The TDS rates for FY 2025-26 (AY 2026-27) detail the tax obligations on a variety of payments, such as salary, interest, rent, winnings, and professional fees.

Reetu | Feb 26, 2025 |

TDS Rate Chart for FY 2025-26 (AY 2026-27)

The Tax Deducted at Source (TDS) rates for FY 2025-26 (AY 2026-27) detail the tax obligations on a variety of payments, such as salary, interest, rent, winnings, and professional fees.

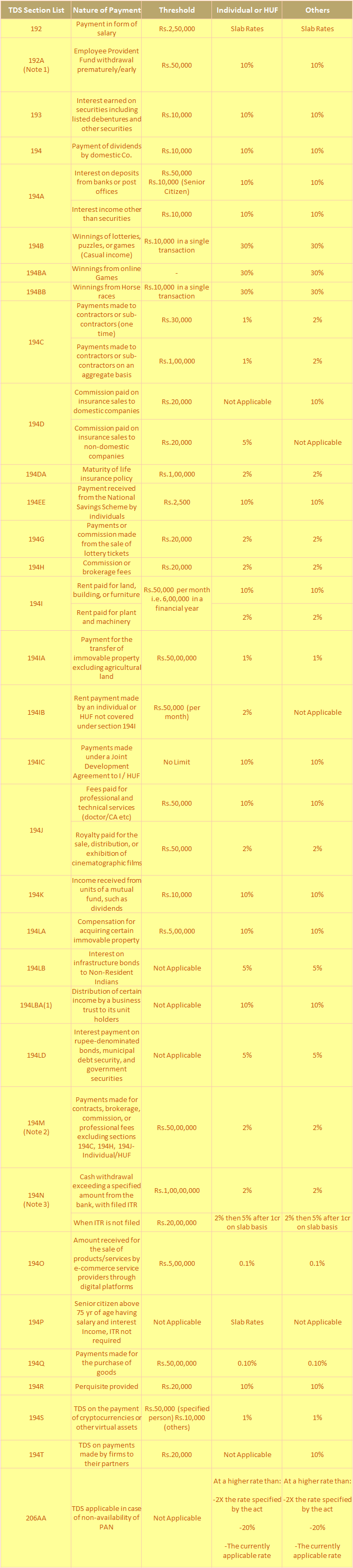

TDS on salaries (Section 192) is calculated using slab rates, whereas other payments have particular thresholds.

TDS on bank interest (Section 194A) applies to amounts beyond Rs.50,000 for senior citizens and Rs.10,000 for others, with a 10% rate. Lottery winnings (Section 194B) and online gaming profits (Section 194BA) are taxed at 30%. Payments to contractors (Section 194C) require 1% TDS for individuals and 2% for others if the amount exceeds Rs.30,000 in a single transaction or Rs.1,00,000 annually.

Rent payments (Section 194I) are subject to TDS at 10% on land and buildings and 2% on plant and machinery. Sales of property (Section 194IA) above Rs.50 lakh are subject to 1% TDS. The cash withdrawal limit for cooperative societies under Section 194N has been enhanced to Rs.3 crore.

Non-residents earning from mutual funds (Section 196A) can now claim lower TDS rates under tax treaties. Section 206AA also requires higher TDS rates if PAN is not present. Understanding these TDS rates enables taxpayers to comply and avoid penalties.

In case of any Doubt regarding Membership you can mail us at [email protected]

Join Studycafe's WhatsApp Group or Telegram Channel for Latest Updates on Government Job, Sarkari Naukri, Private Jobs, Income Tax, GST, Companies Act, Judgements and CA, CS, ICWA, and MUCH MORE!"