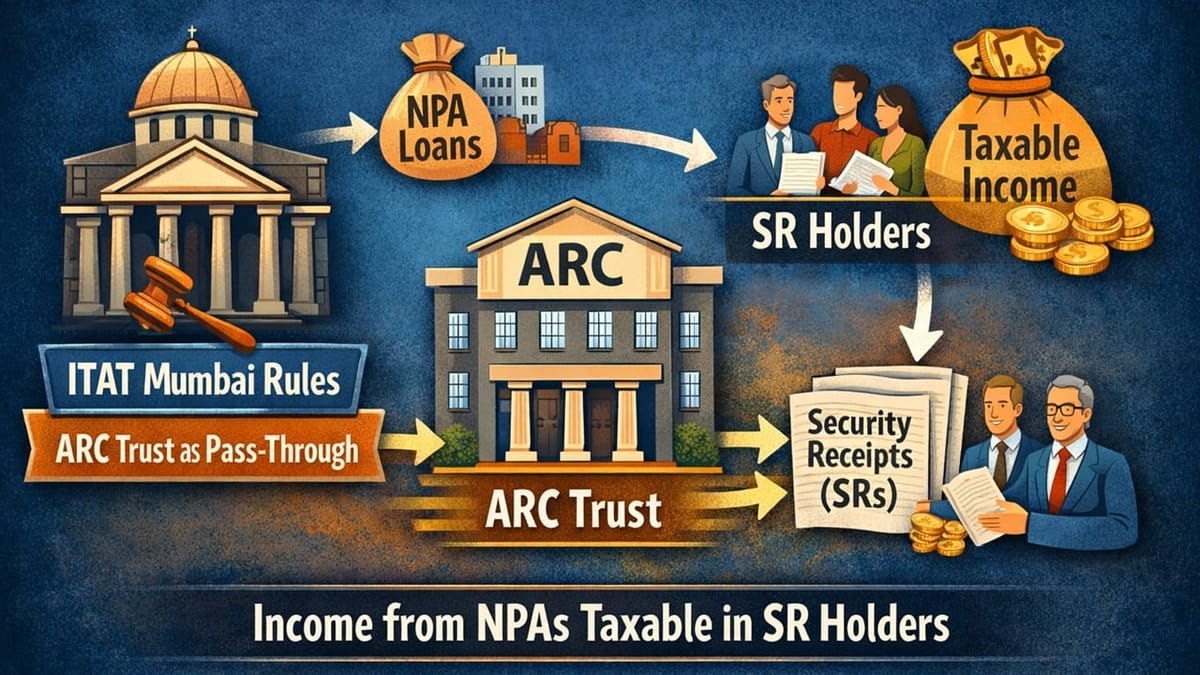

ITAT rules the ARC trust as a pass-through; income from NPAs is taxable in SR holders.

Meetu Kumari | Apr 20, 2026 |

ITAT Holds Securitisation Trust Not Taxable; Income Taxable in Investors’ Hands

The assessee, a trust created by Asset Reconstruction Company India Ltd. (ARCIL), was formed under the SARFAESI Act to acquire and manage non-performing assets (NPAs) from banks and financial institutions. The trust raised funds from qualified institutional buyers (QIBs) by issuing Security Receipts (SRs), representing their interest in the trust assets. For the relevant assessment year, the assessee declared nil income, contending that income arising from such a structure was taxable in the hands of SR holders due to the revocable nature of contributions.

The Assessing Officer rejected this position and held that the assessee functioned as an Association of Persons (AOP), engaged in business activity for profit. He further held that the trust was not revocable and invoked provisions of Section 164 to tax the income at the maximum marginal rate, determining total income at Rs. 16.30 crore. The CIT(A), however, accepted the assessee’s contention and deleted the addition, holding that the trust was a revocable trust and income was taxable in the hands of contributors. The Revenue appealed before the Tribunal.

Main Issue: Whether income arising in a securitisation trust formed under SARFAESI Act is taxable in the hands of the trust as an AOP or in the hands of Security Receipt holders under the provisions relating to revocable transfers.

Tribunal’s Decision: The Tribunal dismissed the Revenue’s appeal and upheld the order of the CIT(A). It held that the assessee trust is a valid securitisation trust constituted under the SARFAESI Act and governed by RBI guidelines. The structure clearly established that contributions made by SR holders were revocable in nature, attracting the provisions of Sections 61 to 63 of the Act.

Relying on a coordinate bench decision on identical facts, the Tribunal observed that such trusts function merely as pass-through entities, and the income arising therefrom is taxable in the hands of the contributors, i.e., SR holders. It rejected the Assessing Officer’s view that the assessee should be treated as an AOP, noting that there was no inter se arrangement among contributors to jointly carry on business. The Tribunal further held that provisions of Section 164 were not applicable, and in the absence of any contrary precedent or distinguishing facts, judicial discipline required following earlier rulings. Therefore, it concluded that the income cannot be taxed in the hands of the trust and deleted the addition.

To Read Full Order, Download PDF Given Below

In case of any Doubt regarding Membership you can mail us at [email protected]

Join Studycafe's WhatsApp Group or Telegram Channel for Latest Updates on Government Job, Sarkari Naukri, Private Jobs, Income Tax, GST, Companies Act, Judgements and CA, CS, ICWA, and MUCH MORE!"