revised value, as the original record was rejected by the recipient. However, the recipient can claim ITC on the re-reported document by the supplier only in the GSTR-2B of the tax period. What to do in case original record is wrongly rejected? If the recipient has wrongly rejected a Credit note in IMS and has already filed GSTR-3B, then the recipient can reverse this ITC. To do it, the recipient can request the supplier to submit the same credit note (without making any changes) in the same period’s GSTR-1A or in the amendment table of a later GSTR-1/IFF. Once the supplier reports this, the recipient can accept the credit note on IMS and recalculate GSTR-2B. This will lower the ITC by the full amount of the original credit note. How to reverse ITC of wrongly rejected Credit note in IMS? If a supplier had filed a record in GSTR-1/IFF but the recipient wrongly rejected it in IMS, the supplier must submit the same record again (without any changes) in GSTR-1A of the same period or in the amendment table of a later GSTR-1/IFF, within the prescribed time. This will not increase the supplier's liability because the revised table records only the delta value. Therefore, the difference becomes zero, so there is no extra tax liability. If a recipient rejects an original credit note, and the supplier submits this in a credit note in GSTR-1A of the same tax period or in the amendment table of GSTR-1/IFF of the future tax period within the prescribed time limit, then the liability of the supplier is added back in their open GSTR-3B return. But if the supplier reports the same credit note again in GSTR-1A of the same period or in the amendment table of a later GSTR-1/IFF within the time limit, the liability of the supplier decreases by the same amount. As the credit note value stays the same, the net effect on the supplier's liability happens only once.About Author

Nidhi

Content Writer

Nidhi is a skilled content writer specializing in personal finance. She creates clear, engaging articles on mutual funds, investments, insurance, and wealth-building strategies. With a passion for simplifying complex financial topics, Nidhi helps readers make informed money decisions with confidence. She can be reached at [email protected]

Nidhi is a skilled content writer specializing in personal finance. She creates clear, engaging articles on mutual funds, investments, insurance, and wealth-building strategies. With a passion for simplifying complex financial topics, Nidhi helps readers make informed money decisions with confidence. She can be reached at [email protected]

Studycafe

Studycafe New Delhi, Delhi, India

New Delhi, Delhi, India 1833

1833My Recent Articles

- Karnataka High Court Gives Another Chance in GST Matter Due to Lack of Hearing

- Delay Should Be Condoned if Explanation is Unrefuted: ITAT

- Non-Service of Income Tax Notice, Ill health of taxpayer, ITAT condones Appeal filing delay

- Books of Accounts Cannot be Rejected Without Any Specific Defect: ITAT Kolkata

- Karnataka High Court Sends ITC Matter Back to GST Authorities for Reconsideration

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts