CA Pratibha Goyal | Jan 7, 2023 |

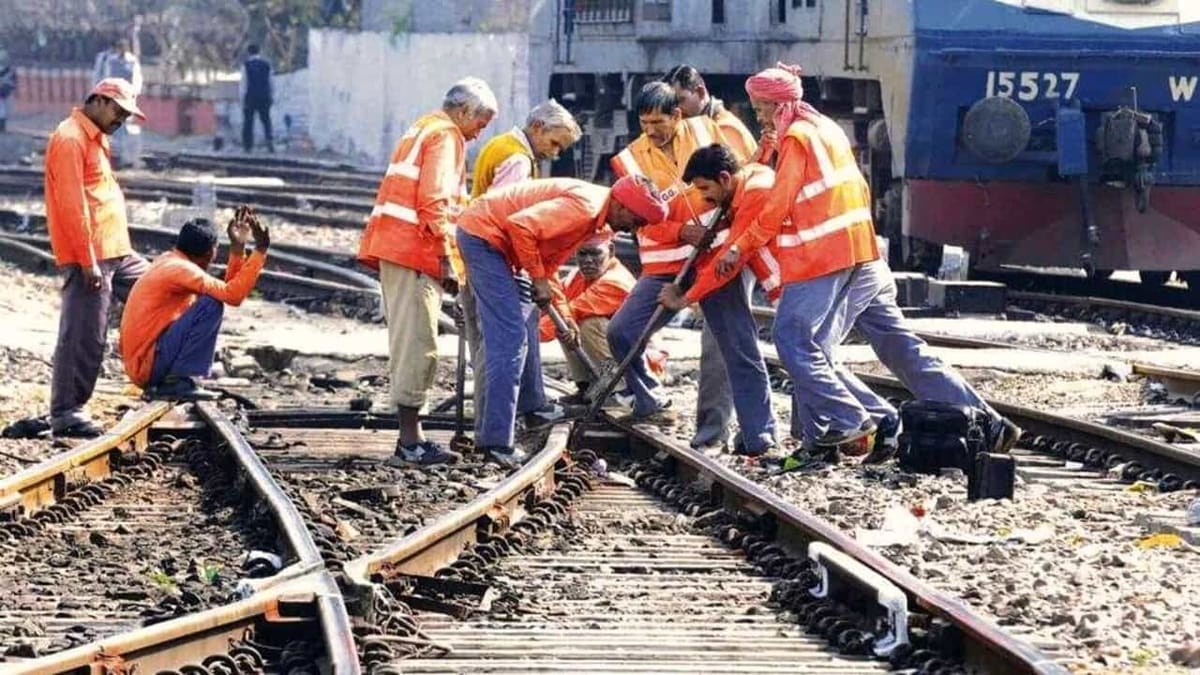

Welding railway tracks along with supply of labour composite supply: AAR

The Advance ruling Authority has ruled out that work being undertaken by applicant as a sub-contractor for conversion of Short Welded Rails (“SWR”) to Long Welded Rails (“LWR”) by Flash Butt Welding process on the railway tracks along with supply of labour services shall be treated as composite supply of services falling under Tariff 995429 and shall be taxable @ 18% vide serial number 3(xii) of Notification No. 11/2017-Central Tax (Rate) dated 28.06.2017, as amended from time to time [ corresponding West Bengal State Notification No.1135 F.T. dated 28.06.2017].

It is contended by the applicant that since the welding services are provided on railway tracks which can be easily detachable from the earth without any damage and no goods are transferred in the services involved, such services should not be treated as “works contract” as defined in clause (119) of section 2 of the GST Act. The applicant further argues that as the treatment or process of welding has only been carried out on goods i.e., on railway tracks to convert from SWR to LWR and the said goods are the property of Indian Railways who is a registered person under the GST Act, the services provided by them would fall under the ambit of job work in terms of definition laid down in clause (68) of section 2 of the Act ibid.

AAR said that railway tracks are considered to be the backbone of railway transportation system and to keep utmost priority on safety measures, railway tracks are firmly fastened on the sleepers. The applicant has contended that railway tracks are easily detachable and therefore should not be treated as immovable property. Considering the procedure as well as the technical aspects for laying of railway tracks, we are unable to accept the factum that railway tracks can easily dismantled from a place and subsequently can easily be laid again elsewhere.

AAR Bench of Mr Brajesh Kumar Singh, Joint Commissioner, CGST & CX and Mr Joyjit Banik, Senior Joint Commissioner, SGST said that the definition of “job work” is restricted to any treatment or process only i.e., the activities of a job worker is to undertake any treatment or process on goods which belongs to another registered person. In present case the contract awarded to the applicant is not limited to any treatment or process (the process of welding for the instant case) on goods belonging to another person. The scope of work as it is noticed from the work order covers the entire job for conversion of SWR to LWR including replacement of existing AT welds for a total distance of 54.03 km by flash butt welding. The work requires pulling back of rail, unfastening of fittings, lifting of rail with wooden block, opening out PSC sleepers either side of joints, removing of ballast, squaring, re-spacing and reinsertion of sleepers, putting back ballast, checking of joint sleeper, re-fixing of fittings etc.

Short Welded Rails (“SWR”) to Long Welded Rails (“LWR”) by Flash Butt Welding process cannot be treated as job work. The bench concluded that services of welding of railway track along with labour services are naturally bundled and supplied in conjunction in each other and therefore would fall under the ambit of “composite supply” as defined in clause (30) of section 2 of the GST Act.

For Official Ruling Download PDF Given Below:

In case of any Doubt regarding Membership you can mail us at [email protected]

Join Studycafe's WhatsApp Group or Telegram Channel for Latest Updates on Government Job, Sarkari Naukri, Private Jobs, Income Tax, GST, Companies Act, Judgements and CA, CS, ICWA, and MUCH MORE!"